Smart Saving for Kids: How to Use 529 Plans, Custodial Roth IRAs, and Custodial Accounts

As Sarah mentioned in her blog last week, April is Financial Literacy Month! This annual observance aims to raise public awareness about the importance of financial literacy and encourage smart money management habits. As with so many habits, starting good money management and savings habits young is a great way to ensure they stick. One of the best gifts you can give your children is the gift of savings – below are a few vehicles parents can use to set their children up for future success.

529

A 529 plan is a state-sponsored, tax-advantaged education savings account that offers tax benefits and spending options.

Most states allow for a state tax deduction if you contribute to a plan in that state 529. For our Virginia residents, the Virginia 529 plan allows up to a $4,000 state tax deduction per account (even if the beneficiary (aka the child) has more than one 529) no matter if you invest in the Invest plan or the Prepaid plan. The contribution has to be made before the end of the calendar year to qualify for that year’s state tax deduction. Click here for a comprehensive list of all state plans and their corresponding state tax deduction eligibility.

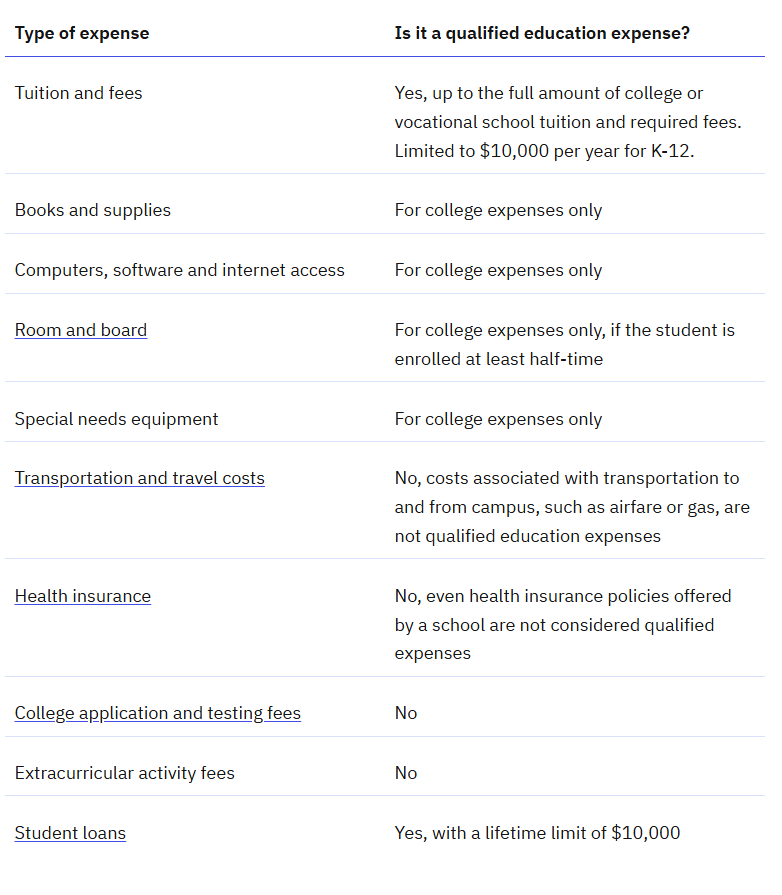

Funds grow tax-deferred AND are withdrawn tax free if used for qualified education expenses. (That’s a triple tax benefit if your state plan offers deductions on contributions.) If used for K-12 expenses, this is limited to $10,000. Anything that is not a qualified education expense will incur federal and possibly state tax on the earnings, plus an additional 10% federal tax on those earnings. Below is a good chart highlighting what is and is not a qualified expense.

https://www.savingforcollege.com/article/what-you-can-pay-for-with-a-529-plan

The Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 and the SECURE 2.0 Act of 2022 permitted 529 funds to be used for student loan repayment, up to $10,000 in student loan debt repayment for account beneficiaries and their siblings. Further, the SECURE Acts allows up to $35,000 of leftover funds in a 529 account can be rolled over into a Roth individual retirement account (IRA), provided the 529 account is at least 15 years old.

Personally, I really like to contribute to my friend’s children’s 529s for their birthdays, in lieu of getting them toys. Most plans have a link that can be sent directly to friends and family, or you can purchase 529 gift cards.

