Happy T + 2 Day! (and Happy Birthday Molly!)

We celebrated our youngest daughter’s 3rd birthday over the weekend. It was a very nice gathering with friends and family. And the kids even went swimming which must have been pretty darn cold. Peppa Pig was the dominant theme, and Molly cutely identified each of the British-based cartoon’s characters sitting atop her cake.

Molly and her very supportive sister – I am sure this has nothing to do with the cake on the table!

Trade Settlement Changes: From T+3 to T+2

Coincidentally, today (September 5th) is also the day that trade settlements go from T + 3 to T + 2 within the U.S financial industry. Prior to today, most securities settled in three business days. So, if you sold a stock today (the trade date or “T”), your proceeds (money) would be available to you three business days after the trade date. So, in this example, you would receive your proceeds on Thursday.

Understanding the Shift from T+3 to T+2 in Trade Settlements

Now, with the T + 2 change, all stocks and securities in the US financial markets will settle on a trade date + 2-day schedule. If you place a trade to sell a stock today, your money would be available to you on Wednesday. Vanguard summed up what the change means in their August 31st article:

“Individual investors and financial markets in general will benefit in several ways:

- Risk reduction.During the settlement cycle, an intermediary representing buyers or sellers could experience financial stress and become unable to fulfill its trade obligations. A shorter settlement-cycle time reduces a number of risks, including credit, market, counterparty default, and liquidity risk—all of which lowers systemic risk.

- Faster payment.Buyers will need to make faster payments for securities that they purchase, and sellers will get paid more quickly. This enhances efficiency and ensures coordinated transactions among market participants.

- Increased global harmonization.Several countries—including most members of the European Union, the United Kingdom, Australia, and other countries in Asia and the Pacific—have moved their settlement cycles to T+2. Canada and Mexico are scheduled to do so in September.”

Accessing Your Investment Funds More Efficiently

Many clients and potential clients that we talk to often have the perception that their non-retirement investment accounts will be “tied up” or otherwise not available to them should the need arise. That is simply not the case, and the new, faster settlement time makes it even easier to access funds from an investment account. We often recommend that clients link their investment accounts to a checking account or other operating account, so, if there is an emergency need, money can move electronically very efficiently and safely.

No matter what, we always try to avoid clients addressing a short-term need with long-term money. We want to avoid getting into a situation where an aggressive investment is being sold at a less than opportune time (read: the stock is down). More aggressive holdings should ideally be sold at a specific price target rather than when a need arises. There are investments, such as short-term bonds, that don’t fluctuate as much, but have the potential to earn a little more interest than a checking or savings account.

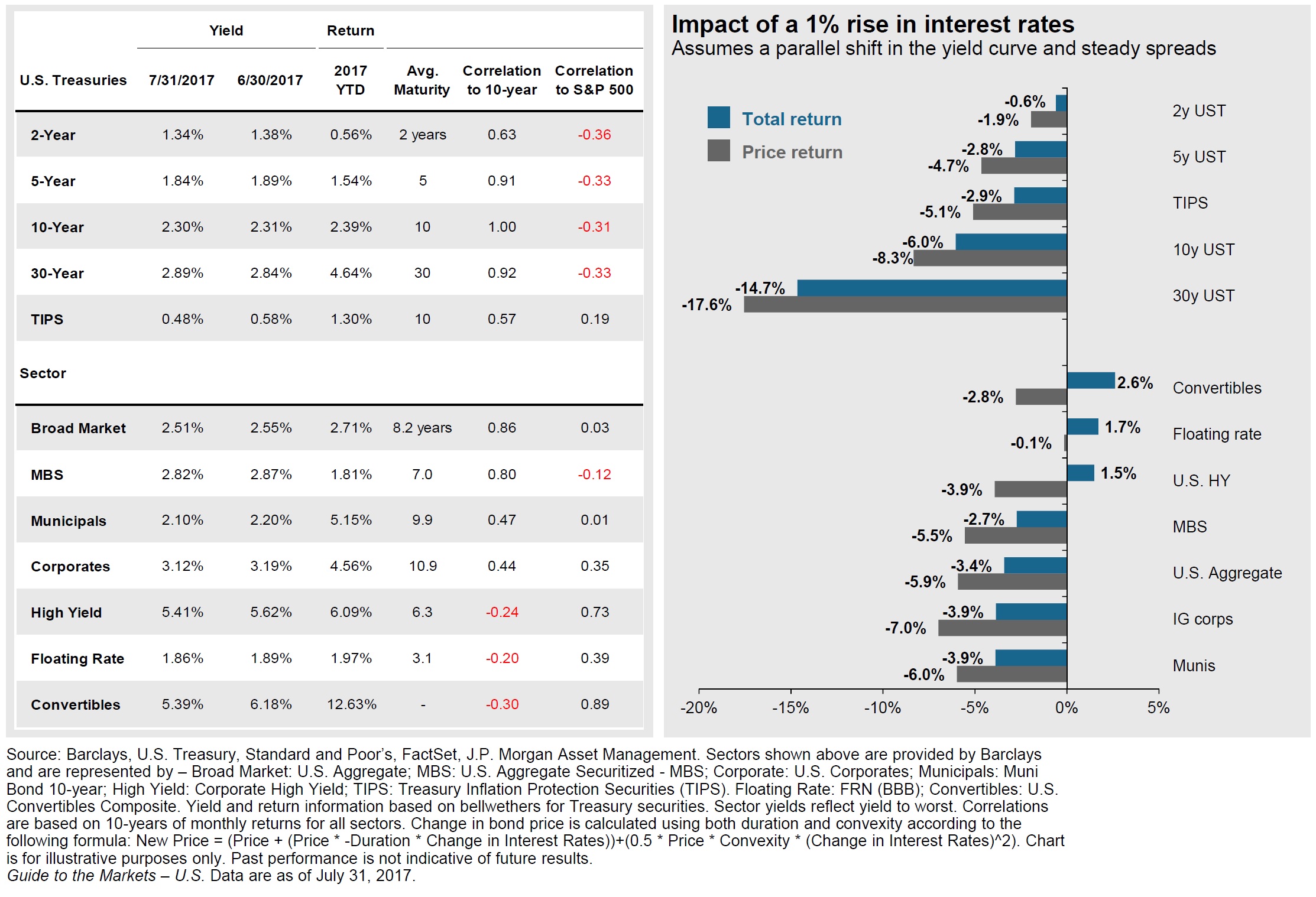

Certainly, even short-term bonds come with a small amount of risk, but they give you a much better chance at keeping up with inflation. However, they may be more appropriate than leaving too much cash in a zero-interest checking account. The chart below is a good example of where we sit with interest rates today. It is a bit busy, but it contains a lot of great information on how bond prices can be affected by rising interest rates.

So, if you are an investor and need money quickly, you will be able to get to your money one business day faster. Happy T + 2 Day and Happy Birthday Molly!