What is a Roth IRA?

If the only thing you know about a Roth is that it rhymes with sloth …well, then this post is for you. So. Are you ready to find out what this Roth IRA thing is?

It is a type of retirement account!

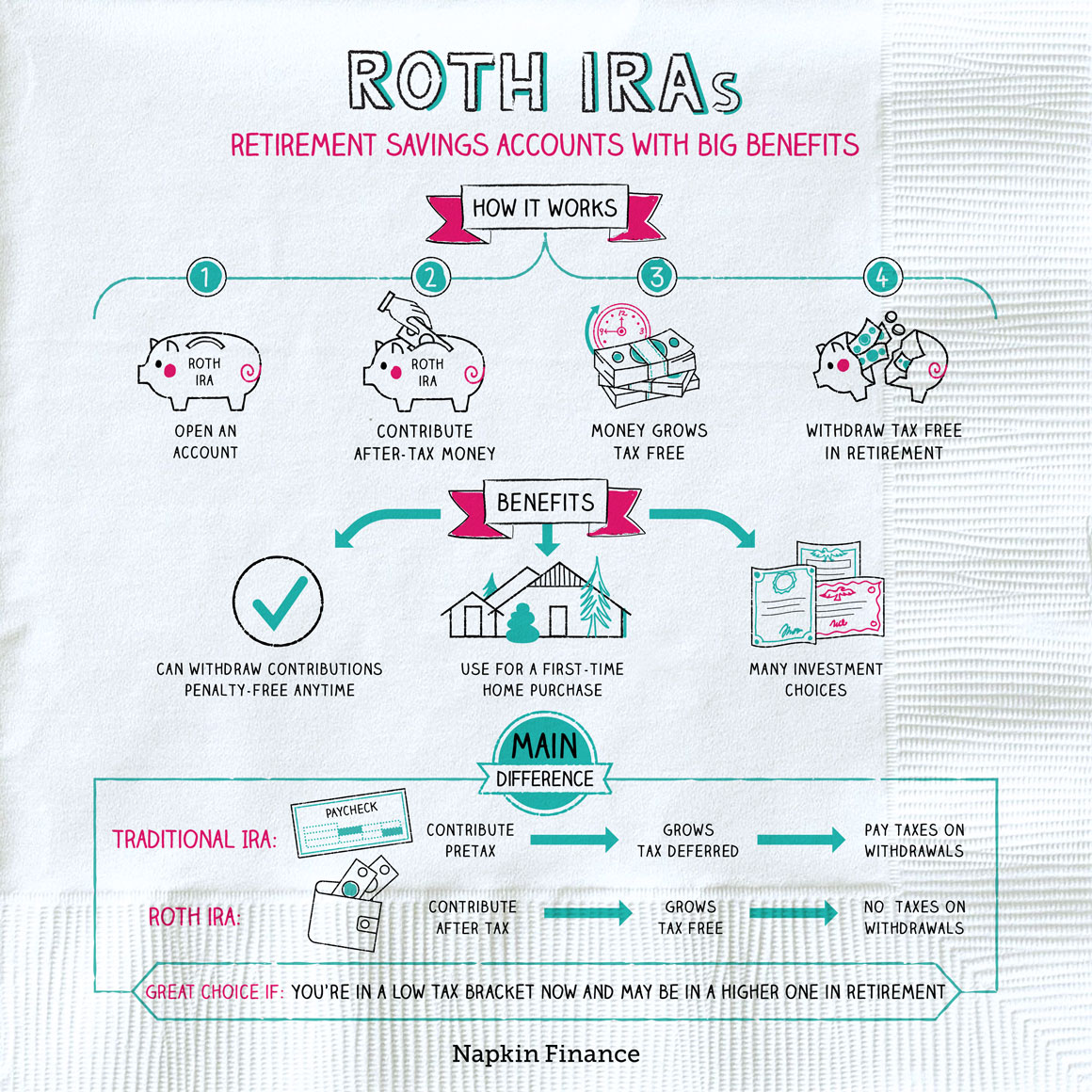

Roth IRAs (IRA stands for Individual Retirement Account) are specific retirement accounts that you can open with a financial advisor that allow you to contribute post-tax, earned income each year as long as you qualify, AND withdraw those funds at retirement age TAX-FREE. They can be incredibly helpful to open while you are young because they allow you to contribute money each year as long as your income falls below a particular threshold. Once your income exceeds the threshold limit, you are no longer able to contribute to the Roth IRA, but are still able to withdraw these funds once you’ve held the account for at least five years and have reached the age of 59.5.

What’s the big deal with Roth IRAs?

The distributions are TAX-FREE. Plain and simple. Most other retirement accounts will require you to pay taxes on the distributions when you withdraw the funds at retirement age. Depending on your tax bracket at retirement age, those tax fees can definitely add up! Therefore, having a Roth IRA that you can withdraw from tax free can be a very useful source of income.

Who can open a Roth IRA?

Anyone can open a Roth IRA as long as you have earned income. Note, income received from real estate is not considered “earned income”.

How much can I contribute to the Roth IRA each year?

As long as you still qualify, you can contribute up to $6,000 each year (…more if you’re over the age of 50). You also don’t need to make your contribution in a lump sum. For our younger clients, I suggest setting up monthly, recurring contributions that won’t stress them out.

How can I be sure I qualify?

For the tax year 2020, you can contribute to a Roth IRA as long as you are making less than $139,000 as a single individual. If you are married filing your taxes jointly, you and your spouse can combine incomes for up to $206,000 before you are no longer eligible to contribute to a Roth IRA. You can contribute towards 2020 until April 15, 2021!

How are they different from Traditional IRAs?