Custodial Roths

Custodial Roths are my favorite and I encourage everyone with children earning income to open one for their child. A custodial Roth IRA is a Roth individual retirement account that is owned by a minor but controlled by an adult until the minor reaches legal adulthood. The rules of a custodial Roth IRA follow the same parameters and IRS guidelines as a typical Roth IRA.

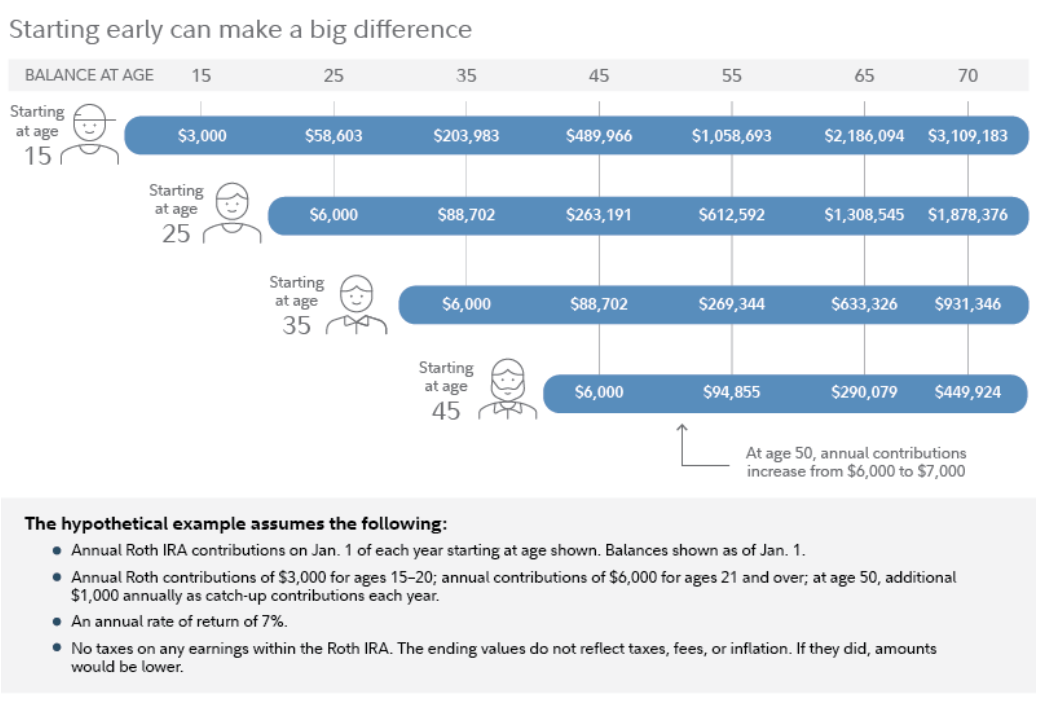

In Virginia, a child as young as 14 can apply for a work permit and start earning “real” income (vs. side cash jobs that younger kids might engage in). If you have a working minor in your household, assisting him or her with setting up a Custodial Roth may provide a wonderful head start toward saving for retirement. It’s hard to think about a 14-year-old saving for something that may be 50+ years away, but as with any investing, the longer the better. Starting early allows you to benefit from compound interest, making it easier to accumulate a substantial fund over time. These kinds of accounts are also great options for grandparents to open as well.

Just like the rest of us, minors have a limit on contributions of $7,000 per year or the minor’s total income for the year, whichever is less. So, if a child earns $2,000 working a summer job, the maximum contribution would be $2,000.

When the child reaches the age of 18, the account is converted into a Roth IRA in just their name and they can continue contributing to it throughout their life. It’s a great head start to saving for retirement!

Custodial Accounts

Like a Custodial Roth, Custodial investment accounts are opened on behalf of a minor (under the age of 18) and while the child technically owns the assets in the account, the adult serves as the custodian, making decisions, like managing contributions and making investment choices, on behalf of the child. These accounts are a good way for parents to save for their children without some of the restrictions of 529s or Custodial Roths. Withdrawals can be made at any time, as long as they are for the benefit of the minor.

It is worth noting that one of the drawbacks of using a custodial account, however, is that it can make the recipient less eligible for need-based college scholarship programs and other such initiatives as the assets in the account are owned by the minor.

The account becomes theirs when the child turns age of majority. The age of majority is typically 18 or 21 years old, depending on the laws of the state of residence. In Virginia, the custodian can select the age of majority for the account, it can be 18, 21, or 25.

All that to say, save early and save often! Increasing your children’s financial literacy and building savings in different vehicles can help set them up for success in the future.