Yankee Swap

The 2017 holiday season is in full swing, and as always, by this point in the year, I am getting tired. Our family has been to 6 Christmas concerts in 12 days…baked 20 dozen cookies…made (and decorated) 3 gingerbread houses…wrapped upteen gifts…and attended 8 holiday parties, each with its own gift exchange.

Most of the parties we attended had a Yankee Swap style gift exchange—as hilariously shown in an episode of The Office, a Yankee Swap gift exchange usually allows gifts to be “stolen” or swapped as the exchange progresses. A Yankee Swap style gift exchange also can go by other names the Grinch Game, Thieving Elves, Cutthroat Christmas, Machiavellian Christmas, or my favorite…Snatchy Christmas Rat.

Call it what you will, but as details of the new tax act heading to vote this week emerged over the weekend, it appears we have an epic game of Yankee Swap (or Machiavellian Christmas) in Congress.

Here are some of the major “swaps” in the current proposal:

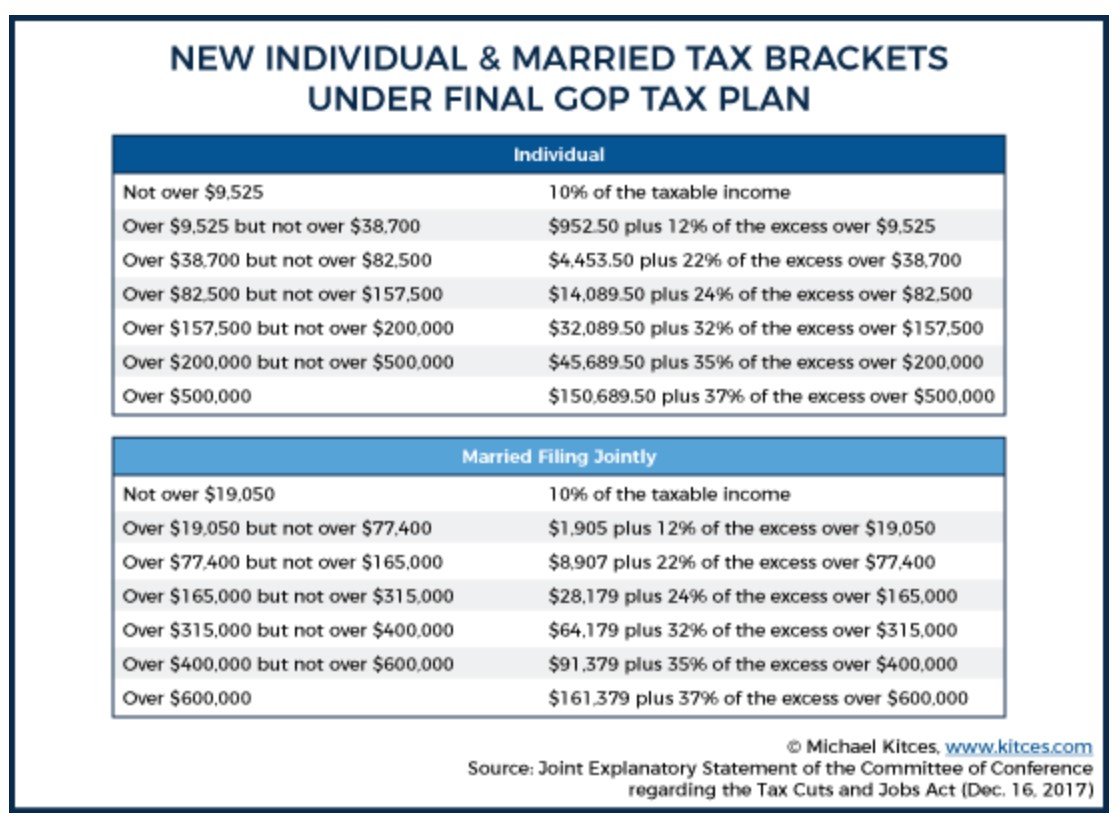

- We keep the seven brackets that we had, but we swap the tax rates for slightly lower rates and expanded brackets:

- We have swapped more generous itemized deductions for a higher standard deduction. The new plan almost doubles the standard deduction for a married couple filing jointly from $13,000 currently to $24,000. For single filers it jumps from $6,500 to $12,000. However, the following itemized deductions now have less generous caps:

- State and Local Tax (“SALT”) Deduction –all state and local income taxes, state and local sales tax, and real estate taxes must be aggregated and limited to a maximum deduction of $10,000 for all filing statuses (aside from $5,000 for married filing separately).

- Mortgage Interest – Only the interest on $750,000 (previously $1,000,000) of home acquisition or refinance debt will be deductible. This becomes effective with mortgages originating after December 15, 2017

- Casualty Losses – No longer allowed aside from those resulting from a Federally declared disaster.

- Miscellaneous Itemized Deductions Subject to 2% Limitation – These are no longer allowed and include items such as: broker fees, tax preparer fees, unreimbursed employee expenses, safe deposit boxes, employee home office deductions, etc.

- We have swapped exemptions for dependents for tax credits. Currently, every taxpayer and dependent gets a $4,150 personal exemption. So, a married couple with two children would have a $16,600 deduction. Under the new tax bill, this is eliminated, however it is swapped for a higher standard deduction ($11,000 higher for a married couple). The child tax credit is also expanded to receiving a tax credit (a direct reduction of taxes owed, rather than a deduction) of up to $2,000 per child. So, this may be a wash for some families.

There are many more changes in the tax plan as proposed—for a more detailed discussion, we highly recommend the great blog post by Michael Kitces found here or this nice summary provided to us by our good friends at PB Mares.

As these new tax rules are digested, we are certain that there will be new tax strategies that emerge for 2018, and we will be sure to apply them in our management of your money. For now, the main two things that you should do in 2017 are:

- Make sure that you have paid all of your state and local taxes owed for 2017 in this tax year, as the deduction may be capped for you next year.

- Accelerate charitable gifts into 2017 if you do not expect to itemize next year with the new expanded standard deduction.

Otherwise, relax and enjoy your holidays, and we will check back in next year!