Though both offer ways to save and invest for your retirement, they are different in the way that contributions and distributions are taxed. Contributions made to a Traditional IRA are not taxed on the way in, but are taxed on the way out (when you withdraw the funds at retirement age/at least 59.5). Contributions made to a Roth IRA, however, are taxed on the way in so that distributions or withdrawals later in life are not. Roth IRAs also have certain income requirements, whereas Traditional IRAs do not.

How do I know if a Roth IRA is right for me?

Before opening any account, it is wise to consult with a financial advisor to ensure this decision is in your best interest. Consider meeting with a financial advisor to open a Roth IRA if you are eligible to contribute, have earned income, already maximize your participation in an employer sponsored retirement plan [such as a 401(k) or 403(b)], and have the ability to put aside savings into a retirement account.

What if I contribute to a Roth and then eventually no longer qualify to contribute?

You’re in luck! If you find that you’re no longer qualified to contribute to a Roth IRA (because your income exceeds the limits required), then you can still have your account, and look forward to taking tax free distributions from the account come retirement time. You may no longer be able to contribute money to this account, but the account can still be invested. You can also consider opening a Traditional IRA at this point, which does not have any income restrictions associated with it. (*However, if you do have both a Traditional and Roth IRA, note that you cannot exceed the $6,000 contribution limit between the two of them).

How does all of this make financial sense?

Take this example: if a 23 year old were to put $5,500/year into a Roth IRA for 8 years and then stopped contributing, they would have $939,677.35 by the time they were 65 (assuming an average interest rate of 8%). The best part? This money would be allowed to be withdrawn without paying any taxes on it. Seem insignificant? Imagine paying 15% taxes on that money. That would amount to a $140,951.60 tax bill. Not so insignificant!

Help! I need to access funds in my Roth IRA?

As long as you have had your Roth IRA account open for 5 or more years, you can withdraw your contributions any time on a penalty free, tax free basis. There are also other exceptions to the early withdrawal, such as $10,000 penalty free for a first time home purchase.

Roth IRAs have many advantages and are certainly something to consider when planning for retirement.