Why 8(%) May Not Be Great

We love to hear our clients taking the initiative to learn more about their personal finances and to educate themselves and while we hope Meridian provides more than enough content to do so, we know there are many other sources and opinions out there.

This may be a bit of a controversial topic as we know many people listen to and follow a certain financial radio personality (which will remain nameless) who is known for his reputation on principles like living debt-free and investing wisely. However, his advice on certain investment strategies, including those involving high withdrawal rates, has faced scrutiny. In particular, his perspective on the 8% distribution rate warrants a closer look. In this blog, I will cover what the 8% rate signifies, why investors should care, why the 8% distribution rate theory might be problematic, and what investors should consider instead.

What is the 8% Withdrawal Rate?

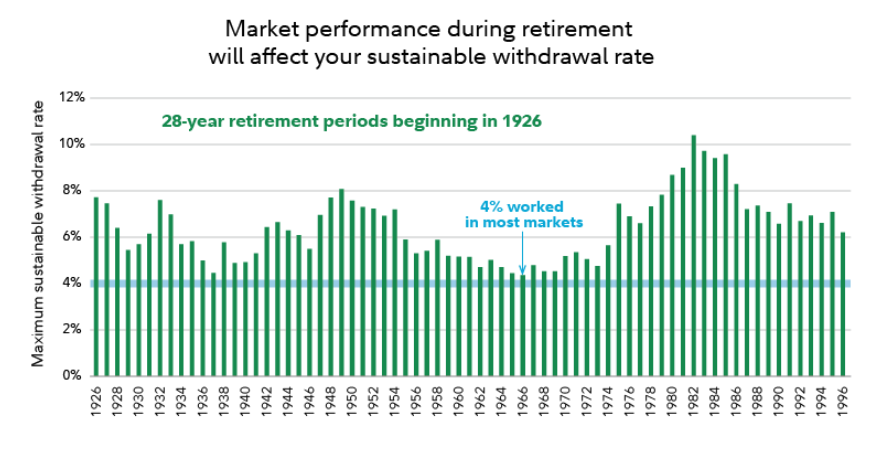

The 8% withdrawal rate is based on a theory that an investor in retirement can safely withdraw 8% of their retirement savings annually assuming 12% expected stock returns minus 4% inflation. This is predicated on the assumption that the portfolio is invested in 100% equities/stocks, which as we well know, is not the most appropriate or prudent allocation for every investor. This is obviously much different than the widely known 4% rule, which recommends spending no more than 4% of your investments during the first year of retirement and then adjusting the total every year to account for inflation.

Source: https://www.fidelity.com/viewpoints/retirement/how-long-will-savings-last

Risks with the 8% Withdrawal Rate

- Longevity Risk: One of the biggest concerns with an 8% withdrawal rate is the risk of outliving your savings. Retirement can last 20, 30, or even 40 years, and withdrawing 8% annually increases the likelihood of running out of funds, especially if your investments don’t perform as expected or if you encounter unexpected expenses.

- Investment Performance: The 8% withdrawal rate assumes that your investments will consistently provide high returns, which is not always the case. Market fluctuations, economic downturns, and changes in investment performance can affect your portfolio’s ability to sustain high withdrawals over time. As mentioned earlier, this theory is based on 8% inflation-adjusted returns; however, over the last decade the S&P 500s inflation-adjusted return falls around 7%.

- Sequence of Returns Risk: The order in which you experience investment returns can greatly impact your retirement savings. A period of poor returns early in retirement, combined with high withdrawals, can deplete your savings faster than anticipated. This is particularly concerning with a high withdrawal rate like 8%.

Adapting Withdrawal Strategies

While the 4% rule is a widely accepted guideline, individual circumstances vary. Here’s how you can adapt withdrawal strategies to fit your unique situation:

- Personalized Planning: Work with a financial advisor to create a personalized retirement plan based on your specific needs, goals, and risk tolerance. A financial advisor can help you adjust your withdrawal rate based on your lifestyle, expected expenses, and investment portfolio.

- Dynamic Withdrawals: Consider a dynamic withdrawal strategy where you adjust your withdrawals based on market performance and changes in your financial situation. This approach allows for flexibility and helps manage the sequence of returns risk.

- Investment Diversification: Maintain a well-diversified investment portfolio to mitigate risks and improve the chances of stable returns. Diversification can help protect against market volatility and improve the sustainability of your withdrawals.

- Regular Reviews: Regularly review and adjust your retirement plan to ensure it remains aligned with your goals and market conditions. Monitoring your investments and spending habits can help you make informed decisions and adapt to changing circumstances.

The suggestion of an 8% withdrawal rate might seem appealing for those seeking higher income during retirement, but it comes with significant risks, including the potential for depleting your savings too quickly. A more conservative approach, such as the 4% rule, provides a higher probability of sustaining your funds throughout retirement.

Ultimately, a successful retirement strategy involves personalized planning, diversification, and regular adjustments. By considering alternative withdrawal strategies and seeking professional advice, you can better ensure a financially secure and fulfilling retirement.

Last week I got to experience deep sea fishing off the coast of North Carolina with some friends and much like sustaining funds in retirement, I learned a thing or two about sustaining strength while reeling in a sailfish and several Mahi Mahi!

And for anyone wondering, I learned the flag is supposed to be upside down as that signifies a catch and release.