The Unexpected

March Madness is here, it is the season of surprises (we’re looking at you, Oral Roberts University…thanks for busting everyone’s brackets…). The members of Yakel family spent the weekend alternately crowing in victory or complaining in defeat, as our family bracket competition got heated…

While March Madness surprises are fun and entertaining, life in general is full of surprises, and not all are good. So, while financial planning attempts to project and estimate how things will go in the future, and equally important part of a financial plan is thinking through—and preparing for the unexpected turns that life can take.

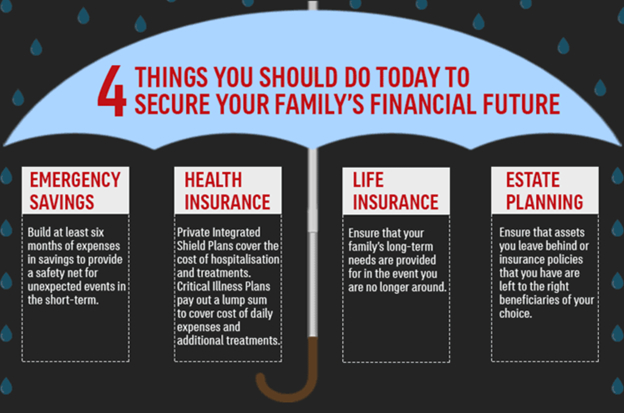

Generally, when thinking about preparing for life’s surprises, we tend to think of them in two main buckets: things we can afford and things we cannot afford.

For the first category—surprises that we can afford, like new tires on a car, home repair, loss of a job—we build an emergency savings fund that will help to cushion the cost.

It’s the second category—things we can’t afford—that is harder to plan for…

These are things like a sudden debilitating illness, a major property loss like a car accident, or an unexpected death. Insurance and estate planning are the main tools used to try to deal financially with these shocks.

We’ve written a fair bit about estate planning so we wanted to touch briefly on the life insurance part of a family’s safety net.

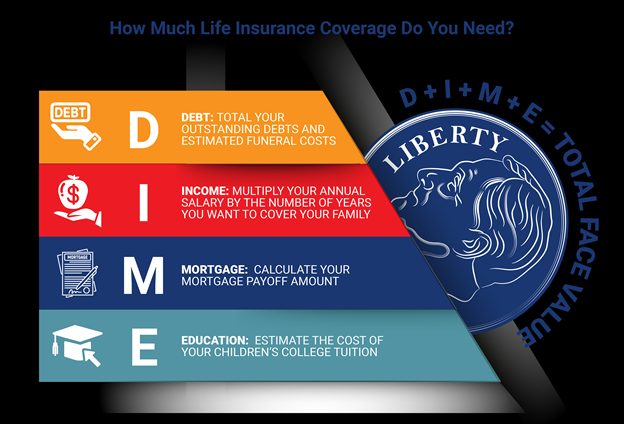

Recently, we’ve answered a lot of questions about how much life insurance is appropriate, and it is a complicated answer. From a basic perspective, the proceeds from life insurance should cover these things:

- Your debts—including your mortgage balance

- The value of your income stream to your survivors who may be counting on it

A simple calculation of desired coverage would be to use the DIME method:

But, from here, that base amount of coverage may need to be adjusted…for example:

You may need more insurance if:

- Your financial situation is changing (i.e. you are thinking about buying a second home or new car)

- You may have to take care of additional family members in the future (like your parents)

- You want to leave a legacy for your family

You may need less insurance if:

- You have vested pension income available to your family in the event you were to die prematurely

- You do not want to pay for college costs, or have other savings set aside

- You do not have family depending on your income (your kids are grown, or your spouse has their own income stream)

Every situation is unique, and coverage should be carefully considered—at Meridian, we are happy to help you think through your safety net in the context of your whole financial plan.

Life is full of surprises, and we’d love to help you be ready.