The Playoff Beard

I am a fan of the Washington Capitals, and if you follow hockey, you probably know that they are currently playing in the second round of the playoffs against the Pittsburgh Penguins. It has become somewhat of a tradition for players (and now fans) to let their beards grow for as long as the team is still playing (the longer the beard, the closer to a championship). More recently, fans have been raising money for various charities by asking people to “sponsor” their beards.

Personally, I am just jumping on the bandwagon and growing my beard to show my allegiance to the team. Plus, I grow a pretty decent beard if I do say so myself. Maybe next year (assuming the Caps make the playoffs!), I will be more charitably minded and pick a good cause. If you are so inclined, click here to support the USA Warriors Ice Hockey program.

Anyway, in the playoffs, everything is magnified. Mistakes and penalties seem (and are) more costly, and goals are harder to come by. In a best of seven game series, there is little room for error…which reminds me of the need for proper planning as people near retirement. Approaching retirement can be a lot like playoff hockey; mistakes with your investments are magnified and can derail your plans to retire and even cause you to have to work longer.

While it’s always important to pay attention to your investment allocation, it becomes even more important as you get close to the transition from saving for retirement to spending in retirement. The set it and forget it strategy can work for a while, but when you are in the “playoffs” of your working years, avoiding errors becomes paramount.

Unfortunately, errors can occur in a few ways; from taking too much risk for your situation, to being too conservative and not getting the returns needed to reach your goals. One of the most common mistakes is not rebalancing your account on a regular basis. Rebalancing means to reset your investments to the way you initially intended on a regular basis. Most agree that rebalancing annually (more on this in next week’s blog!) is adequate.

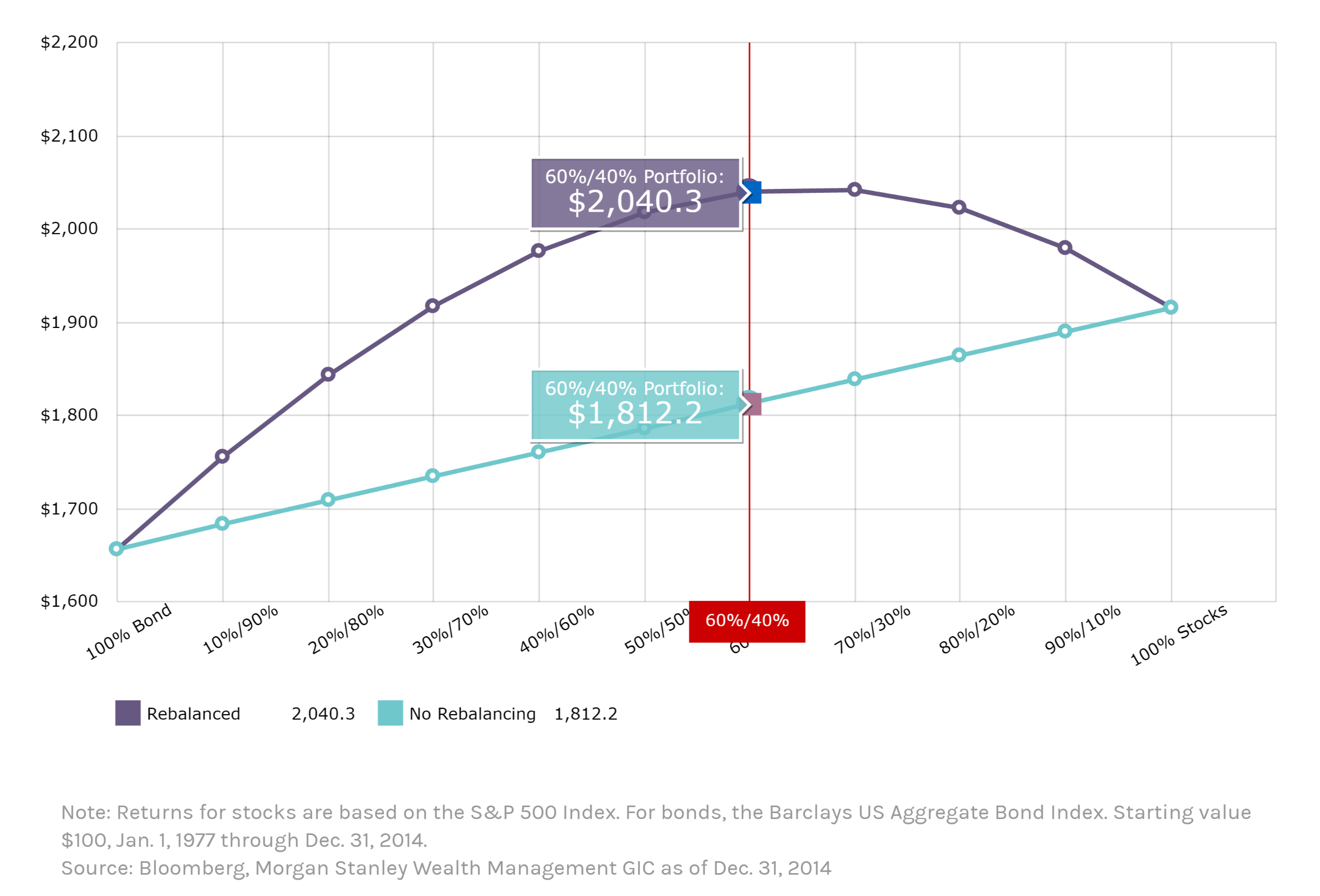

Inevitably, a portion of your portfolio will perform better than other parts during a calendar year, and you can end up taking too much (or to little) risk unintentionally. Below is a chart from Morgan Stanley showing how rebalancing can actually help returns and reduce volatility in most cases. It shows how $100 would have grown from January 1, 1977 to December 31, 2014. The light blue line is the set it and forget it strategy (not rebalancing), and the purple line is rebalancing to the intended mix of stocks and bonds on an annual basis.

Interestingly, a portfolio of 60% stocks and 40% bonds (when rebalanced annually) actually outperformed an all stock (the S&P 500) portfolio. In every case, rebalancing boosted returns fairly significantly. One other thing to keep in mind is that all of your accounts should be working together. If you have an active 401(k) plan at work as well as an IRA, it’s important to make sure they are allocated as though they are one account. In other words, if you are conservative in one, maybe you need to be more aggressive in the other or vice versa. Just remember that your investment mix should fit your specific situation, and that in the playoffs of your career, mistakes are magnified.

Here’s hoping that I don’t have to shave anytime soon and the Capitals advance to the next round. As of the writing of this blog, they are trailing 2-1 in the series. Let’s go CAPS!