The Individual Medley

As a relatively new “swim parent,” I have learned a lot about swimming and swim meets in general. For those of you experienced swim parents, you are probably doing a combination of cringing and smiling right now; cringing at all of the early morning practices and smiling at all of the great experiences for both you and your child(ren).

My son Coleman (age 7), has really enjoyed his time with the Evergreen Barracudas swim team, and he has been able to contribute here and there as he improves. As is tradition, the older kids watch out for and help coach the younger kids. We are very fortunate to have some great role models for our young children, and I am very thankful for their patience and kindness.

As is typical with any new sport, improvements can come pretty quickly, but even I was impressed at Coleman’s recent time improvement in his Individual Medley this past weekend (yes, I am also a very biased dad!). For those of you not aware, the IM is all four strokes in one event – backstroke, breaststroke, butterfly, and freestyle. While his time was unofficial as he was DQ’d for a minor infraction (noted as “alternating kick – fly”…come on! He’s 7! 😊), he reduced his time by a whopping 40 seconds! That’s pretty amazing when you consider it probably took him about that long to go one length of the pool a month ago.

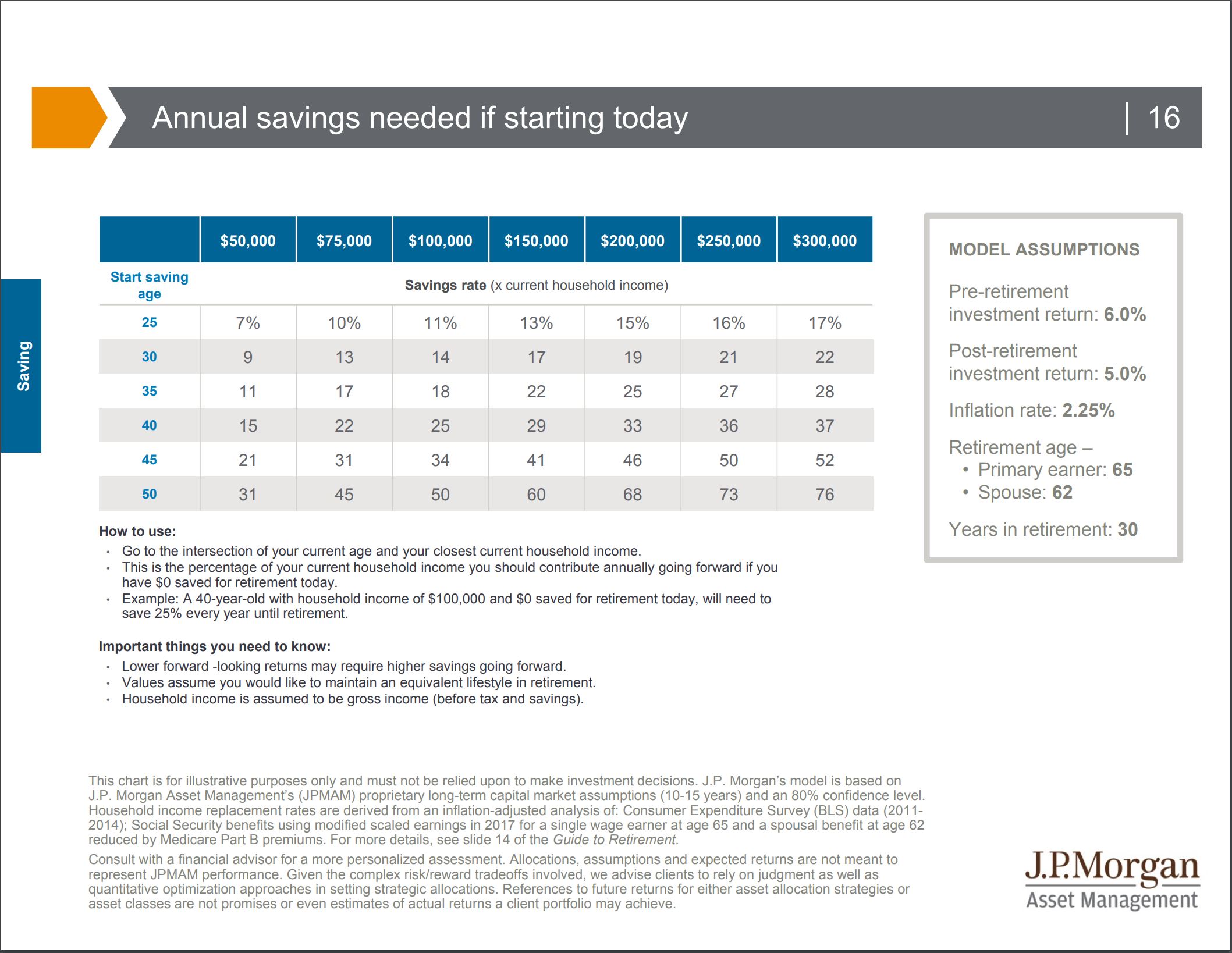

Most time improvements are just incrementally better from week to week, and I am sure that will be the case with Coleman as he gets older and continues to improve. Incremental improvements are what we should strive for when contributing to company retirement plans as well. Whether you are investing in the government Thrift Savings Plan (TSP), a 401(k), or other type of plan, you should strive for incremental increases in how much you contribute. Not contributing enough or at all could make catching up later in life virtually impossible. JP Morgan puts out an annual Guide to Retirement, and the chart below gives you an idea of what percentage of your salary you should be saving at a given age.

If you are not contributing enough based on the above chart, do NOT be discouraged! Instead, try for incremental increases in your percentage. This way, it won’t feel like a drastic change to your paycheck, and my guess is that you will barely even notice the difference (since most contributions are before taxes). Got a raise? Give your retirement contributions a raise too! And, by the way, if your company is matching some of your contributions, you can count that as part of the recommended savings rate too.

See how much you can bump up your savings rate over time, and try not to get DQ’d while saving for your own retirement!

And, to the parent who disqualified this little guy, I will show you an “alternating kick…..” sorry, biased-angry-swim dad talking!