Financial Moves You Can Still Make Before Filing Your Taxes This Year

Tax season is in full swing, 1099s are all finally released, and while you may be preparing to file, there are still some last-minute financial moves you can make to maximize your refund or reduce your tax liability before April 15th 2025.

1. Contribute to an IRA

One of the best last-minute tax-saving moves is contributing to an Individual Retirement Account (IRA). If you qualify, you can contribute up to $7,000 ($8,000 if you’re 50 or older) for the 2024 tax year until April 15, 2025. Traditional IRA contributions may be tax-deductible, reducing your taxable income.

For tax reporting purposes, please note you will not receive an official tax document reporting your 2024 contributions to IRAs until May 31, 2025 on the Tax Form 5498. It is up to the individual to track and provide transaction details of IRA contributions when filing taxes.

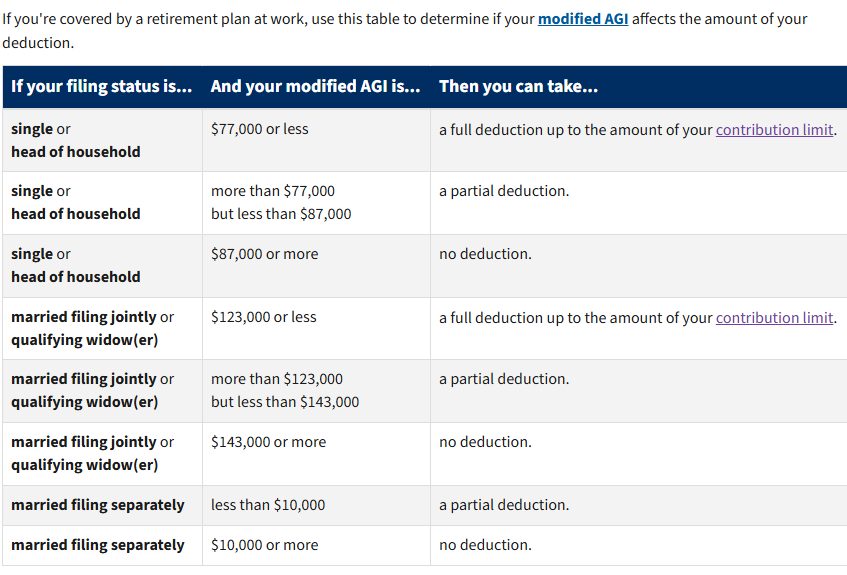

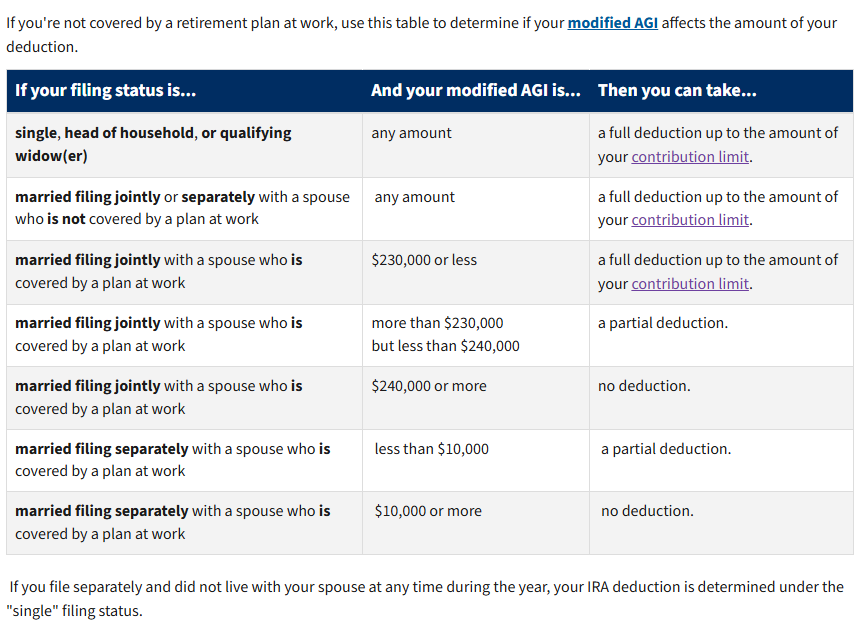

How to know if your IRA contributions will be deductible:

Source: https://www.irs.gov/retirement-plans/plan-participant-employee/2024-ira-contribution-and-deduction-limits-effect-of-modified-agi-on-deductible-contributions-if-you-are-covered-by-a-retirement-plan-at-work

2. Fund Your Health Savings Account (HSA)

If you have a high-deductible health plan (HDHP), you can still contribute to a Health Savings Account (HSA) until the tax filing deadline. The 2024 contribution limits are $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up contribution for those 55 and older. Contributions to an HSA are tax-deductible and can grow tax-free when used for qualified medical expenses.

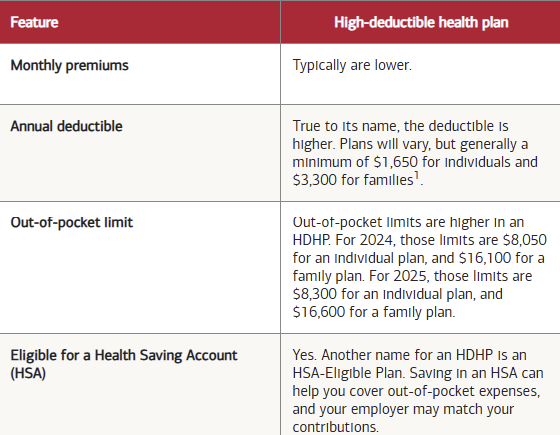

How to know if you have a high deductible health plan:

Source: https://healthaccounts.bankofamerica.com/how-an-HDHP-works-with-an-HSA.shtml

3. Maximize Contributions to a SEP-IRA (for Self-Employed Individuals)

If you’re self-employed or a small business owner, you may be eligible to contribute to a Simplified Employee Pension IRA (SEP-IRA), which have higher contribution limits than a traditional IRA or Roth IRA.

Because of the SECURE 2.0 Act, contributions to SEP IRAs can now be made with either pre-tax dollars (like with a traditional IRA), or after-tax dollars (like with a Roth IRA). If you were self-employed in 2024, you can generally set aside up to 20% of your net income or $69,000, whichever is less. If you had employees, you can contribute to their retirement account as well—up to 25% of their compensation or $69,000.

Contributions can be made until the tax deadline, and they are deductible, helping lower your taxable income.

4. Check for Missed Deductions and Credits

Before you finalize your return, review potential tax deductions and credits you may have overlooked, such as:

- Education Credits – The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) can help offset education expenses.

- Energy-Efficient Home Upgrades – If you installed energy-efficient windows, doors, or solar panels, you may qualify for tax credits.

- Charitable Contributions – If you made donations in 2024, ensure you’ve accounted for them. Even non-cash contributions (like clothing or household items) to qualifying charities can be deductible.

- Property Tax, State and Local Income – You may also deduct up to $10,000 in property tax, state, and local income tax

- Medical Expenses – Medical expenses that exceed 7.5% of your Adjusted Gross Income

Final Thoughts

Taking advantage of these last-minute financial moves can help you optimize your return and set yourself up for financial success and possibly mitigate your tax liability for 2024. As with any tax planning, we highly recommend working with a certified accountant to ensure accuracy.

Preparing for tax filing is not fun, just as Dude realizes playing dress up with his human sister is uncomfortable; however the goal is to hopefully be rewarded at the end. (And yes, he was rewarded for being the best princess there ever was).