The Problem of 5 + 2

I love a good accent. I love hearing clipped British notes, the slow Southern drawl, or my favorite—the lilting Irish brogue. Hence, the reason why my favorite economist is Dr. David Kelly from J.P. Morgan—he discusses the world economies with sly humor and a lovely Irish lilt. He is easy to listen to, and not just because of his accent. Dr. Kelly explains challenges and opportunities in the current economic environment in quick, concise, straightforward notes.

The 5 + 2 Investing Puzzle

In a recent webcast by JP Morgan, Dr. Kelly led with discussing the problem of 5 +2. While all of us our answering “7” in our minds, he explained that the problem is not simple arithmetic, but is a more complex question of what do investors do in a world where the expected returns on equities over the coming decade are around 5%, and the expected returns on fixed income are near 2%. These low return assumptions challenge savers and retirees alike. Most retirement plans were built with return assumptions that ranged from 7-10%…a far cry from the 4-5% that a balanced portfolio is expected to generate over the next decade.

Why International Stocks Matter

With the problem being 5 + 2, Dr. Kelly made the case that international equities are part of a solution. Here are a few compelling reasons that he laid out for consideration:

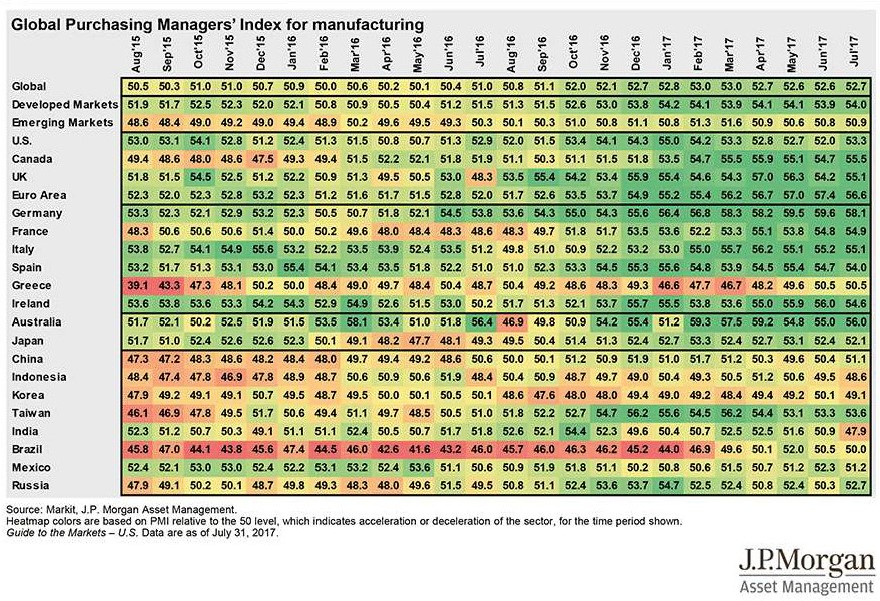

- International economies are still growing and strengthening. Below is a manufacturing heat map from JP Morgan’s Guide to the Markets. It shows strengthening economies as green, slowing countries as red—and you can see that most international economies are gaining momentum.

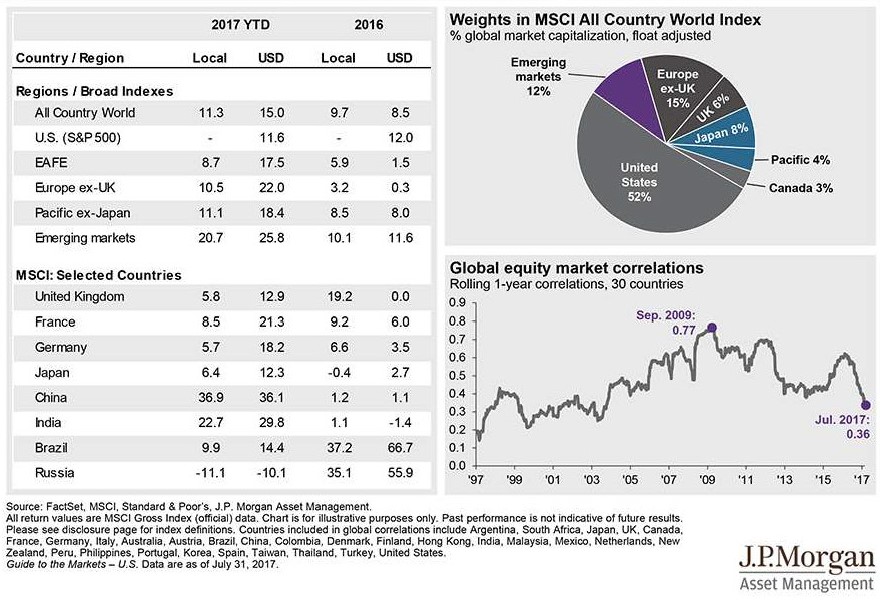

- Half of global equites are outside the US, and correlations between the markets are slipping. As shown by the chart in the lower left corner, instead of moving in lock step together, international equities are now behaving much less like US equities—decoupling from the relative historical strength of the US and forging ahead on their own. Additionally, international equities are benefiting from the reversal of a strong US dollar. In this chart, you can see that the falling dollar amplified the strong returns in Europe (EAFE in the chart—in euros, the US investor earned 8.7% in 2017. When that same investor converts their euro denominated return to US dollars, the favorable exchange rate amplifies their return to 17.5%.

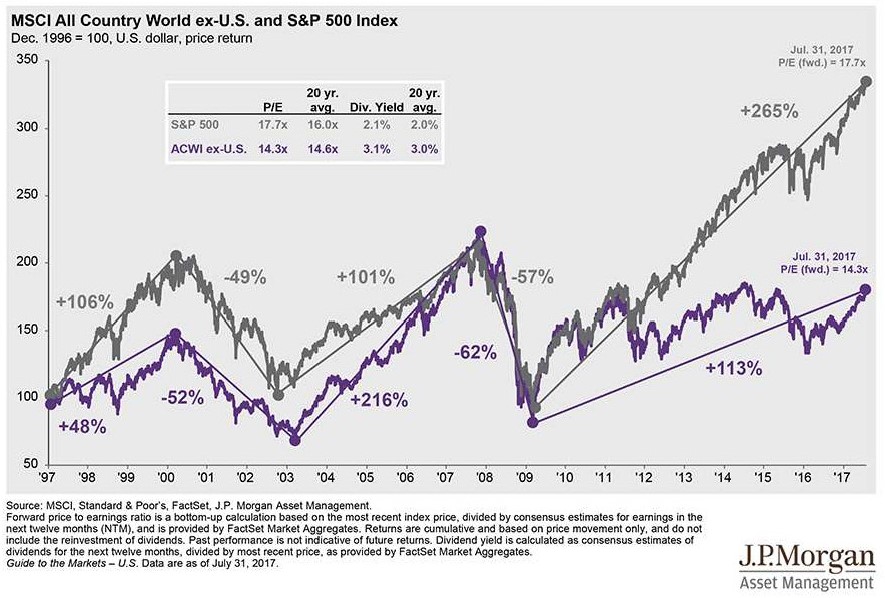

- Investors haven’t missed the boat. Despite strong returns so far this year, international markets have so much more room to grow to return to their old historic highs. In addition, valuations relatively lower than those in the US markets imply that international markets are still slightly undervalued. And, higher dividend yields than the US means that investors are being compensated fairly to be patient and wait for capital growth.

While 5 + 2 is a problem that needs to be solved, Dr. Kelly’s case for the world of opportunities is strong, and long-term investors should consider prudent allocations to equities around the globe!