Let’s Get Digital…Digital…

Nathan always references cool songs in his blogs—the only one that came to mind for this blog was Olivia Newton-John’s “Physical”. Not exactly a cool song, but I digress…

Recently, I followed our usual Meridian advice to clients and started to review our own estate plan. I hadn’t really looked at it since Melanie was born, so Jonathan and I pulled it out and realized we needed to update several things, especially given both the tax law and state law changes. One of the most significant changes that had occurred since we first drafted these documents in 2011 was the proliferation of digital assets.

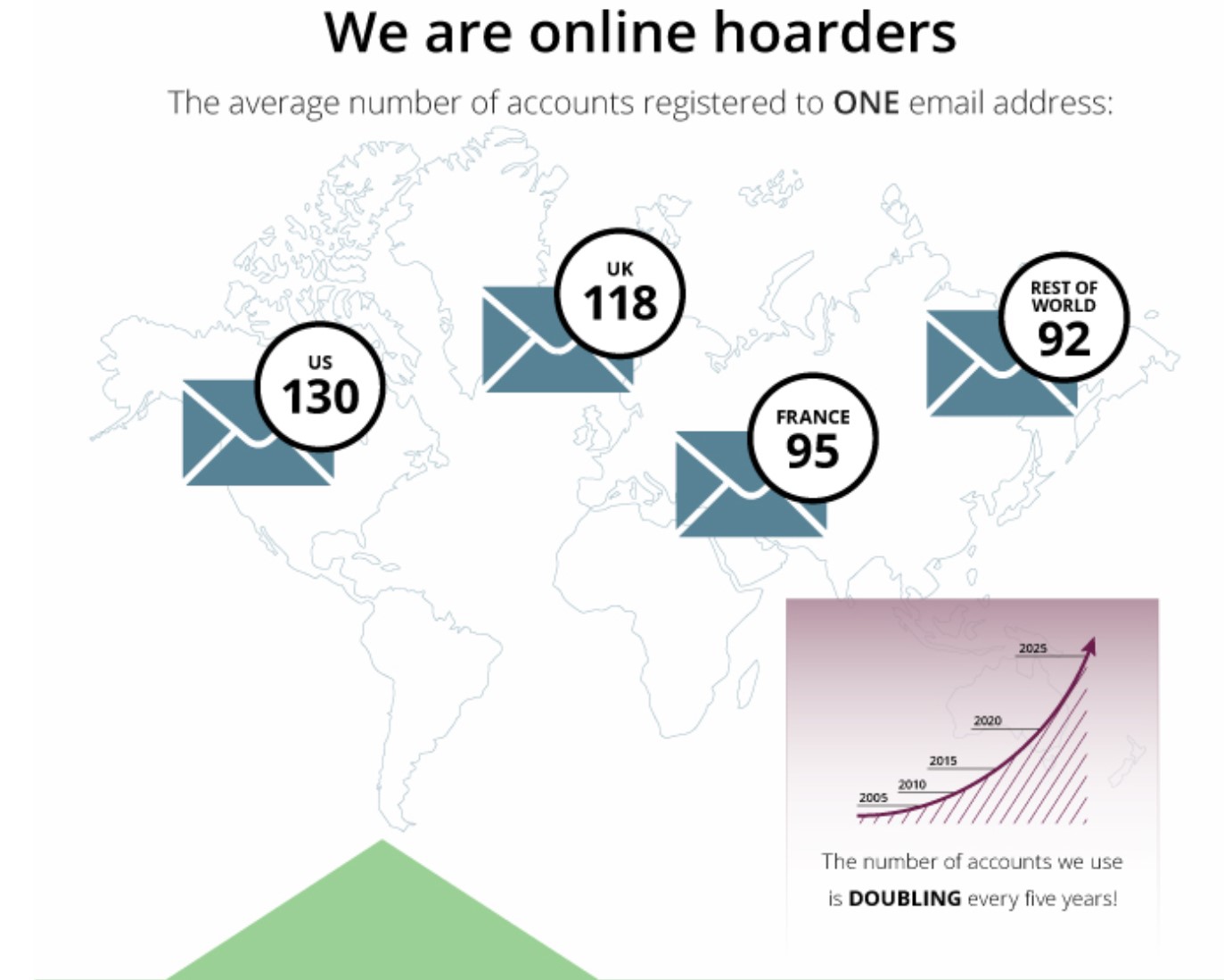

Back when we had first drafted our estate plan, it was mostly concerned with physical assets—our house, our car, our money. But now, less than a decade later, many of our assets our purely digital—like our photos, music library, books, PayPal account, social media accounts, blogs, Dropbox account, hotel and airline rewards, contact information, etc. According to one study, the average American has about 130 online accounts—and this number is estimated to double every five years!

With these digital assets, the Terms of Service agreement—that long legal section that we blithely scroll past to check “I Agree” so we can get on with accessing the service—has dictated the disposition of these assets when the account owner is incapacitated or dies. Many terminate the account immediately upon notification of death or disability. In a recent case, Apple required a court order to allow a widow to access her deceased husband’s iPhone.

The variation between the various digital asset platforms led to the passage of the Revised Uniform Fiduciary Access to Digital Asset Act—or RUFADAA for short… 😊

RUFADAA has been adopted in 38 states, including Virginia, and the law allows an agent, attorney-in-fact, executor, trustee, or guardian to obtain information from the companies that hold digital assets (now called “custodians” under the act) about your accounts. Additionally, if properly drafted, the power of attorney document, will, or trust can enable a your fiduciary to manage your digital assets on your behalf. Interestingly, these documents will trump the provider/custodian’s Terms of Service agreement.

This is all good news as we continue to migrate more and more of our valuable assets from the physical to digital space. In order to plan well for these assets, here are a few steps that you may want to consider:

- Create an inventory—it is hard for surviving family or named fiduciaries to track down all of your digital assets if they don’t know where to start looking. While it may be difficult now to name all 130 online accounts that you have, at least beginning with a list of some of the most important accounts (email, pictures, music, anything of value…) is a great start. At Meridian, we have a digital asset inventory form for our clients to use—let us know if you’d like a copy and we are happy to send it to you.

- Consider using a password manager—using a program to maintain login credentials could provide added security (because of the ability to use complex passwords) as well as provide a master list of online accounts for family members. Many of these password systems will allow a user to name a trusted person in the event of an emergency. Although, the downside to these systems is a full hack of the manager itself!

- Revise your estate planning document to incorporate RUFADAA provisions—we defer to the estate planning attorneys on this one, but it may make sense to incorporate some of the new law into your revised estate planning documents to allow greater flexibility.