Finding the Balance in Rebalance

More so now than ever do I believe the theme of “finding balance” is playing a key role in all of our lives. The economy, financial markets, and life itself seem anything but in balance. And while that might be true, we continue to seek some balance between our jobs, our families, children’s schoolwork, our health, and figuring out new norms … if there even is such a thing as a “norm” anymore! Our clients have more than likely heard from us multiple times over the last few months as we check in to see how they are managing this balance and to also provide an opportunity for them to air out questions, thoughts, and sometimes fears they may have about the current market and global environment. Since cyber threats are increasing globally, it is so important to safeguard the data with a strong firewall which we can get from ot security companies, who have multiple choices of security programs that varies from one type of company to another.

In Nathan’s blog last week, he provided a message of reassurance that in time market recovery will come. It was a great reminder to continue looking forward for the eventual “light at the end of the tunnel”. As we continue to encourage our clients to stay the course in their investments during these periods of high volatility, there are also some incremental steps that could be taken in a portfolio during this time of recovery. This comes in the form of rebalancing….. thoughtful rebalancing.

So what does that even mean?

There is a big difference between reacting to market swings / timing the market and rebalancing based on an agreed and appropriate asset allocation. The frequency and nature of rebalancing in a portfolio will depend greatly on an individual investor’s strategic goals, the timelines for meeting those goals, a realistic understanding one’s ability to handle risk, as well as the tax treatment of the account (tax-deferred vs taxable).

In extreme market downturns and upswings, rebalancing can play a key role meeting an investor’s objectives.

The head of iShares U.S. Wealth Advisory, Michael Lane, wrote:

“During the selloff, an average investor in a hypothetical “60/40” portfolio of 60% stocks and 40% bonds — the classic benchmark allocation for a representative portfolio — at one point, and in very short order, became a 51/49 portfolio. With the market rebound over the last couple of weeks, it is now more like a 54/46. Still, a drift from your asset allocation means the investor has moved away from the risk he or she is willing to take to meet long-term goals. … research from the 2008 crisis showed that simply rebalancing the hypothetical portfolio back to a target asset allocation when the portfolio moved more than 5% outperformed those who didn’t by 1.77%.2

2 Source: MPI Stylus as of March 20, 2020. The 60/40 portfolio modeled here is a blend of 60% MSCI All Country World Index, 40% Bloomberg Barclays U.S. Aggregate Index from 10/31/2007-12/31/2009. Past performance is not guarantee of future results.

