Lucky Break

While even the IRS is scrambling to figure out how to comply with the new tax act—one portion of the new bill does seem clear, and is a really nice gift for parents and grandparents of students. The new tax act allows 529 plan distributions for any eligible education expenses of K-12 education—not just the previous restriction of higher education expenses only. This means that up to $10,000 a year of any eligible elementary, middle school, high school, or home school expense can be paid from any 529 account. Your tween need a computer for 6th grade papers? That is a qualified expense. You had to buy books or pay supply fees? Also a qualified expense. Pretty cool.

Here is a list of eligible expenses:

Source: Fidelity

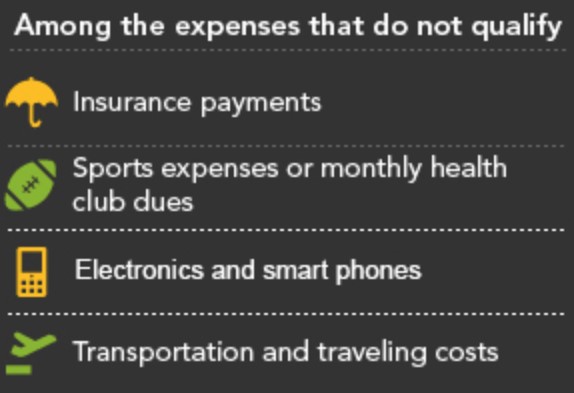

Here is a list of items that are NOT eligible expenses:

Source: Fidelity

This new feature of 529 plans helps Virginia parents that homeschool or send their kids to private school. Previously, all of those costs were paid with dollars that had been taxed by both the Federal government and Virginia. Now, by simply opening a Virginia 529 account, those expenses can now be paid with dollars that are exempt from Virginia income taxes.

Virginia is also unique in that the state 529 plan allows up to $4,000 of contributions per account to be deducted from Virginia income tax. So, in theory, in a family of four with two kids and two parents, each parent could open a 529 account for each child (for a total of four 529 accounts) and deduct up to $4,000 per each account (or $16,000 total!) on their Virginia income tax return.

If you do have education expenses for your K-12 student that could be paid from a Virginia 529 account (tuition, books, supplies), we recommend that you open a separate 529 account (as opposed to just using the 529 account designated for college savings). The main reason is that the time horizon for investing the account is much different. If you send your 3rd grader to private school and want to use a 529 account to pay their current tuition, the account should be invested very conservatively, if at all (we would recommend using the stable value or FDIC insured option). Meanwhile, the college 529 account for your 3rd grader should be invested fairly aggressively since they don’t head to college for almost a decade.

Already, there have been loud complaints about this new policy, so we are not sure how long it will last. But, for now, it is a cool planning opportunity for Virginia parents and grandparents!