2016 is Not Over (For Some Types of Retirement Plan Contributions)

As the year turns over to 2017, it seems that the “internet” is happy to be saying goodbye to 2016. I am not completely sure the exact reason or reasons why, but the popular sentiment seems to be that 2016 was a “bad year.” I am certain many good things happened to many people, but negativity often moves the needle and gets people talking and commenting. Everyone seemed to agree that Mariah Carey’s performance (or lack thereof) on New Year’s Eve perfectly summed up the year. Just in case you have somehow missed this story, here’s a good summary from The Washington Post. I think a lot of credit needs to be given to the back-up dancers, who seemed unfazed but the “audio malfunction!”

There may be at least one good reason why we shouldn’t let 2016 fade into the rearview mirror so quickly: retirement plan contributions. Up until April 15th of this year (or your tax filing deadline), you are still allowed to make contributions to some types of IRAs and count them for 2016. This option can be especially helpful if you are a small business or a sole proprietor, and you do not have a 401(k) or other type of plan into which you have made recurring contributions over the past year. Not only will contributing to IRAs help you save for retirement, but it could also provide you with a tax deduction if you need one.

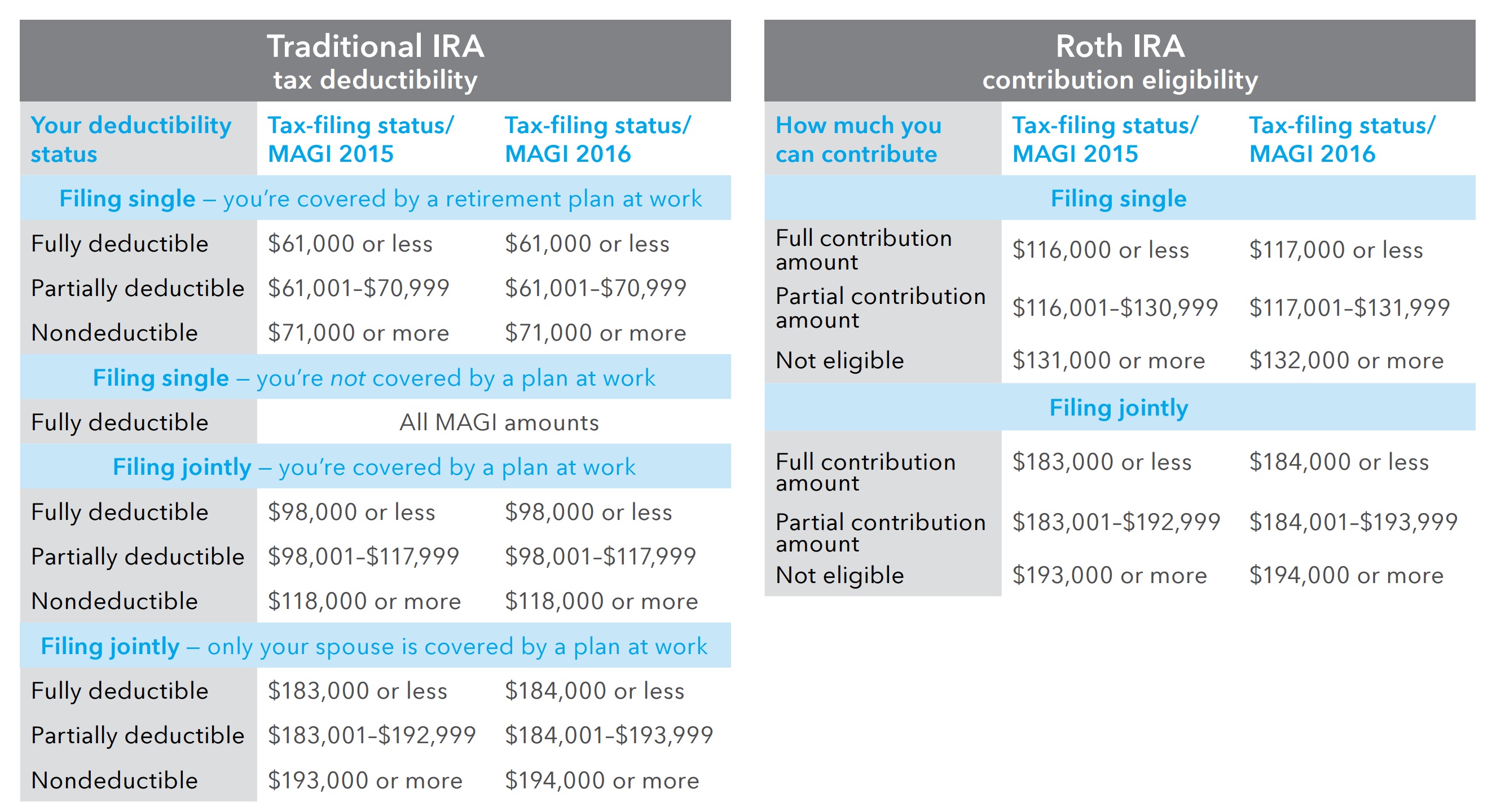

As usual, there are limits and restrictions that the IRS gives us. Whether or not you are already covered by a plan at work, your income level, and your tax filing status (single, married, etc.) are all things considered when it comes to your options. Here’s a chart from American Funds that gives a good summary of what you can and can’t do with both Traditional and ROTH IRAs. Please note that MAGI stands for Modified Adjusted Gross Income.

If you are under 50, you can contribute up to $5,500 to an IRA, and for those over 50, you are allowed an additional $1,000 catch-up contribution.

For a small business or sole proprietor, a SEP IRA might be a particularly good option. The contribution limits are much higher, and your ability to contribute is not limited by your spouse’s plan options. For 2016, you can contribute up to 25% of compensation or $53,000, whichever is less. Please note that if you do have employees, you/your company are required to contribute the same percentage of compensation that you give yourself. For example, if your compensation was $100,000 in 2016, you could contribute up to $25,000 to a SEP IRA (25% of $100k). If you have a full-time assistant that received $30,000 in compensation, then you/your company would also need to add $7,500 to his or her SEP IRA (25% of $30k).

As always, consulting a tax advisor on the best option for your situation is a great idea. Just keep in mind that just because 2016 is officially over, it might not be over for your retirement savings options.

All the best to you and yours in 2017!