Stocking Up on Employer Stock

The groundhog really was not joking with his appearance implying 6 more weeks of winter. While the snow can be beautiful, snow days lose a little bit of their magic when you actually have to go somewhere and shovel it. My one year old has the right idea about snow days, particularly after he face planted the second we went out in the snow the other day. All was not calm when all was white….

But just as 2020 is now a thing of the past, so will be the winter weather (hopefully sooner than later)! And with spring in the near horizon, that means tax season is about to be in full swing. While you can’t actually file your taxes until this Friday, many individuals are already preparing themselves for how much they may owe or will be refunded.

Tax Advantages for Employer-Offered Benefits

Even though tax savings strategies particularly from an employer benefits standpoint have ended for 2020, understanding the tax advantages and implications of employer-offered benefits is an important exercise and one we revisit often while reviewing and updating financial planning for our clients.

Benefits provided in the form of stock whether it is provided as an incentive, an award for performance, or an opportunity to further invest in the company you are employed with is an excellent benefit to grow / accumulate wealth within a company you (hopefully) believe in to be profitable. However, clarity around the taxation of these benefits is a frequent concern and question we receive from clients.

The most two common forms of employer stock compensation we tend to see are

- Employer Stock Purchase Plan (ESPP)

- Restricted Stock Units (RSU)

Employer Stock Purchase Plan (ESPP)

ESPPs are a way to purchase company stock at a discount of usually 5%-15% with after tax payroll deductions. Employees who wish to participate in this plan defer a portion of their pay or a dollar amount during an outlined offering period of usually 12 – 18 months with several purchase periods usually consisting of 6 months each within that timeframe. During this period, your contributions to the ESPP accrue until shares are purchased on your behalf on the last day of a purchase period. The price of stock purchased is the lower of the price it is trading at either on the first day of the offering period or the last day of the purchase period plus the discount. So essentially as an employee you get to buy company stock by choosing the lower price out of two days, plus with the set discount, which means you receive an immediate unrealized capital gain – a pretty sweet benefit!

