Name Your Beneficiaries

I know I have touched on this topic before, but we have come across a couple of cases recently where clients have failed to name beneficiaries on their IRAs, or they have named their estate as the beneficiary. Both situations can create problems, and in some cases, less options for beneficiaries. All types of retirement accounts (IRAs, 401ks, 403bs, etc.) are required to have at least one beneficiary named.

If you are married, the situation is pretty straightforward (assuming you want your spouse to inherit your IRA! 😊). While you should still name the spousal beneficiary directly, he or she can essentially treat the IRA as his/her own and use the money for retirement expenses.

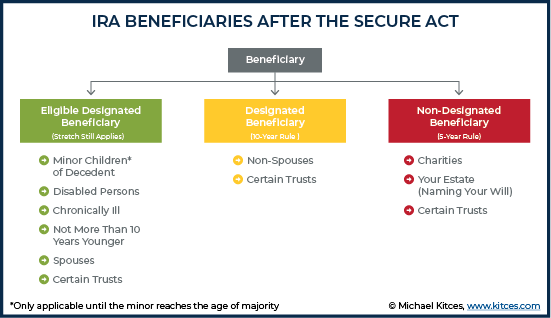

For non-spouse beneficiaries (in most cases, children), the situation has become more straightforward with the passing of the SECURE Act. All non-spouse beneficiaries must withdraw all of the money within 10 years following the date of death of the original account owner. This change is less advantageous (from a tax perspective) than the previous life expectancy method, but it does allow some flexibility around the timing of withdrawals.

Here is a simple chart from Michael Kitces outlining the beneficiary options depending on type:

It is also important to note that, with a few exceptions, retirement accounts are the only types of accounts that have beneficiaries. All other assets are covered by a will, so it is critical to have a will and update it as necessary.

Part of the reason I thought of this blog topic was my own children. I don’t know why I thought of it while camping with them, but I realized that I had yet to update my own will since having kids. Even in my business, I cringe at the thought of thinking about a will and getting it updated! It can be a pain, but it can save you children and other beneficiaries a lot of trouble!

Eagerly awaiting their Beneficiary IRAs