Are the best investors dead?

A 2014 Fidelity study of the best performing 401K accounts came to an interesting conclusion…the best performing accounts over the time period of 2003 to 2013 were those held by an estate or by participants who had totally forgotten about their account. In both cases, the accounts were marked as inactive due to lack of trading activity.

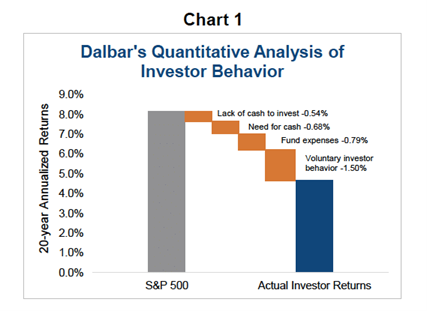

This Fidelity study (which is hard to actually find and has become a bit of urban legend) bears out the painful truth that an average investor trades too often and at the wrong times…and corroborates the annual study done by DALBAR. DALBAR uses mutual fund purchase and redemption information to extrapolate what the average investor experience has been. They calculate that investors have cost themselves around 3-4% annually due to selecting expensive funds, forced liquidation, and “unforced errors” (buying and selling at the wrong times):

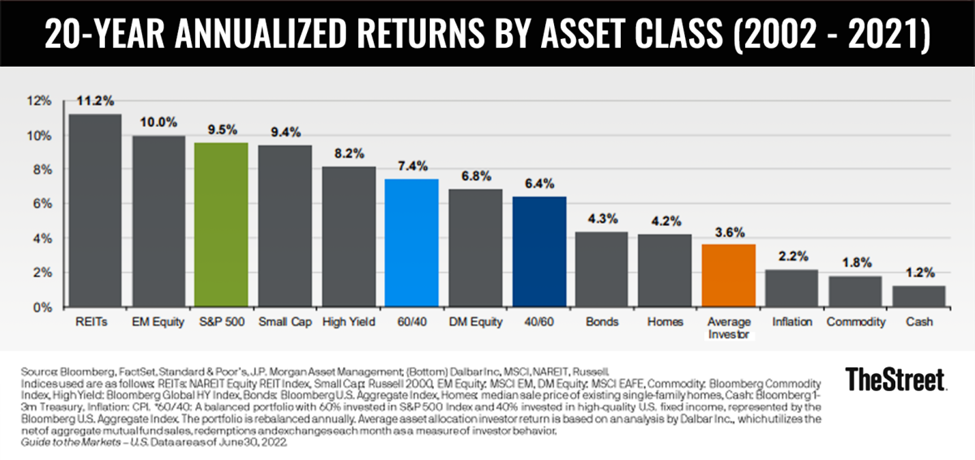

Over long periods of time, those trading errors add up, with the average investor averaging an annual return of 3.6%, versus the S&P average annual return of 9.5% and the average balanced portfolio return of 7.4% (in light blue):

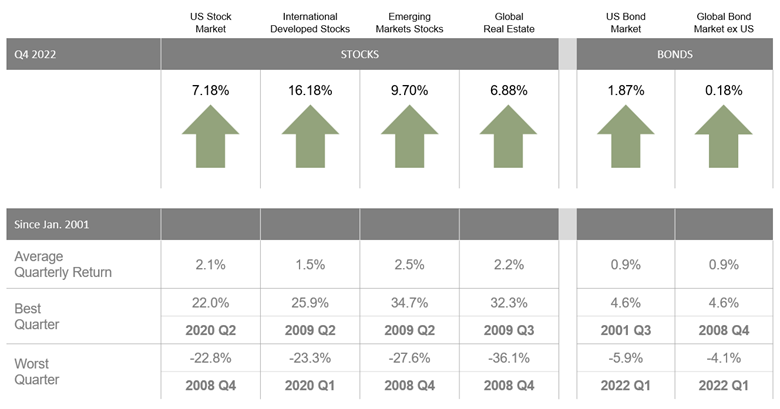

Even over short time frames, trading errors stack up. At the end of the 3rd quarter of 2022, it was bleak for investors. September 2022 was brutal, with S&P 500 down 9.34% for the month…and down over 24% for the year. Many investors gave up…and then missed the 4th quarter rally:

So, how to “play dead” as an investor?

- Carve off any cash that will be needed for emergencies, upcoming projects, or living expenses for the next 3 years and keep that money safely invested in cash equivalents (like money market funds or CDs) or fixed income investments (like government or corporate bonds)

- Decide on an appropriate mix of investments for your unique situation…do you need more income or more growth?

- Buy companies and funds that you plan to hold for a long time. Buy stocks of companies you plan to hold to your grave. Buy funds that have fees that are justified (either low cost, well diversified funds or if the fund cost is higher, make sure the fund has delivered excess returns over the benchmark historically).

- Rebalance back to your target allocation no more than quarterly—and on a schedule. Not when you feel like it.

- Revisit your target mix of investments annually to amend for any changes in your personal situation.

Most of all, avoid excess trading—the costs and the time out of the market is what sinks most investors…so set up your portfolio well, and then be like Milo and Bailey and “play dead”: