WILMA!!

My two boys have been fascinated with TV shows, music, and movies from decades past—or as they like to call it: “stuff from the 1900s.” ☹

To my heart’s delight, we’ve been binge watching the A-Team at night–with occasional diversions to Knight Rider and MacGyver. My husband educates them on key musicians from the 70s, 80s, and 90s (only the alt/grunge bands from the 90s, of course…). And, my dad fills them in on things further back—Abbott and Costello, the Marx brothers, Pink Panther, and Looney Toons.

The boys and my dad haven’t made it around to the Flintstones, but I’m sure they will at some point…all I remember from my childhood is Fred yelling “WILMA!!!” at the end of the credits…

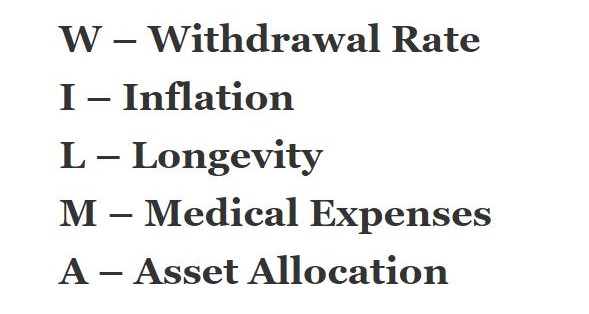

While “Wilma” reminds me of the Flintstones—it is also a mnemonic device to help advisors remember the main risks in retirement.

When clients think about risk in retirement, many are clearly focused on the risk of losing money in their investment portfolio. But, a great retirement plan also takes into consideration the WILMA risks:

Just a quick note on each…

Withdrawal Rate

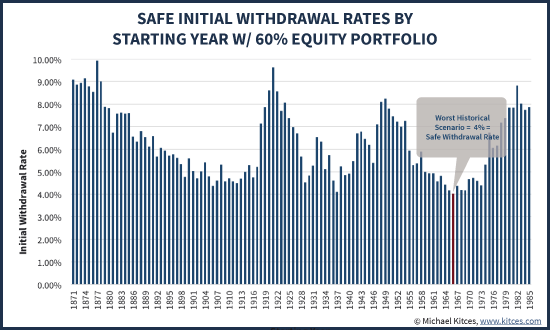

Most retirees have heard the 4% rule of thumb for retirement withdrawals…basically, a portfolio can support an initial annual withdrawal of 4% for 30-year period with a high likelihood of success. This rule began with initial retirement research which examined every rolling 30-year retirement period from 1871 to present, looking for the maximum withdrawal rate that could have been sustained over the period without running out of money. A well-known financial planner, Michael Kitces, published a summary of this research which showed that in the worst historical 30 year retirement period, a withdrawal rate of 4% was still successful, so that became the “safe withdrawal rate”:

So, while 4% is regarded as a “safe” rate, it is still a very wide and general target—many retirees would be ‘safer’ using a smaller initial withdrawal rate, while others could be more aggressive. Good retirement planning will adjust the initial generic 4% withdrawal rate based on factor unique to each client like current market conditions, portfolio allocation, other income sources, and future asset transfer plans.

Inflation

Inflation is the rising costs of goods and services over time, and with headline inflation running at 4% annually (compared to 2020), it has been getting a lot of attention these days.

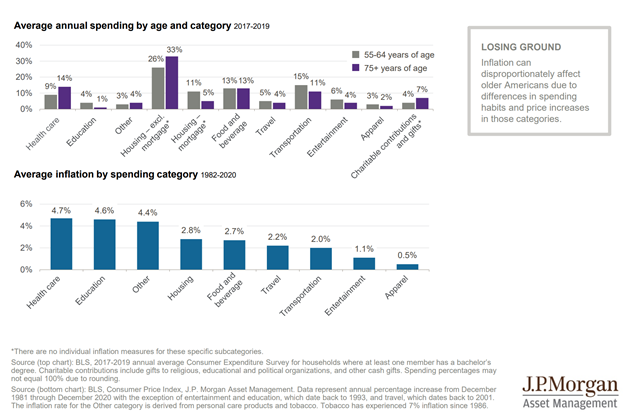

In retirement, inflation is particularly difficult as health care costs tend to rise faster than other goods and services, which affects retirees more than most:

Longevity

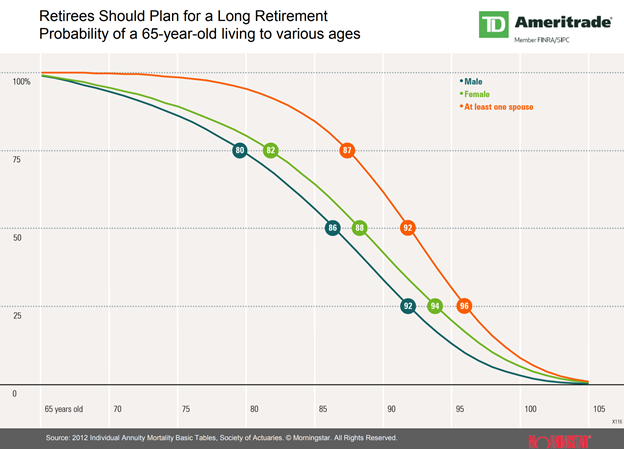

Longevity risk a challenge, as Americans are living longer—and married couples have a very high chance that at least one partner will live past age 95. Back “in the 1900s”, retirement would begin at age 65 and would end around age 85—now that 20 year retirement period is stretching to over 30 years! Building and investing a portfolio to sustain such a long period of withdrawals is a challenge.