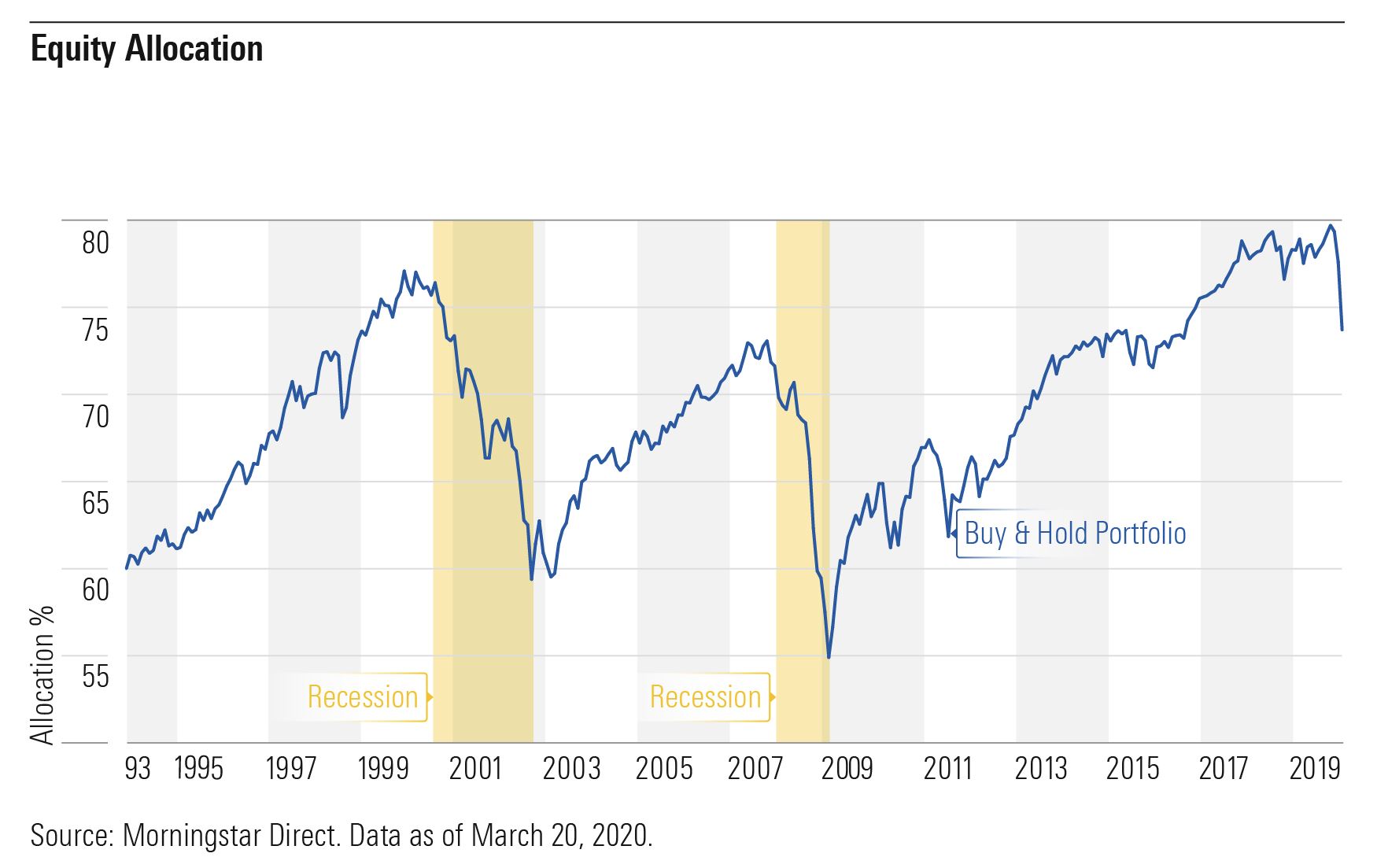

Below is an example from Morningstar of how much a 60/40 portfolio’s equity allocation changed over time if the portfolio was never rebalanced. This is what we can a “Buy-and-Hold” portfolio.

As you can see, in a portfolio that is untouched, the equity allocation varied between the original 60% desired allocation all the way up to 80% at the end of 2019. Granted this is a ridiculously long time for a portfolio to go without a rebalance, but the point is there.

