What Happens When My Work Retirement Plan Dissolves?

We recently helped a business owner who is nearing retirement unwind his company’s work plan. This can happen for several reasons, but it is usually because the business is closing or the plan itself is ending. Either way, it’s important for the participants to know their options and avoid some common pitfalls.

When a retirement plan closes, it means that each qualified participant will receive a payout from the plan on a pre-determined date. Prior to that date, each recipient will choose how he or she wants to receive the money. Here are the options:

- Send it to my IRA – this is likely the best option. It avoids taxes and allows for flexibility with investments moving forward.

- Send it to my new company’s plan – if your company is closing entirely and you are moving to a new job, you can usually have money from the old plan moved into the new plan

- Just send me a check – CAUTION on this one. Your distribution will be taxed as though you received a paycheck for the full amount, AND you could face a 10% penalty if you are under age 59.5

I would say the most common pitfall is treating money coming out of the plan as “found money” and spending it.

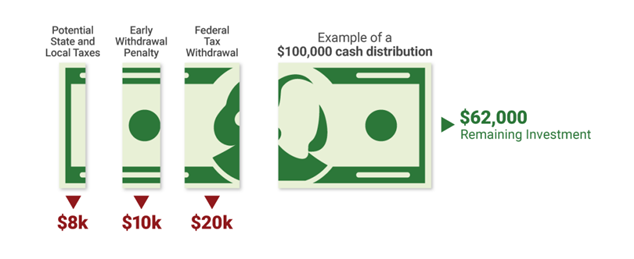

In the above example, if you withdraw $100,000 and are under age 59.5 (assuming no other exceptions), you are giving away about $28,000 in taxes and then another $10,000 in early withdrawal penalties, leaving you with a net amount of just $62,000. To further compound this issue, some IRA holders do not elect do have approximate taxes and penalties withheld (or set aside) in advance, so there can also be an unwanted surprise amount owed come tax time.

Also note that some plans automatically send out checks to smaller dollar account holders. In this situation, the recipient still has the option to roll the money into his or her IRA and recoup any automatically withheld tax money once taxes are filed.

The bottom line is that you should try to move the money directly to an IRA (or new company plan) first. Even if you need some of the money down the road, you can control how much you take out in which tax year to minimize the tax impact. Don’t be like Rosie when faced with these types of decisions!

Lastly, there are exceptions to many situations, so your specific options may differ from the examples laid out above. Make sure you understand all your choices and the implications of each.

Happy fall y’all!

Nathan