The Splits

In all the market drama of January, Google’s announcement of a stock split went unnoticed by many investors who were distracted by all the other crazy market moves.

On February 1, Google parent company Alphabet said it would split its stock 20–1. That means that for every 1 share of Google an investor owns, after the July split, they will now own 20 shares. That doesn’t actually mean their shares will be 20 times more valuable, as the price adjusts accordingly. This chart from Visual Capitalist shows the math of a split:

Using the same logic, if Google split today, the share price would fall from $2,784 to $139.

Investors love stock splits because of the inherent cognitive bias of anchoring. Once, an investor has seen that Google is worth $2,784 per share, buying a share at $139 seems to be an incredible bargain. However, in reality, no value has been created and the only thing that has changed is the number of shares outstanding.

According to James DePorre, Founder of Shark Investing, “From a pure accounting standpoint, stock splits have no impact on the valuation of a stock. It is simply the equivalent of cutting a pizza into more slices…Stock splits can have a dramatic psychological impact. The theory is that an expensive stock can now be more easily bought by a greater number of people when it is trading at 5% of its prior price. It also can create the illusion that the stock is now ‘cheaper’ simply because the price tag is lower, although valuation remains the same.”

(same logic…)

Despite the academic reason why stock splits should not have a material impact on a company’s stock performance, there are a few reasons why they actually do:

- Retail investors prefer to buy lower priced stocks. In an academic study, investors preferred to own more shares of a lower priced company than 1 share of a higher priced one. It feels more meaningful—and a better chance at gains– to own 20 shares of Google at $139 than 1 share at $2,784. According to Rueters, there’s recent evidence that this is true:

- When Apple split its stock 4–1 in July 2020, retail investors upped their purchases from $150 million per week to nearly $1 billion, according to Vanda Research.

- When Tesla split its stock 5–1 in August 2020, retail investing jumped from $30–$40 million/week to $700 million.

- Stock splits are sometimes used by company management to convey optimism about company growth. In one academic paper, companies who announced stock splits, combined with strong corporate earnings, excelled post-split.

- Index inclusion…and this may be one of the bigger reasons that Google is splitting…many stock indexes have metrics for inclusion. The Dow Jones Industrial Average is weighted by share prices, so a high priced stock would overwhelm the index. So, the Dow tends to include stocks with more moderate prices. If Google’s new price in the $100 range makes them more attractive for inclusion in the Dow, that would be a huge benefit to Google shareowners. Any mutual fund or exchange traded fund that maps to the Dow would have to go and buy significant amounts of Google shares, increasing demand and potentially driving the price higher.

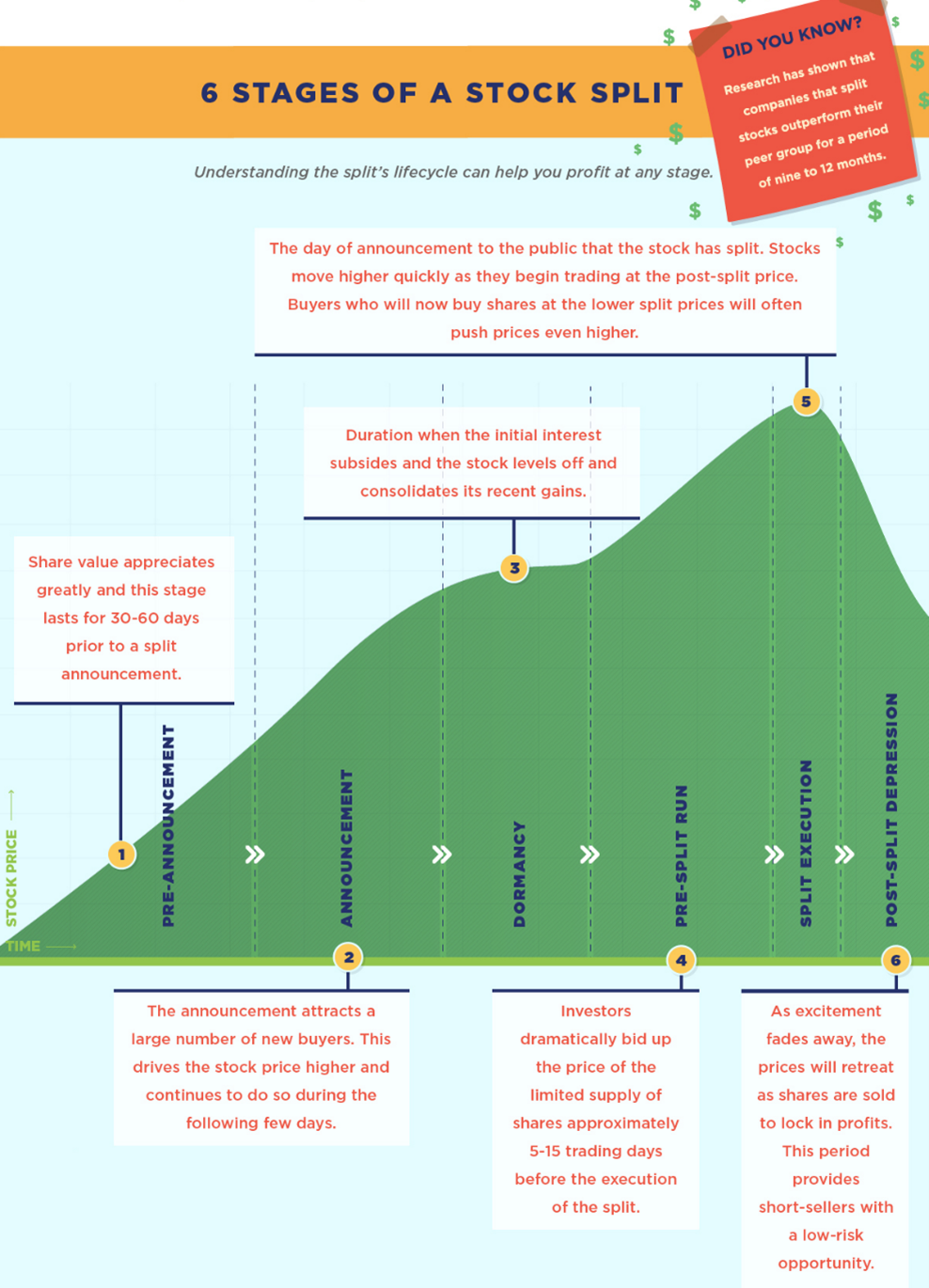

So, while stock splits should not be a driver of future performance, in real life, they do tend to cause short term price movements. This chart from Visual Capitalist illustrates the life cycle of a typical split:

At Meridian, we do not trade into these short term price cycles, but we are interested in the management reasons for a split… Google’s split is certainly an interesting one!