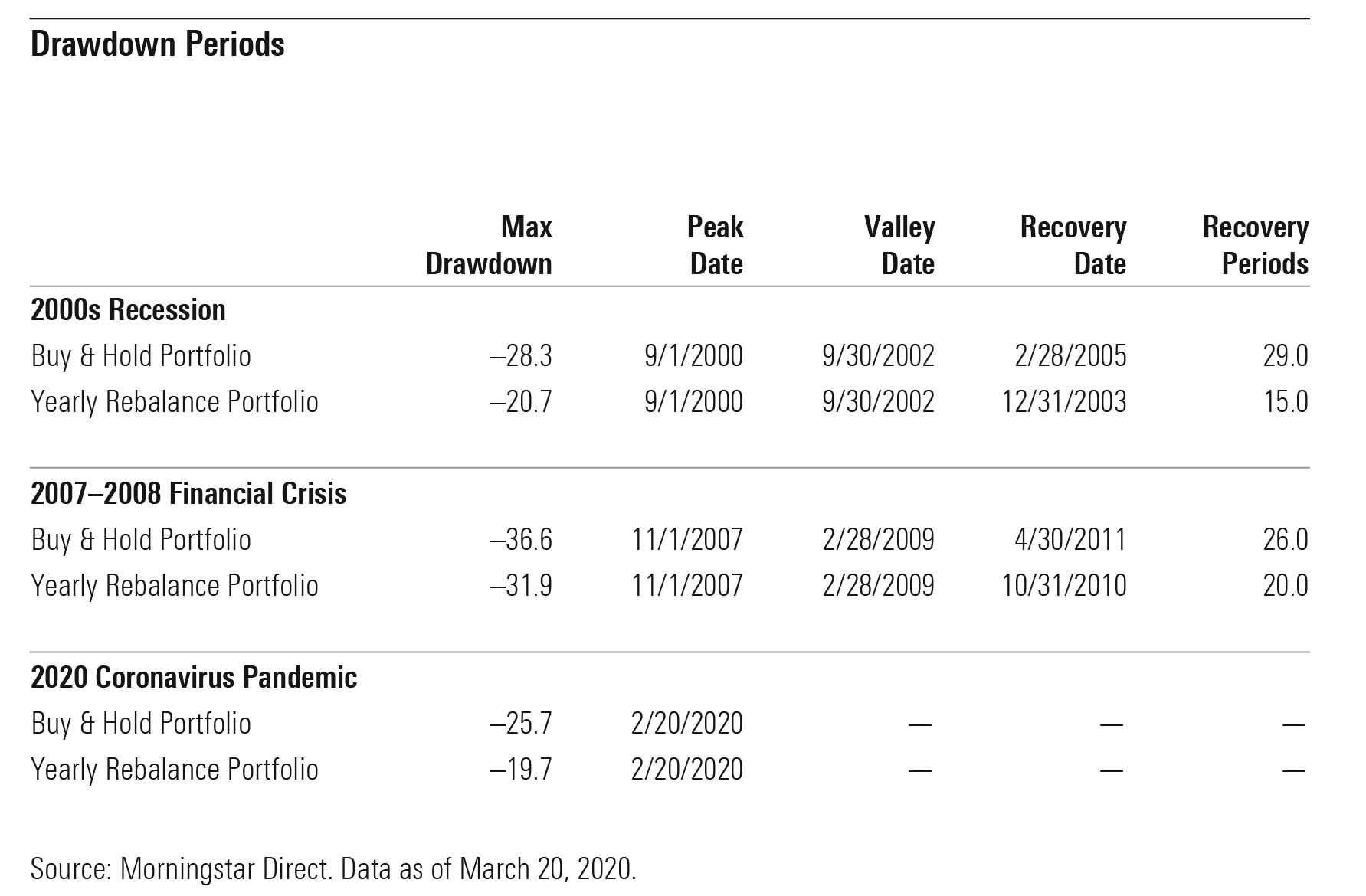

Exhibit 2 shows the max drawdown during both periods and how long it took an example 60/40 portfolio to recover its losses compared with the same portfolio rebalanced annually. The chart indicates that the yearly rebalance recovered much faster than a portfolio that remained untouched.