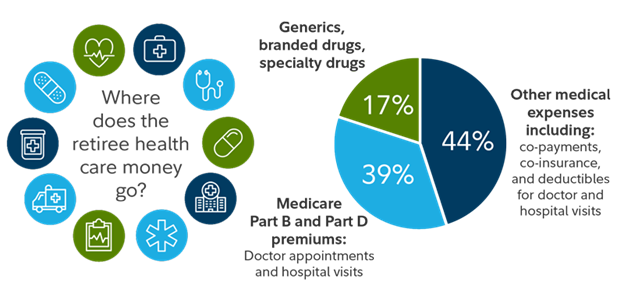

Medical Expenses

As the JP Morgan chart shows above, medical expenses comprise about 10% of retiree spending. Fidelity does a very thorough health care cost study every year, and the 2021 study determined that a couple retiring in 2021 will need $300,000 to cover medical costs in retirement. BusinessWire summarized the study:

“According to Fidelity, a 65-year old, opposite-gender couple retiring this year can expect to spend $300,0003 in health care and medical expenses throughout retirement. For single retirees, the 2021 estimate is $157,000 for women and $143,000 for men.

This year’s estimate marks a new milestone high, up 30% from 10 years ago when the amount was $230,000, but just 1.7% from 2020 ($295,000) as health care inflation has remained relatively flat over the last few years. Fidelity began measuring in 2002 to build greater awareness of estimated health care costs and the importance of starting to plan and save early to meet those anticipated expenses. Since then, the estimate has risen a total of 88% (from $160,000).”

The Fidelity study showed that the major health care costs are pretty evenly split between Medicare premiums and co-pays, deductibles, and co-insurance:

Asset Allocation

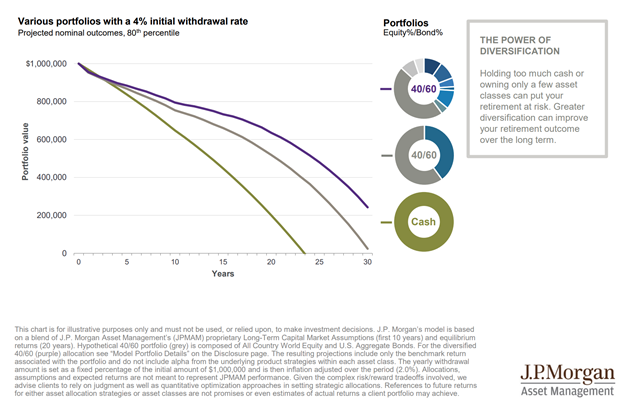

Referencing back to the 4% withdrawal rule, that historical study assumed that the retirement portfolio was invested—not held as cash. In fact, this chart from JP Morgan shows that an initial withdrawal of 4% from a cash portfolio will likely deplete a portfolio after 20-25 years:

The above chart also illustrates how asset allocation and diversification help to mitigate risk in retirement. A portfolio invested in 60% global stocks and 40% U.S. bonds (a rather common balanced retirement portfolio) will most likely support a 4% withdrawal stream over a 30 year period. However, additional diversification can allow for additional return potential without increasing total portfolio risk dramatically.

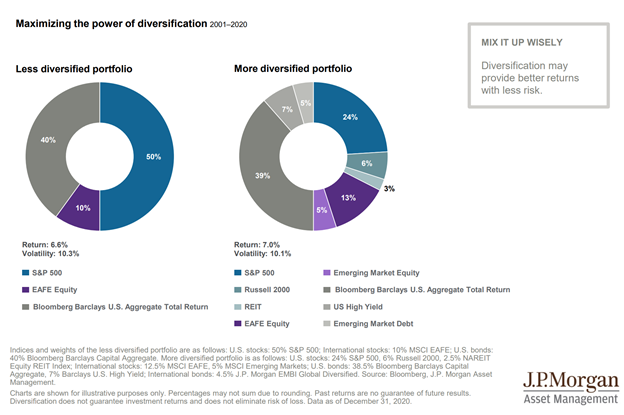

As illustrated below, adding additional asset classes like small stocks, real estate, and high yield bonds has historically produced higher returns than a less diversified portfolio (7.7% annually vs. the less diversified portfolio return of 6.6%) with less risk (10.1% annual volatility compared to the less diversified portfolio volatility of 10.3%).

It can be a lot to consider, so if the WILMA risks of retirement are worrying you, we are happy to work with you to build a plan to mitigate each of these as much as possible!