Are We There Yet?

As I write this, we are packing up to head out on a small road trip to visit friends and clients. Thankfully, with electronic devices, our kids are mostly self-entertained on the road, but invariably—about an hour into the trip–the littlest will pull out the age old question—”are we there yet?”

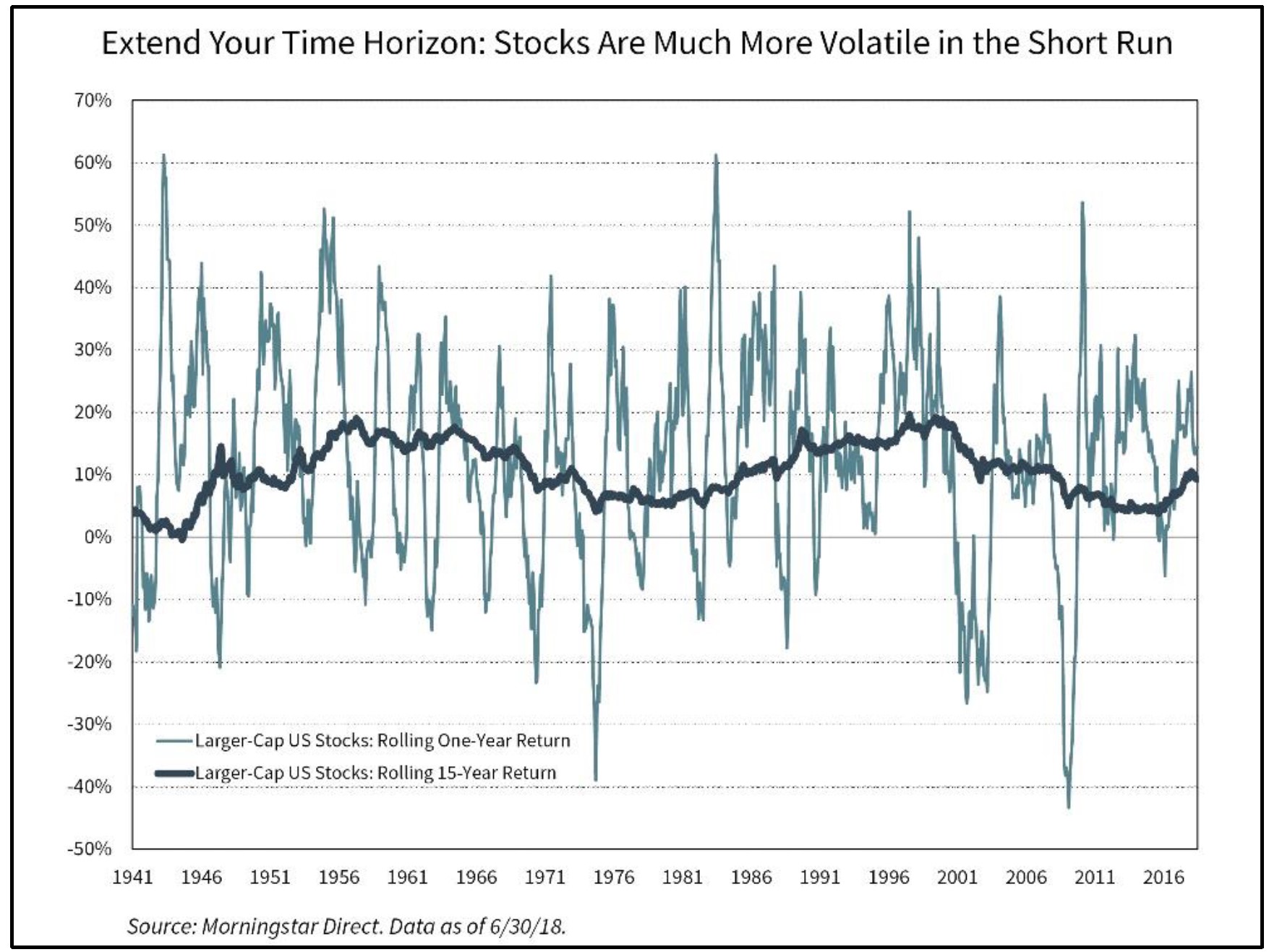

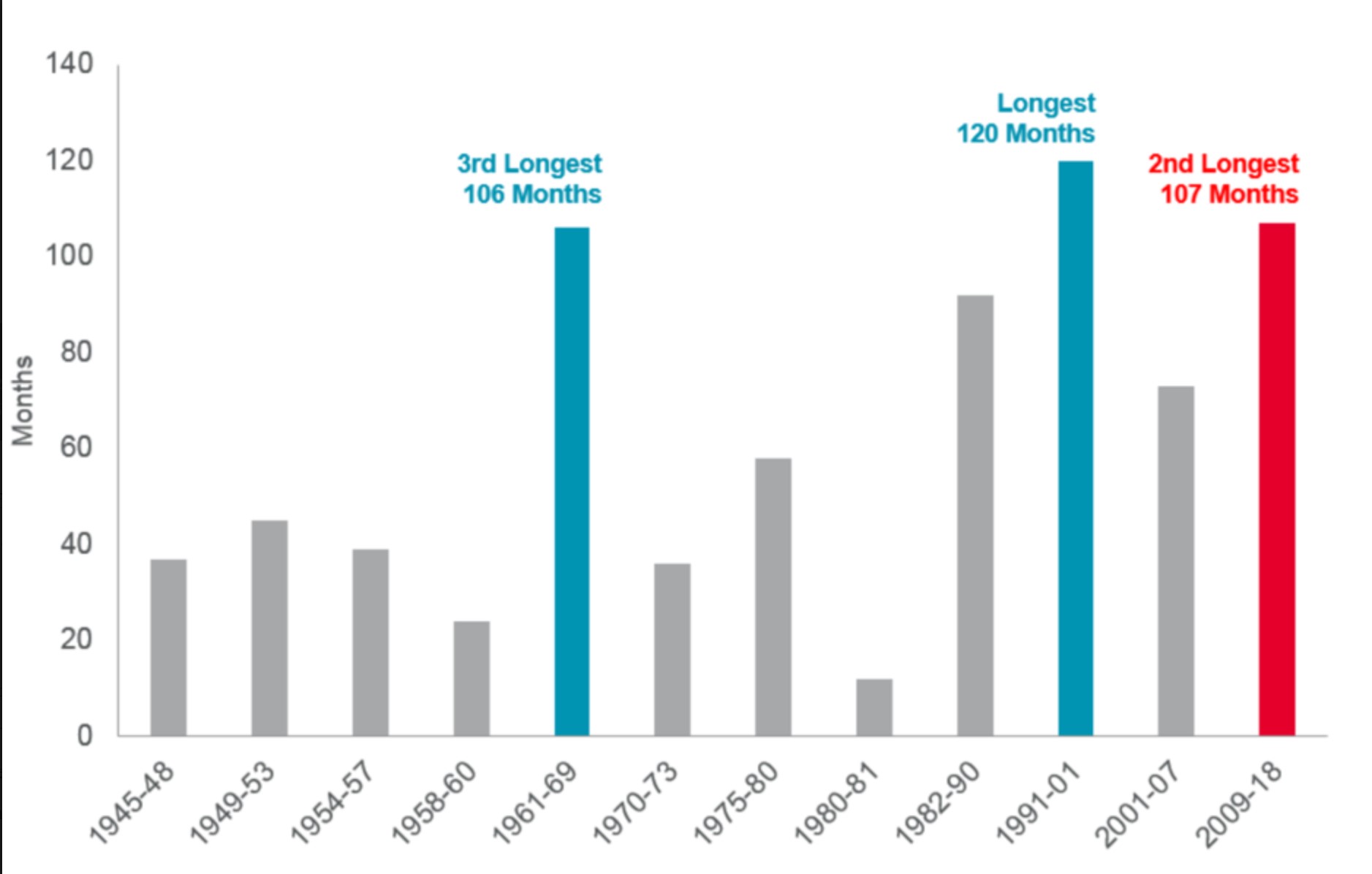

We are sort of asking the same question about our stock market—it’s been a long trip—one of the longest recoveries in history:

And that has many of us asking—are we getting close to the end?

At Meridian, we do not believe anyone can accurately predict the end of an economic cycle unless they have the benefit of hindsight. But, here are a few things that we have been keeping an eye on:

- The yield curve—historically, the yield curve (the curve of short term rates to long term rates) has been a good predictor of recessions. In the past, when short term interest rates are higher than long term interest rates, a recession has followed in the next 2 years.