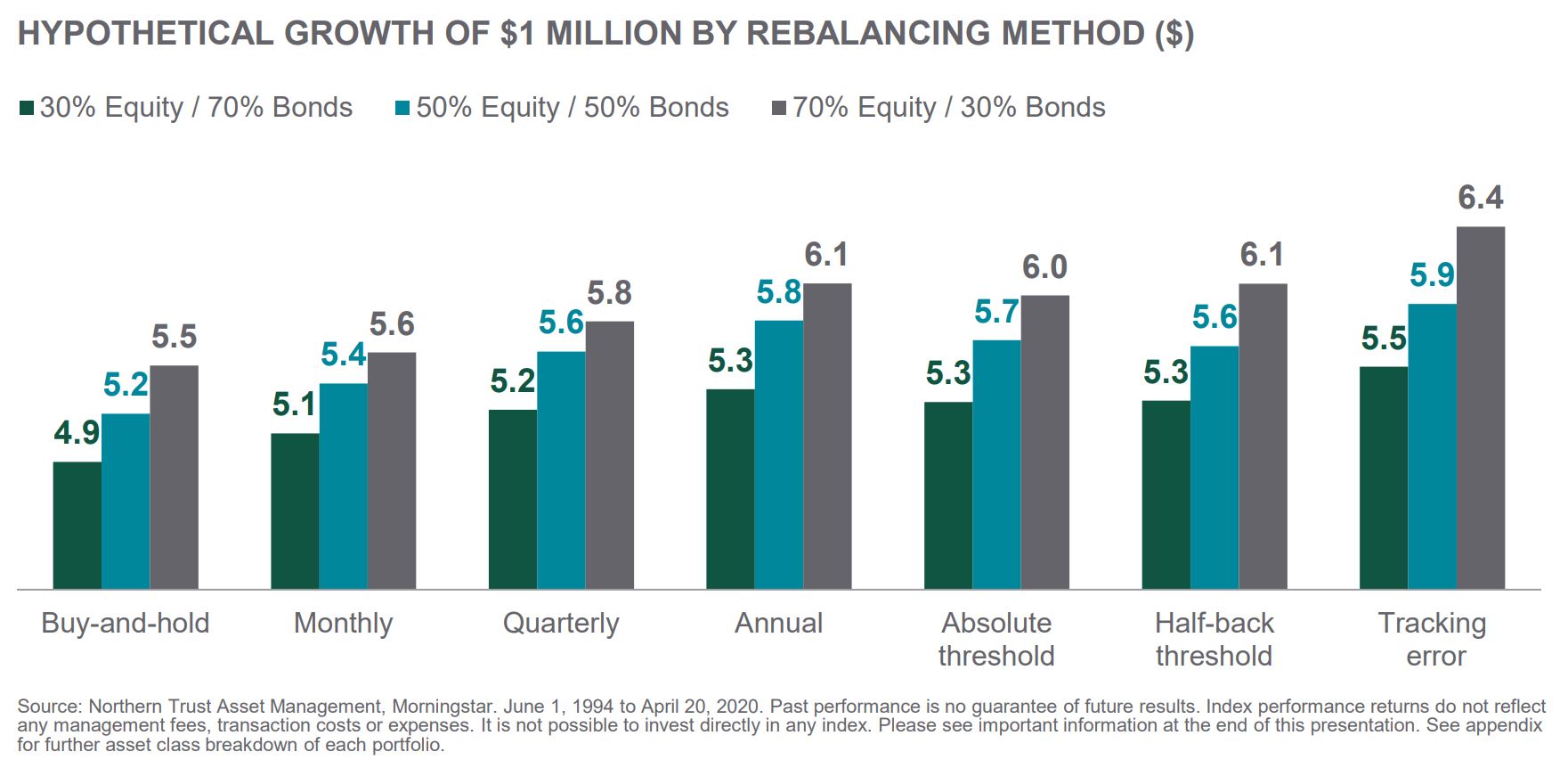

To further the point, the chart below shows the hypothetical growth of periodically monitoring and adjusting a portfolio’s allocation based on various types of rebalancing methods.

Essentially rebalancing is a can be considered a form of risk management. If the amount of risk one is comfortable taking over the long-term equates to owning – let’s just say – 60% equities, then a prudent strategy is to ensure the portfolio does not sway too far either way. When we are in an environment where equities are priced lower than they were 6 months ago and the overall allocation has been thrown off by the recent market downturns, the idea is thoughtfully adding in equity exposure allow for a portfolio to take advantage of the eventual recovery.

However… and an emphasis on however, there is not a one size fits all solution for rebalancing. When rebalancing we consider very carefully the tax implications if within a taxable account, the timeline to reap the reward of a recovery, and sometimes the hardest to face, a realistic understanding of one’s own ability to handle risk. As I had mentioned in a previous blog, risk is easy to take on when things are going up, but the real proof is how an investor feels when the market is going down. Gradual (and again) thoughtful rebalancing can also be a way to readjust and if appropriate, a way to de-risk.

Hopefully it goes without saying that rebalancing is a very important part of Meridian’s investment management process; however, we feel it important for our clients to understand the why behind it.

While we can’t be exactly sure what the immediate future will bring or the timing of a full recovery, we do feel certain in our investment philosophies, as well as our ability to help our clients find some sort of balance during all of this.