Retirement in America: From Family Farms to 401(k)s

As the United States approaches its 250th birthday, the evolution of retirement tells a powerful story about how Americans have worked, saved, and planned for the future across generations. From family farms in colonial America to today’s 401(k)-driven retirement system, retirement has changed dramatically alongside the nation itself.

In early America, retirement as we know it barely existed. Most people worked on family farms or in family-owned businesses, where older generations gradually reduced their workloads while younger family members took over. Financial security depended largely on land ownership, family support, and personal savings rather than formal retirement accounts.

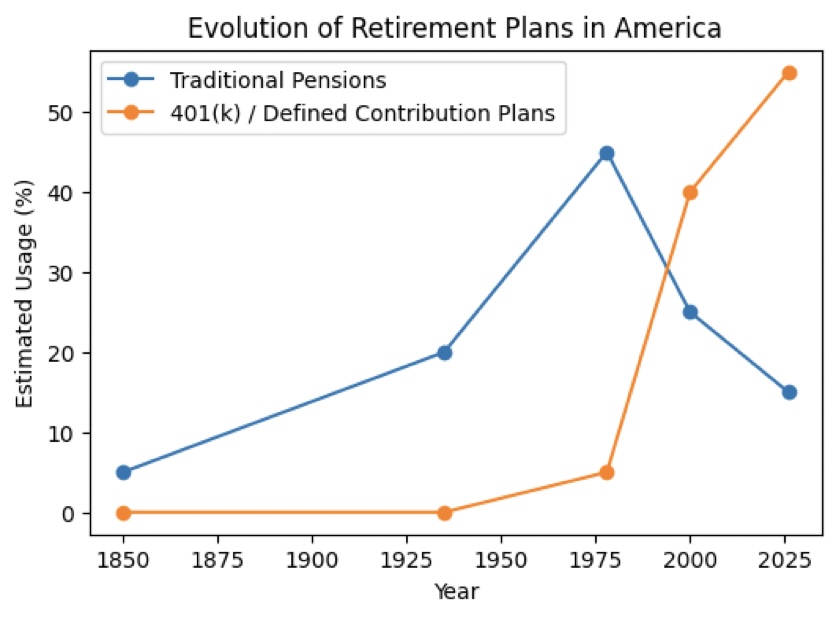

During the Industrial Revolution, Americans increasingly moved from farms to factories, creating a need for more structured retirement systems. Factory work was physically demanding, and older workers often struggled to continue labor-intensive jobs. In response, pensions began emerging in the late 1800s, particularly among railroad companies, government employers, and large corporations. These pensions rewarded long-term employees with guaranteed retirement income.

