Introducing Baby Grace!

For those of you who may not have known, our client service specialist, Gretchen gave birth to a beautiful and healthy baby girl in April! While Nathan and I are struggling to keep up with all that Gretchen does around Meridian (she does a great job of keeping our office organized and us on track…), we are so happy to have a new little member of the Meridian family.

And Gretchen, being the amazing planner and supreme organizer that she is, has already started planning and saving for Baby Grace’s future.

For Virginia parents, 529 college savings accounts are one of the best vehicles for saving for future college expenses. Each state has their own 529 plans, but they all share these common characteristics:

- Earnings on the money contributed to the plans is tax free if used for qualified education expenses. Some states allow a state income tax deduction for contributions to 529 plans as well.

- The money in the college savings account can be used at eligible institutions around the country for tuition, room, board, books, and computers.

- Others, such as grandparents or friends, can contribute to the savings accounts.

- The owner of the college savings account can change the beneficiary of the account as plans change.

In Virginia, there are three programs:

- CollegeAmerica: This plan is sold through a broker and uses American funds. The broker receives commissions based on the funds selected to implement the savings program. The American Funds family is a well respected fund family, yet its costs are a little higher than the other two Virginia choices.

- Prepaid529: This plan takes the guesswork out of how much college tuition will cost for your child. Each Prepaid 529 semester purchased will cover one future semester of in-state tuition and mandatory fees at Virginia public colleges and universities. You are able to buy from one to ten semesters and make payments by either a one time lump sum, monthly payments, or a combination of both. You must buy the semesters before your child reaches 10th The one hazard of this plan is that you may use the semester credits at private or out of state colleges, but you are not guaranteed that the tuition for the semester will be paid in full—it may only cover a fraction of the tuition. For that reason, this plan is best used with students who are relatively certain to stay in state—or in combination with another college savings vehicle.

- Invest529: This plan is one of our favorites…low cost and broadly diversified, the Virginia Invest529 has achieved a Gold rating from independent analyst firm Morningstar. In this account, you can add money in a lump sum, or in payments as low as $25/month. You pick from a well rounded line up of mutual funds—or you can use an age-based target portfolio. We really like these portfolios as all that you need to do is select the portfolio closest to the date that your child will begin attending college. As an example, Baby Grace will attend college in 2035, so Gretchen should choose the 2036 portfolio. This portfolio starts off very aggressive, with a large allocation to stocks. As Baby Grace gets closer and closer to graduating from high school, the portfolio automatically rebalances to get more steady and stable in preparation for upcoming withdrawals. It is the ultimate “crock pot” portfolio—you just set it and forget it.

Gretchen is an amazing mother in so many ways (she’s doing cloth diapers, folks!!)—and we are really proud to see her thinking ahead and planning for Grace’s future. As the Virginia 529 program site points out, the earlier you start planning, the easier it is to save—so give us a call if you need any help!

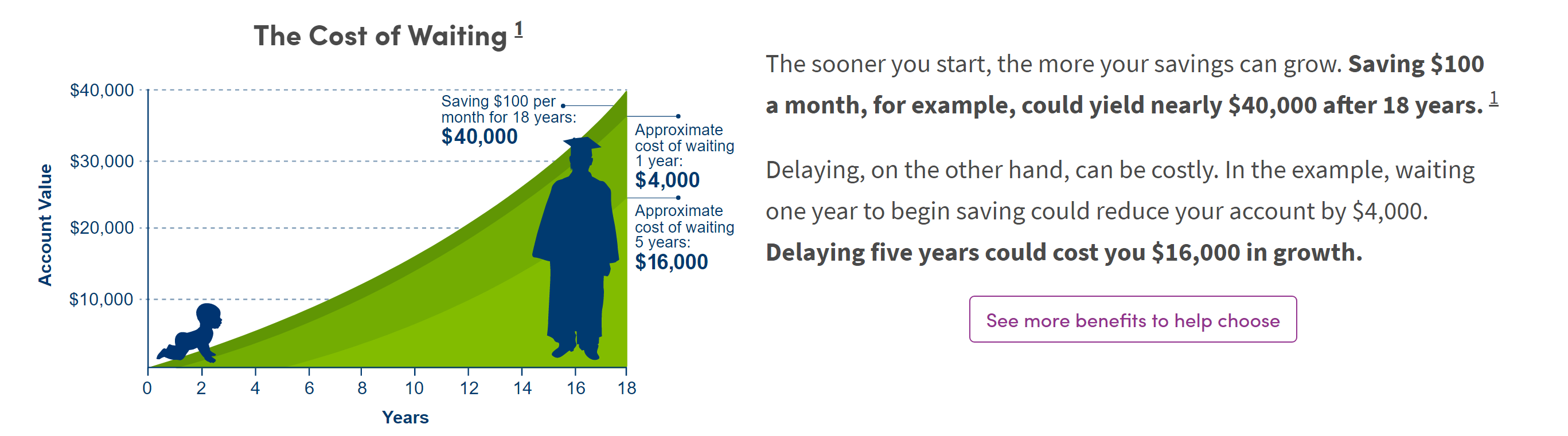

- This chart is for illustrative purposes only and is not intended to reflect actual performance of any specific investment. Assumes interest rate of 6.25 percent compounded monthly. The value of your Virginia529 account will vary depending on market conditions and the performance of the investment option you select, and it may be more or less than the amount you deposited. You could lose money – including the principal you invest – or not make money if you invest in one of these programs. Past performance of investments is not an indicator of future returns.↩