Should I Pay or Should I Go?

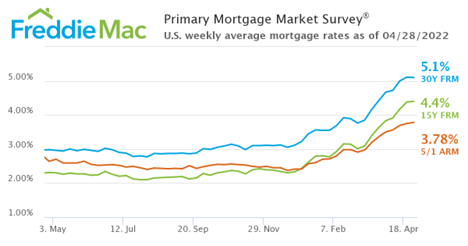

Recently, we have been fielding many questions about whether it is more prudent to use excess cash to pay off a mortgage or go invest. While we do answer this question with regularity, the interest in paying off (or accelerating paydown) a mortgage seems to have risen over the past month. Maybe because of the headline mortgage rates moving up dramatically since last year?

Or because the investment alternatives for cash have been so scary as of late?

Either way, we have been tackling this question of mortgage payoff a lot in 2022.

In general, the mathematical answer has been to hold on to your mortgage and invest your cash when the rate of return that you could earn on your cash would be greater than the interest rate you pay on your mortgage. This was a relatively easy decision when mortgage rates were 3% to 4% and a balanced investment portfolio was expected to earn 4-6% conservatively over a long period.

In today’s environment, that decision is getting a little murkier. Several assumptions complicate that mathematical analysis:

- You can get a mortgage rate lower than 4%

- You have the risk tolerance to invest in a portfolio that could earn more than 4% and handle the risk involved

- You invest or save the amount of money you were going to put towards your mortgage (not spend it)

If any of these assumptions shift, then the decision to pay or go invest is more complicated.

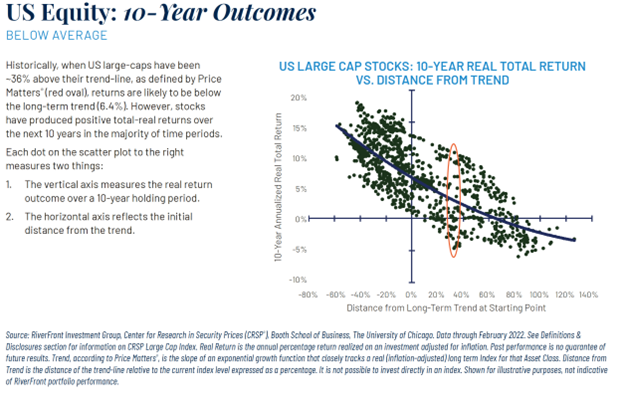

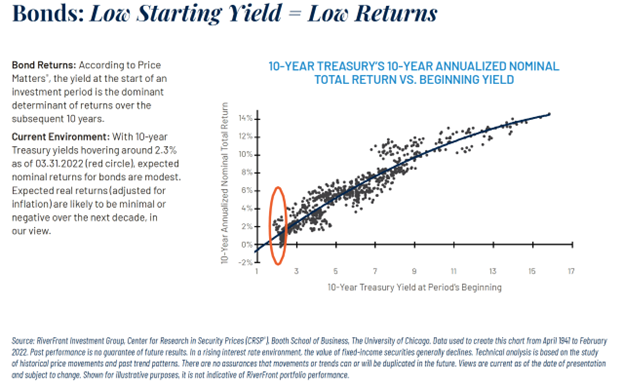

Right now, with mortgage rates in the 5% range, an investment portfolio has to assume more risk to clear that hurdle. Riverfront Investment Group neatly sums up what the historical data shows us about potential forward returns for stocks and bonds based on current valuations and interest rates:

If a balance investment portfolio of 60% stocks and 40% bonds historically has earned 4-6% from our current valuation levels, then picking between paying down a 5% mortgage (for a ‘guaranteed’ return) or a 4-6% investment portfolio (with assumed risk) is a hard choice.

Other considerations that need to be factored into the decision to pay off a mortgage or invest are:

- Are there other cash resources available to fund living expenses? No sense in using all available cash to pay off a mortgage and then have no funds available to pay day-to-day bills…or being “house rich and cash poor”

- Will paying off the mortgage with cash that is not productive (CDs, savings account, money market monies not needed for other purposes) help to reduce the cash flow burden on fixed income streams (like social security and pensions)?

- If deciding against making additional principal payments on a mortgage in favor of investing, is there a system in place to make sure that extra payment money DOES get invested (and is not just spent)?

- Is there a peace of mind that is achieved from paying off a mortgage before retirement? That is a hard benefit to numerically quantify!

In closing, what has been a relatively simple calculation and decision has become far more complicated recently. Paying a mortgage off sooner should be analyzed in the context of a full financial plan…and if you need help working through that process, we’d love to help!