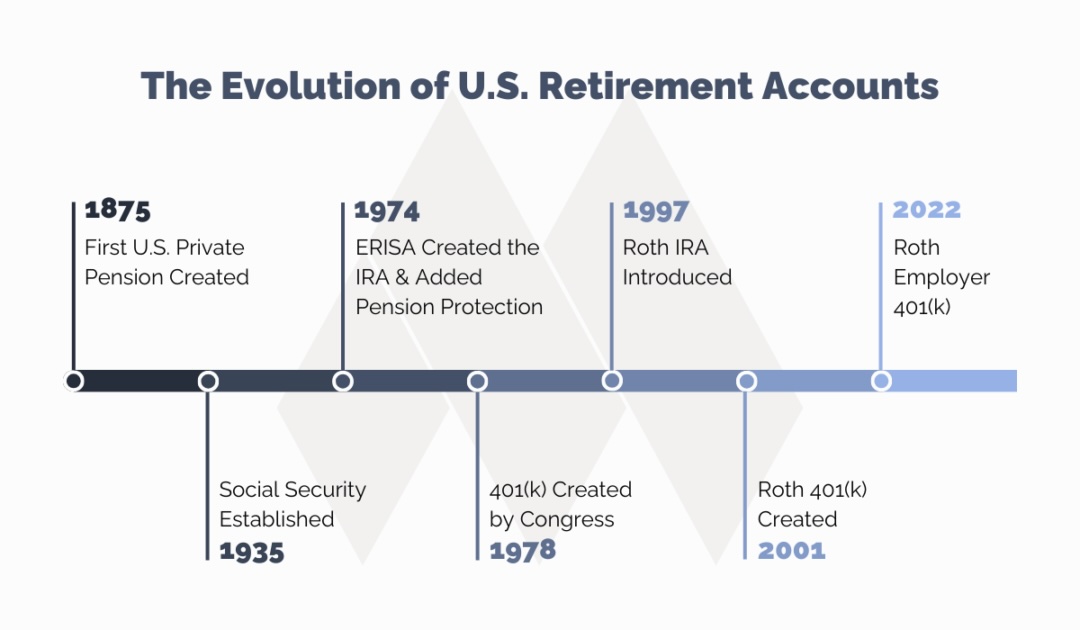

The Great Depression highlighted the financial vulnerability many older Americans faced, leading to one of the most important milestones in retirement history: the creation of Social Security in 1935. For the first time, the federal government established a nationwide retirement safety net funded through payroll taxes. Social Security remains a foundational part of retirement income for millions of Americans today.

Following World War II, employer-sponsored pensions became increasingly common during America’s economic boom. Many workers relied on a combination of pensions, Social Security, and personal savings to support retirement. Retirement at age 65 became a widely accepted goal, and long-term employment with a single company was common.

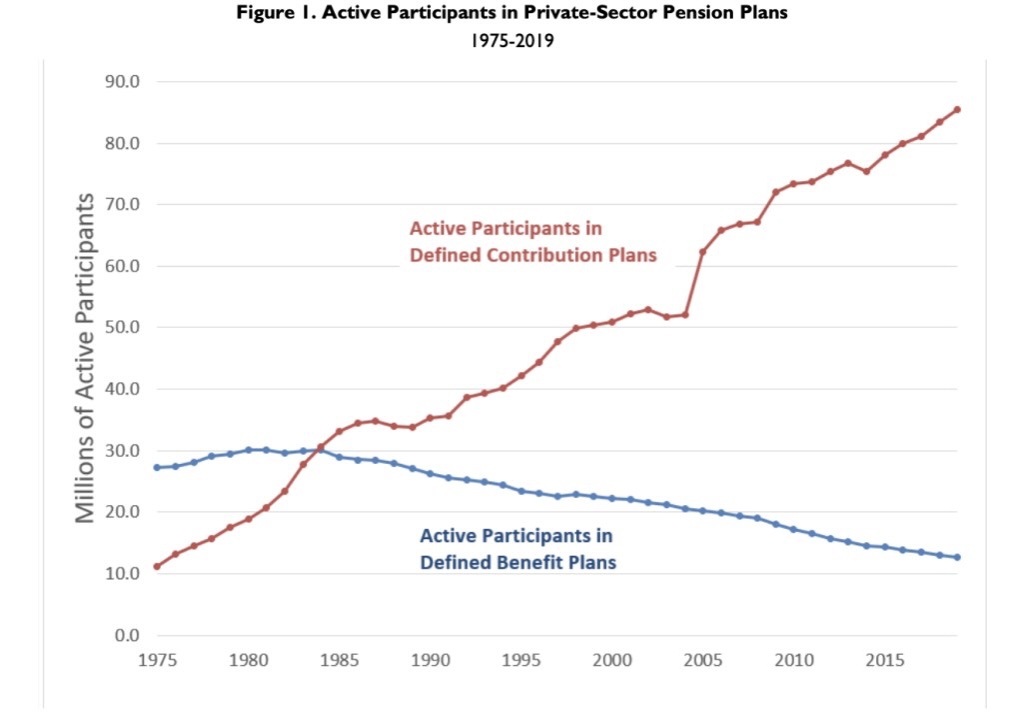

However, retirement planning shifted significantly in the late 20th century with the rise of the 401(k). Created through tax law changes in 1978, 401(k) plans allowed employees to contribute pre-tax income into investment accounts for retirement. Over time, many employers moved away from traditional pensions in favor of these defined-contribution plans.