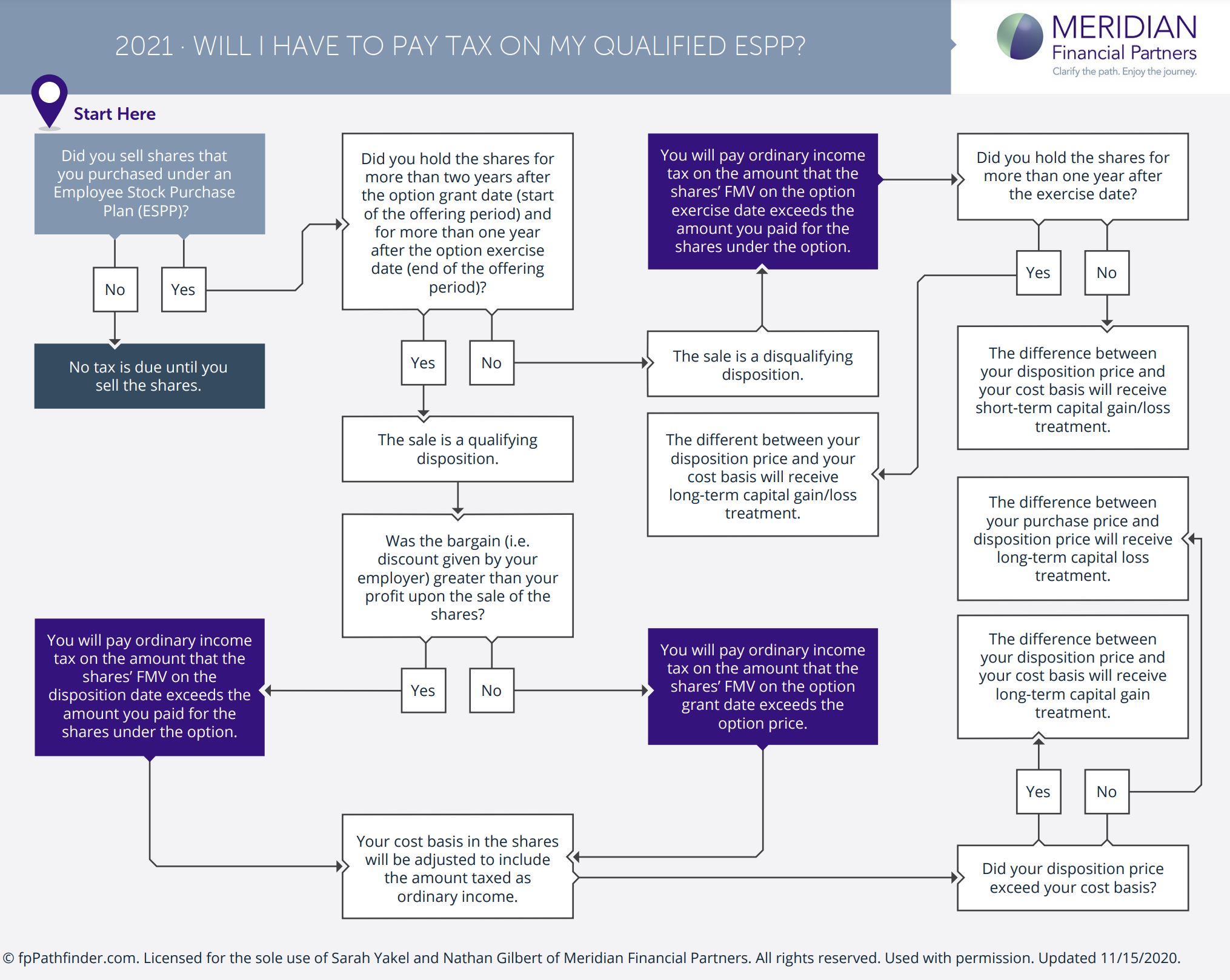

Understanding how these benefits are taxes can feel daunting, particularly if you are looking to sell shares in the near future. If you are looking for the cliff notes version, this chart below is great to help determine how you will be taxed on the sale of your stock in your Employer Stock Purchase Plan.

If you sell your stock and have held your shares of company stock for more than 1 year after the purchase date and more than 2 years after the beginning of the offering period, this is considered a qualifying disposition. Ordinary income tax is owed on the lesser of:

- The discount offered based on the offering date price OR

- The gain between the actual purchase price and the final sale price

Long term capital gains, which tend to be more favorable, are owed on the difference between the sale price of the stock minus purchase price (not including the discount).

If you sell your stock and have not held it for either more than 1 year after the purchase or 2 years after the beginning of the offering period, this is considered a disqualifying position. Ordinary income is owed on the difference between the actual purchase price (what the price the stock was selling for on the day you purchased it, not the lower of the two prices as mentioned earlier) and the discounted purchase price. Capital gains (short or long depending on if you held it for more than a year after purchasing) are paid on the difference between the sale price and the actual purchase price.

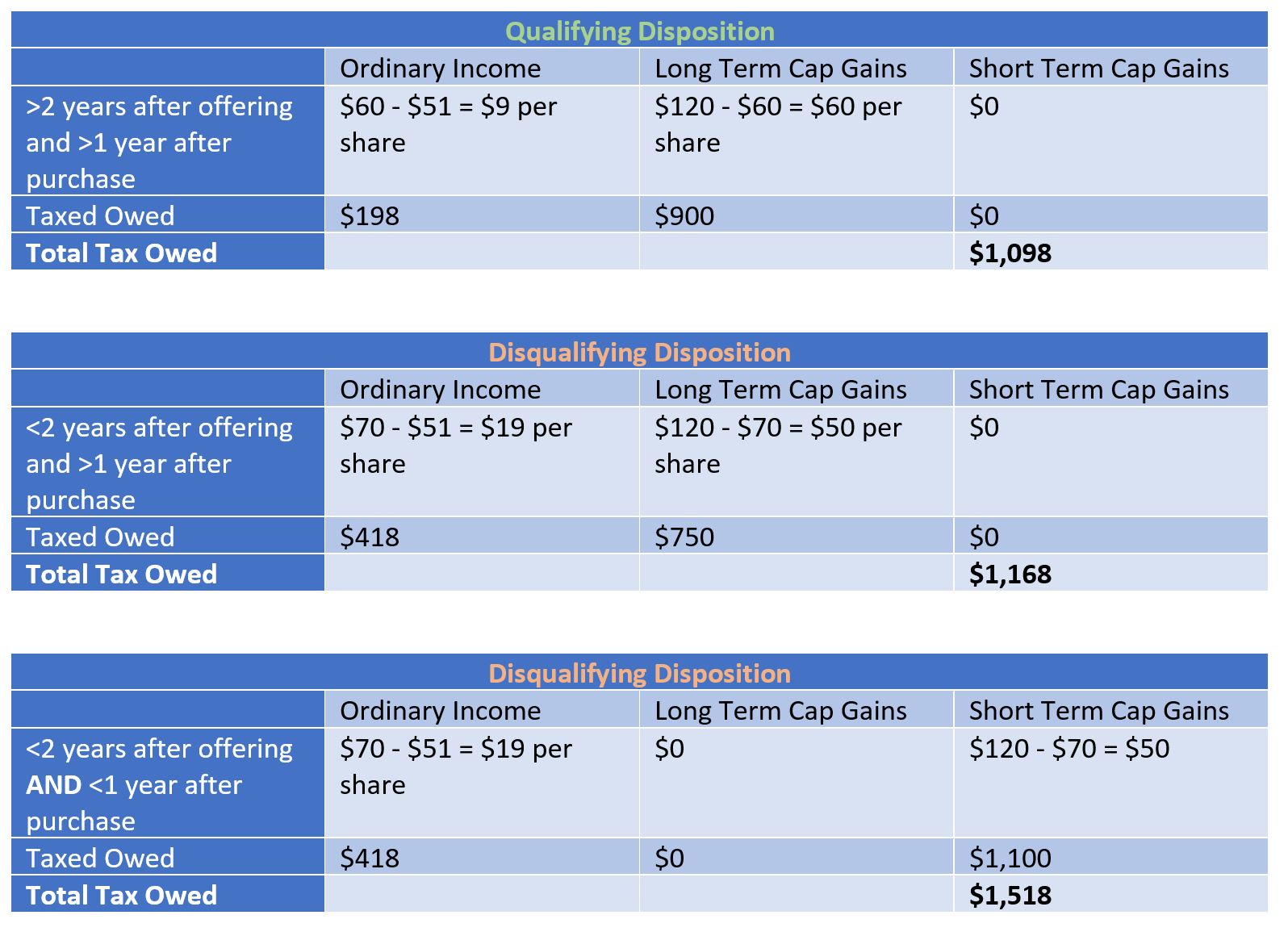

Here is an example:

- You participate in an ESPP, the stock price at the beginning of the offering date was $60.00.

- The stock price at the end of the purchase date was $70.00

- Discount provided is 15%: $9.00 — This is 15% of $60.00 since that is the lesser of the two above prices.

- Shares purchased 100.

- If you sell all 100 shares at $120 and you are in the 22% marginal income tax bracket and 15% long term capital gains tax bracket.

When figuring out how much you owe if you sell stock from an Employer Stock Purchase Plan it is important to know these dates / numbers.

- The market price of the stock on the offering date

- The market price of the stock on the purchase date

- Discount offered

- Number of shares purchased

Restricted Stock Units (RSU)

RSUs are a little more straight forward from a taxation perspective. RSUs stand for restricted stock units and are considered a form of compensation. They are issued through a vesting and distribution schedule upon an employee remaining with the employer for a certain period of time or achieving performance milestones. Unlike ESPP plans where you could have the option to turn around and sell the stock once you purchase it, you cannot sell RSUs until they vest and therefore there is no real tangible value until the shares vest.

From a tax perspective, restricted stock units are taxed once they vest as opposed to ESPP that are taxed once shares are sold. When restricted stock units vest, the entire amount of the vested stock must be counted as ordinary income the year it vests. While that sounds like a painful tax hit, most companies provide a sell to cover option in which shares of the vested stock are sold to cover the income taxes owed. If shares are sold at a later time after vesting, the difference between the sales price and fair market value on the date of vesting is capital gain (or loss).

While stock bonus and purchase plans are excellent ways for employees to invest in their employer and in some cases at a discount, it still is important to ensure that while you have some “skin in the game” that you aren’t putting too many eggs in one basket. It is very common for employees who feel closely attached to a company they work for to fall victim to confirmation bias or familiarity bias. Focusing portfolios on a company we feel too familiar with or focusing only on information about a company that confirms our beliefs rather than contradicts them can stand in the way of proper diversification of a portfolio.

If managed properly and keeping some awareness, owning stock through your employer is still an excellent way to build your investments and even build a source to fund future financial needs or other investment vehicles. But being prepared for the tax implications is also a crucial part. No one likes surprises on April 15th.