Ch-Ch-Ch-Ch Changes (to tax rates)

Facing Financial Changes

The first refrain of the song “Changes” by David Bowie contains some surprisingly apt lyrics for probable changes in tax rates:

“Ch-ch-ch-ch-changes. Turn and face the strange. Ch-ch-changes. Don’t want to be a richer man.”

Yes, there are some changes (and maybe even strange ones) coming to the tax rates. While it’s almost impossible to do so, I am going to attempt to discuss these potential (still not set in stone) changes without getting political. Folks have argued for many decades (okay, centuries) over taxes and how or whether they should be applied. The headline reasons for the increases are to pay for trillions of dollars in stimulus payments, a sweeping infrastructure bill, and increase tax on the “wealthy” (there are wide ranges for what Americans consider wealthy).

What can you do it about it? I hate to say it, but there’s really not much you can do in advance other than keep a close eye on things and adjust your estate and retirement planning accordingly. Some highlights or lowlights depending on your opinion/situation:

- The top tax bracket for the highest earners will go back to 39.6% from 37%. Social security tax would be applied at higher income levels

- The corporate tax rate would go from 21% to 28%

- Those earning over $400,000 would pay more in payroll taxes

- The Child and Dependent Tax Credit would go from $3,000 to $8,000

- Tax relief offered for student debt forgiveness and restoration of first-time homebuyers’ credit

- The estate tax exemption will be reduced considerably. Step-up on cost basis on death would be removed

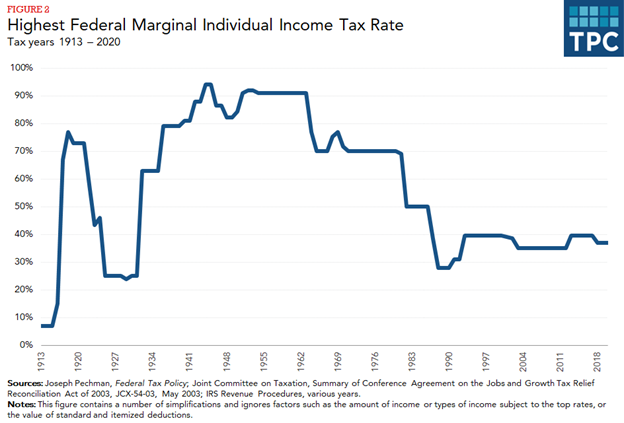

There are many other implications and nuance related to the overall plan. And, the thin margins for Democrats in the House and Senate might make it difficult for some of Biden’s proposals to pass. For some context, here is a chart of the top income tax rate over time.

Ch-Ch-Ch-Changing Tax Rates

There is certainly a lot to unpack here, and far too much to try to address in one blog post. As mentioned, there isn’t a whole lot you can do to avoid the tax increases, but you could consider:

- Increasing your contributions to tax-deductible retirement accounts. If you aren’t already contributing the maximum, this should help reduce your income

- Give away some money and/or stocks. You can currently give $15,000 per year to anybody without affecting your lifetime gift and estate tax exemption

- If you give away some highly appreciated stock, this may help avoid some capital gains payments (the recipient would still incur capital gains if the stock is sold)

- Make gifts to an irrevocable trust. This option requires some advanced planning and consultation with a qualified estate planning attorney. In short, it gets money out of your taxable estate while still providing some potential income for the remainder of your lifetime

Here’s hoping that the coming changes include further reductions in COVID cases and restrictions. It would be ideal if my son no longer had to change in and out of his hockey gear in the parking lot!

Happy Spring!

Nathan