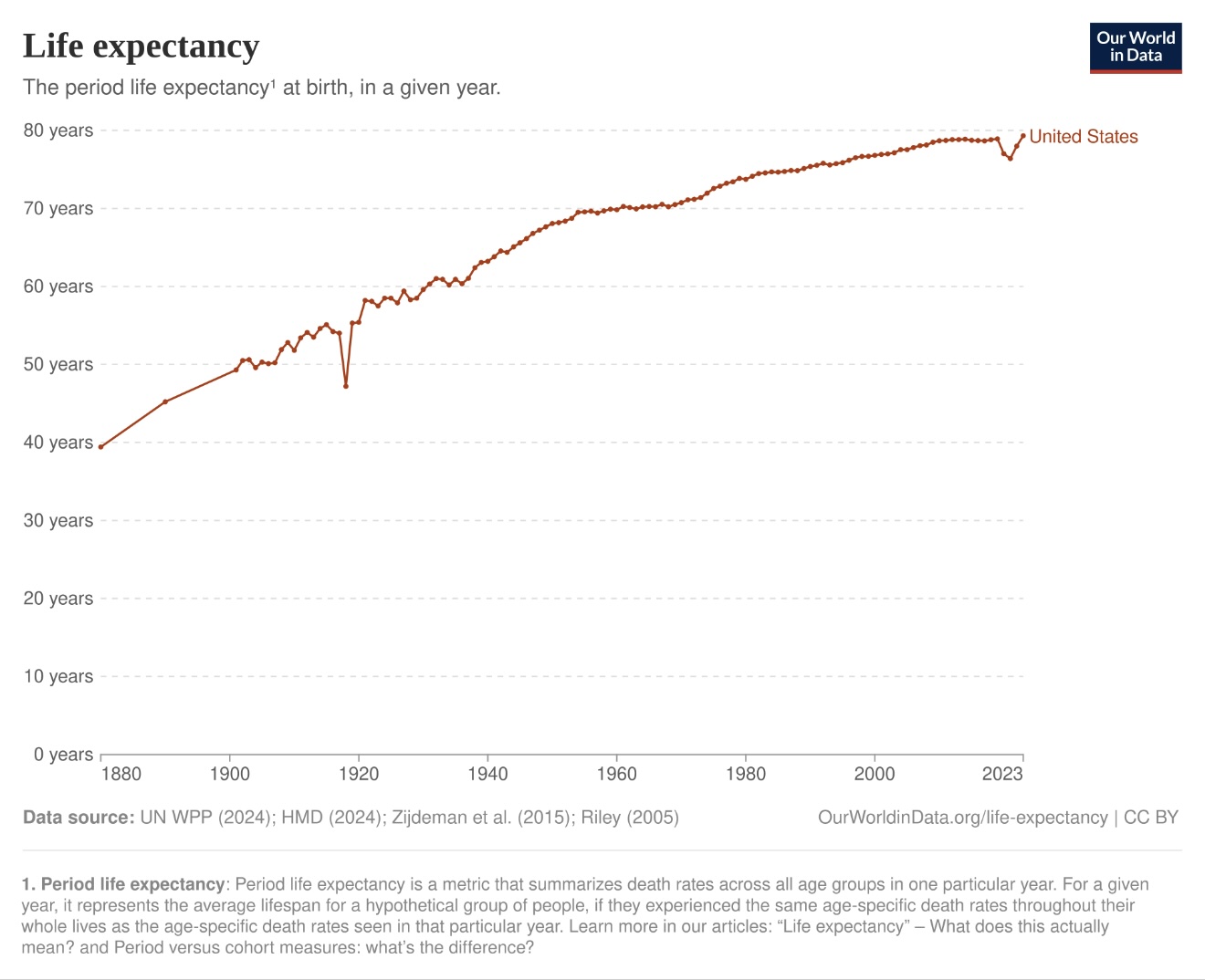

This transition placed more responsibility on individuals to save, invest, and manage their retirement strategies. While 401(k)s offer flexibility and investment opportunities, they also carry risks including market volatility and potential for loss, which should be carefully managed. On top of that, Americans today must also plan around inflation, healthcare costs, tax strategies, and longer life expectancies when preparing for retirement.

Modern retirement is no longer a one-size-fits-all concept. Some people retire fully, while others continue working part-time, start businesses, or pursue second careers. The definition of retirement continues evolving alongside changes in technology, healthcare, and the economy.

As retirement planning becomes increasingly complex, having a long-term financial strategy is more important than ever. That’s where experienced financial guidance can make a meaningful difference.

As advisors, we have the fiduciary duty to act in our client’s best interest by helping individuals and families build personalized retirement strategies designed around their goals, lifestyle, and future needs. Whether you are just beginning to save, approaching retirement, or already retired, our team can help you navigate key decisions involving retirement income planning, investment management, tax-efficient strategies, risk management, and wealth preservation.

As America celebrates 250 years of progress and innovation, retirement planning continues to evolve. Systems may have changed from family farms to pensions to 401(k)s, but the core objective remains the same: achieving financial security and peace of mind for the future.

Source: Period Life Expectancy

Source: The Evolution of U.S. Retirement Savings Accounts

Source: Transition from Pensions to 401(k)s

Additional Sources: