A Funny Thing Happened on the Way to Meridian

A few weeks ago, my low tire pressure light came on as I was driving the kids to school. I stopped quickly, topped off all the tires, and kept on heading to school. After I dropped the kids off, the light came on again, and I knew I had a leak. What I didn’t realize was the severity of it!

As I pulled into Warrenton Village to grab coffee and call a mechanic to schedule an appointment to get the leak plugged, I heard the rim of my tire crunching on the pavement, and parked in front of Starbucks to find this:

Groaning, I started the process of getting out the spare tire and tools. After wrestling ineffectively for a little while, a very kind lady stopped and said, “You know, National Tire and Battery is right behind you.”

Thankfully, I was able to just walk over, explain the situation to the folks at NTB, and they came to the parking lot and fixed me right up!!

A few days later, relaying the story to my dad, he was stunned to learn that I wasn’t a card carrying member of AAA. For such a small price per year, her argued, I could have total protection and peace of mind that I would never be stranded on a flat tire again.

I argued that since I’ve had a flat tire that has stranded me once in the past 15 years, the $142/year cost for the Plus membership would have been exorbitant…that would have been $2,130 in membership fees to cover one tow truck visit.

My dad argued that I was lucky to have been stranded in the parking lot of a tire store, and I could have been on a dark, desert highway. He said that the peace of mind was well worth the premium price of the membership.

We agreed to disagree (I think), but the argument is a perfect example of risk management decision making.

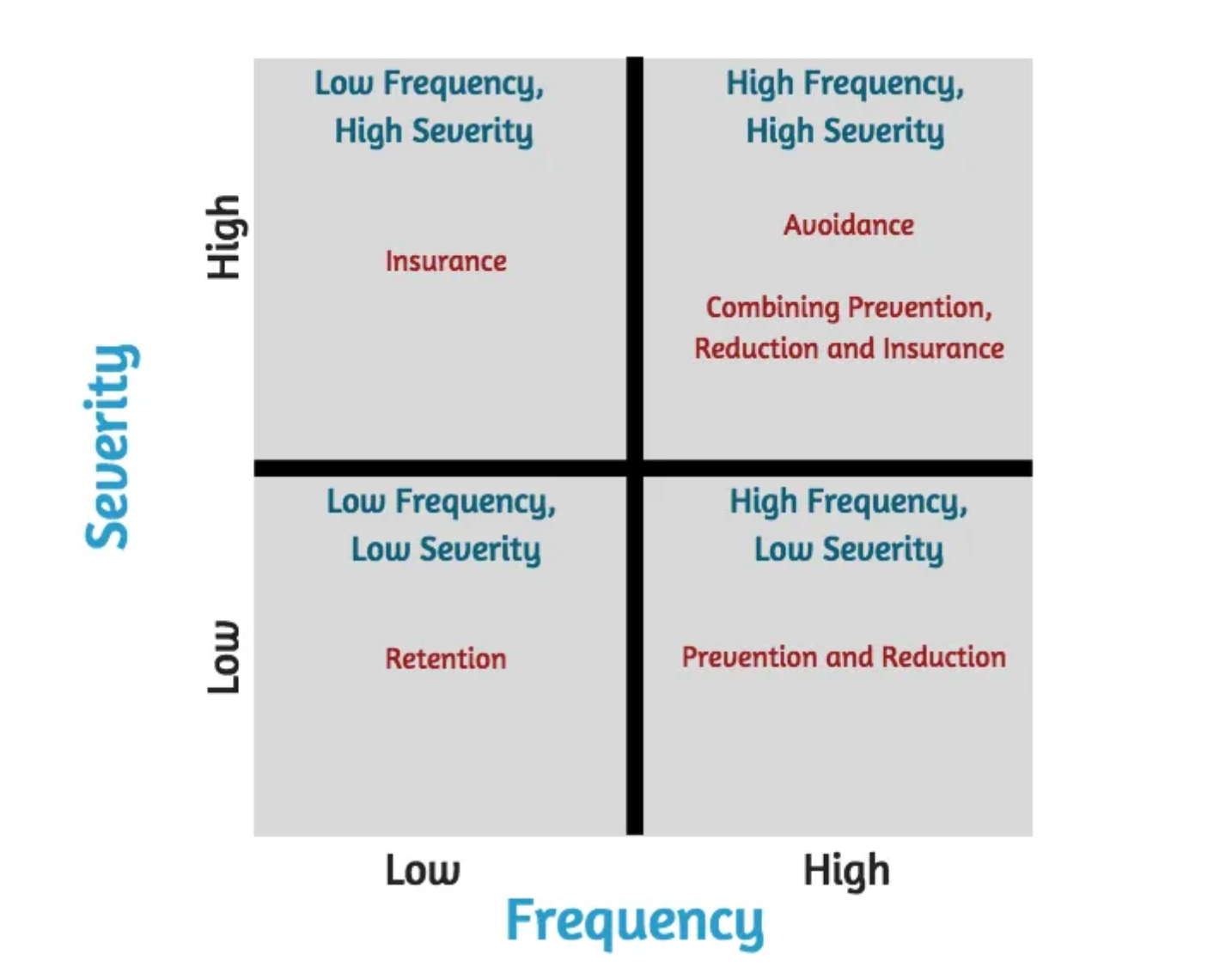

Risk Management Decision Making

When deciding how to manage risk, severity of the loss should be considered along with how frequently the loss most likely will occur. So, the traditional risk management decision framework looks like this:

When a loss occurs frequently but isn’t a huge loss, you generally just take proactive steps to prevent and reduce the risk. In the summer in Virginia, there is a pretty high probability that a thunderstorm will occur in the afternoon, but we just accept that risk and carry umbrellas or adjust outdoor plans as needed. No big deal.

When the chance of loss happening is low, and the impact would be minimal, those risks can basically be ignored.

It’s when the consequences are big, and the severity of the loss would be high where it gets hard. High frequency, high cost events are difficult to manage—like building a house in a flood plain. Chances are high that a flood will occur and cause damage. Insurance will be prohibitively expensive, so one of the main options is to avoid the risk entirely (i.e. don’t build the house there!!).

The category of low frequency events that cause large damages is where insurance is most often used. Because the loss causing event is relatively infrequent, the cost to transfer the risk to an insurance company is modest—but protection will be available when needed most. It’s not often we are in car accidents, but when we are involved in one with huge damages to property, insurance coverage is valuable.

The conversation with my dad demonstrates that risk management is slightly different from person to person. I view a flat tire as a low frequency, low severity event—so, I elect to just retain the risk. My dad views a flat tire as a low frequency, high severity event, so he pays for insurance coverage to mitigate the potential loss.

Annual Risk Management Review

And this is why an annual risk management review is important! We can view risk differently, and severity is measured differently by everyone. My husband reminded me that as a college student with very little money, a flat tire was the end of the world…and so a very high severity risk. (And frankly, with the way he and his friends drove, it seemed to be a high frequency event too). So, he reminded me that he fully used his AAA membership!

At Meridian, we are happy to help you review your risk management strategies—while we don’t sell insurance policies, we work with several great agents that we trust to help you find the right blend of risk management tools for your unique situation and are happy to introduce you!

And, after a dead battery today, I think we will be reevaluating that AAA membership for the Yakel family… 😊