At this moment, we are not yet inverted, but are getting closer:

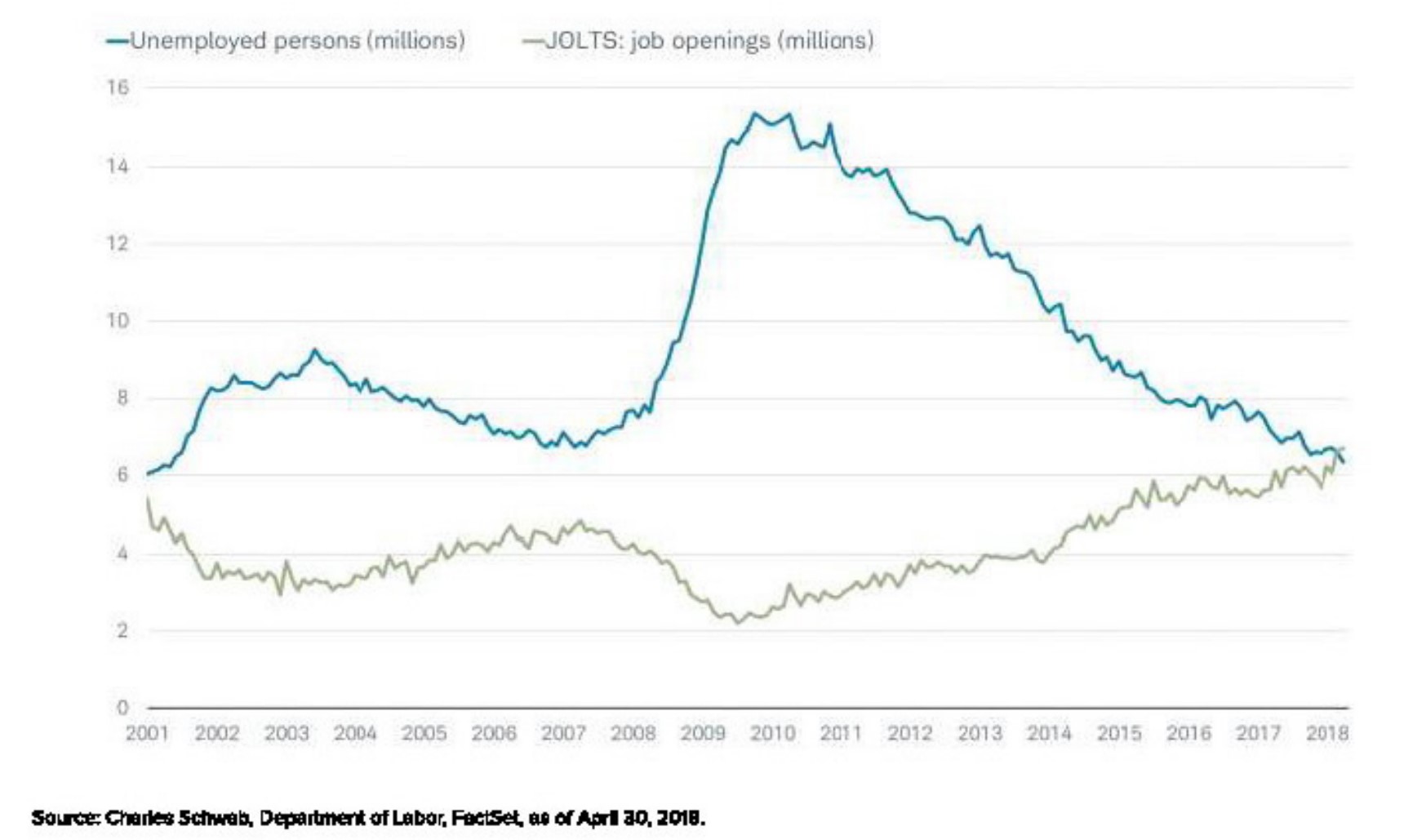

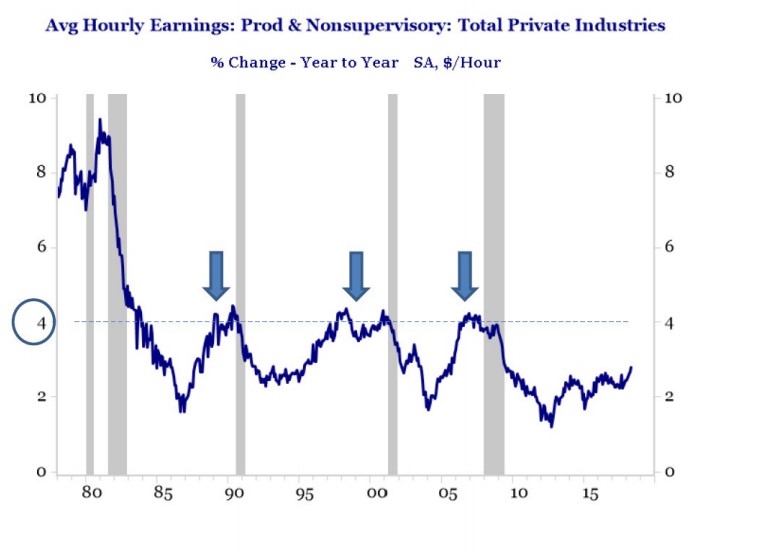

- Unemployment and wages—typically layoffs precede recessions. As good employees get harder and harder to find, companies have to pay more to attract workers. As they pay more, their margins shrink and their profitability drops. To attempt to maintain their profitability, companies begin rounds of layoffs.

Currently, there are more job openings than there are unemployed people in America for the first time since 2000:

So, we are finally seeing wages beginning to increase, although slightly:

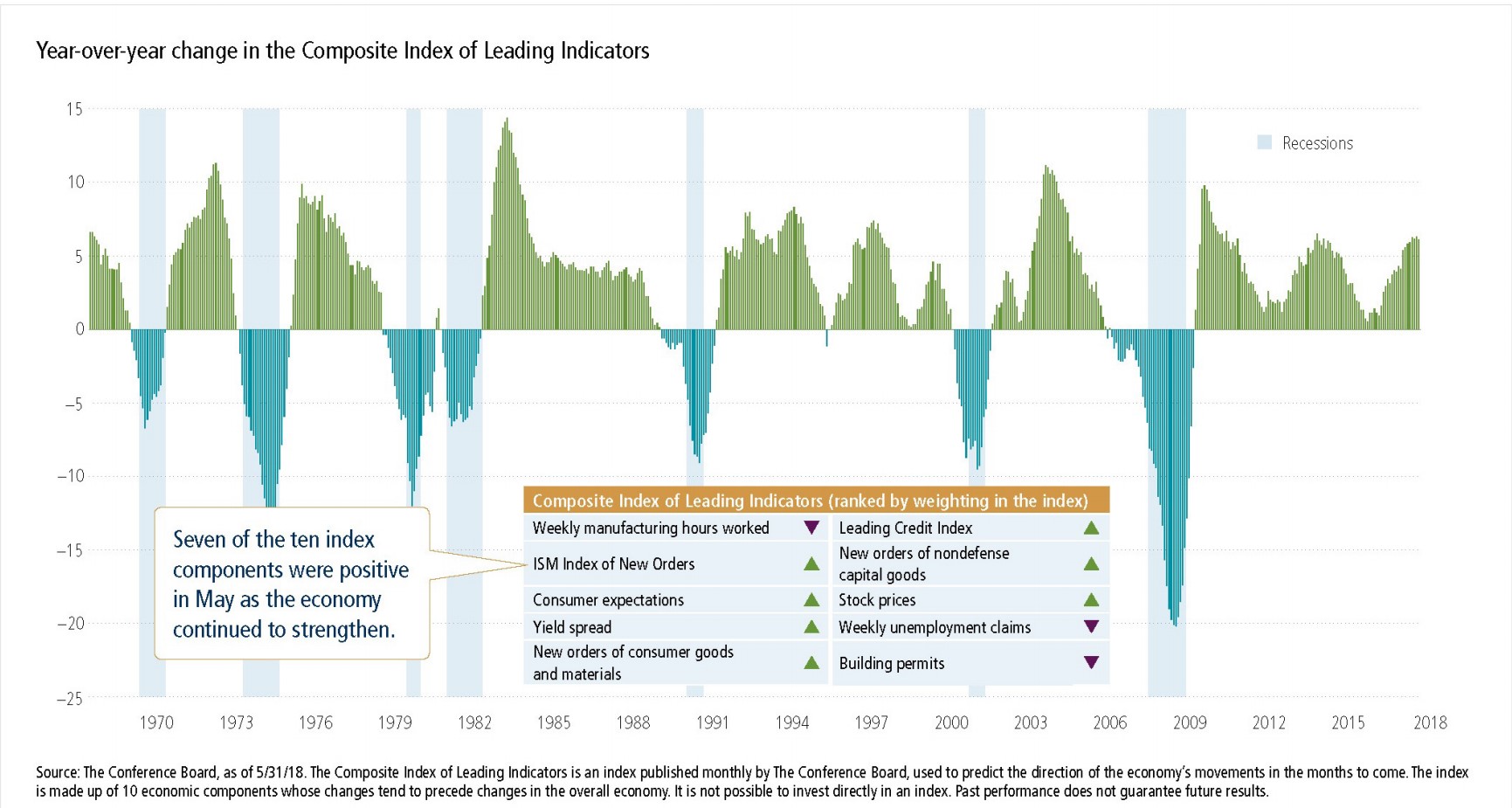

- Leading indicators—traditionally, there are about ten economic indicators that tend to change before a recessionary period. These are data points like new house building permits or new unemployment claims.

As of June 30, the composite of leading indicators grew again, indicating continued strength in the US economy, however at lower and lower levels than in the past:

Interestingly, much has been made of the recent news that U.S. GDP (gross domestic product) grew 4% for the year ending June 30, 2018. While this is undoubtedly a solid number, GDP is a lagging indicator—which means that this number just confirms the growth we’ve already have. Placing too much significant on the predictive nature of this number would be akin to driving by looking in the rearview mirror—not too helpful.

Given all of the economic data that has been published in July for the period ending June 30, 2018, it does appear that the U.S economy is in the second half of its expansion. In past expansions, this has meant:

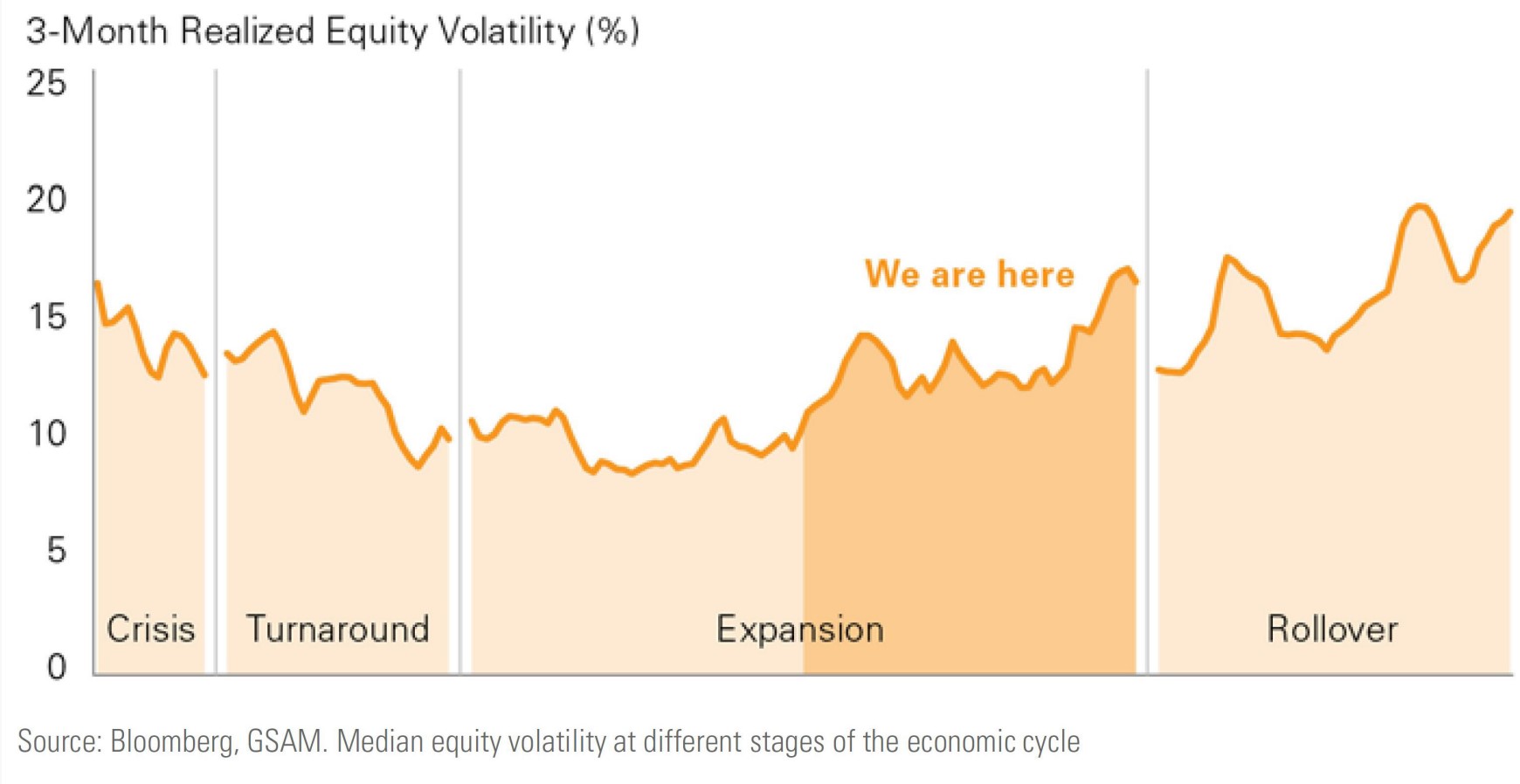

- Increased volatility—enough said:

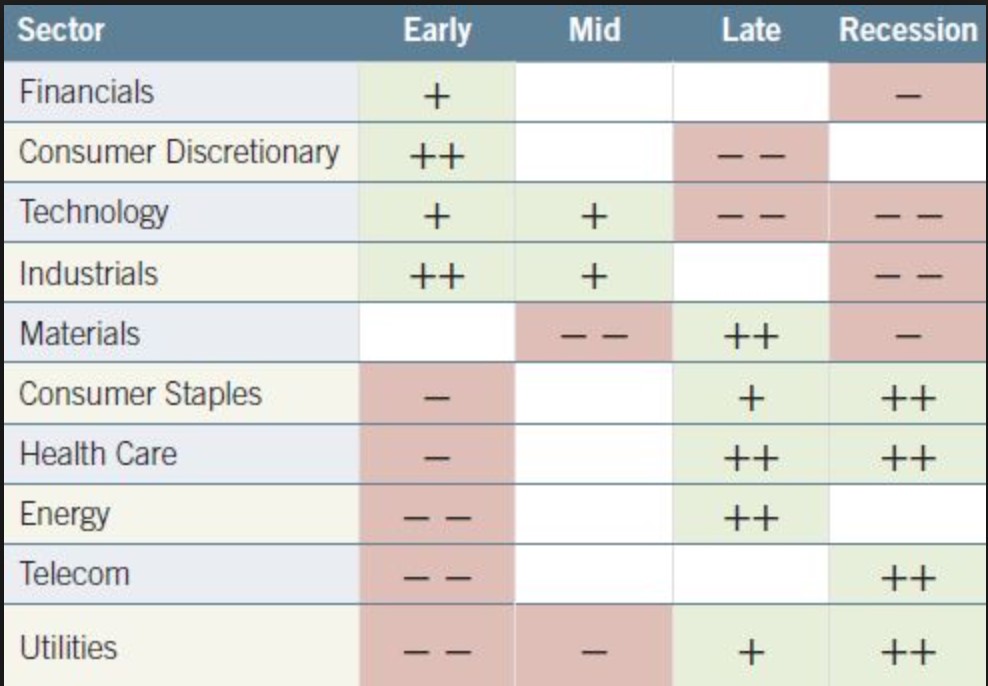

- Potential for more gains in the stock market—according to research by Fidelity, the average stock market return during the late cycle economic phase is about 5% on average. Additionally, Fidelity points out that some sectors thrive more than others at the end of an economic cycle:

So, what do we do with all this? It appears that we may indeed be getting close to the end of this stock market ride, although the exact timeline is absolutely fluid. We should buckle our seatbelts as the ride will most likely be a little bumpy, but we should not hop off the ride early either.

Instead, revisit your asset allocation and de-risk where possible. Stay diversified and patient. Despite the volatility, remain disciplined. And, when it starts to look pretty scary, remember to widen your perspective…everything looks different with more time: