The “R” Word

The dreaded “R” word is frequenting headlines and the minds of investors as the uncertainty of a “hard” or “soft” landing comes to the fore front. The “R” word being recession, a word that brings uncomfortable flashbacks to almost anyone and stirs up an instinctual fight or flight response.

And it’s with good reason that the question on recession has become more frequent. Diversification faced a challenging year in 2022, with the 60/40 portfolio (60% S&P 500 and 40% Bloomberg U.S. Aggregate Bond index) down 16% on a total return basis. Not only was it the worst performance since 2008, but also it was the first year since 1974 in which both stocks and bonds declined

While it is impossible to exactly predict what will happen in the economy and the markets in a week, much less in several months, it’s helpful to know what defines a recession, recessionary indicators, and what most of our readers want to hear – how to position a portfolio in the case of a recession.

What is a Recession?

Recessions are typically the 4th phase within a business cycle where economic activity contracts, profits decline, and credit is scarce for businesses and consumers. Recessions are also usually combined with rates and business inventories falling, which allows for the next business cycle to take place (the early cycle).

NBER, the National Bureau of Economic Research, defines this period as “a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

NBER uses trailing data (i.e- data from the past), which usually means that by the time a recession has been declared, the stock market and the economy may have already been through the worst of it and on a path to recovery. For example, when the 2020 COVID recession hit, NBER announced the recession in June 2021 … more than a year after the fact. Here is what the stock market did in that period:

Granted while the recovery from the recession in 2020 was rapid and that being historically the shortest recession, the average length of recessions since the end of WWII recessions last approximately 11.1 months. In some cases 11 months can seem like a lifetime, it’s important to point out that recessions have historically been the shortest phase of the cycle.

Note : This does not include the 2020 recession.

Historical Indicators of Recessions Include:

Decline in real GDP (Gross Domestic Product)

GDP does play an important role in the identification of a recession as the textbook definition of a recession is “generally identified by a fall in GDP in two successive quarters”. And while the rate of growth of real gross domestic product (GDP) is a key economic indicator, this estimate is released with a delay.

Whether or not we are in a recession, there will be a recession, data is pointing to slowing growth.

As of the end of February, data showed that the U.S. economy cooled at a faster pace in the 4th quarter than previously reported. U.S. GDP growth revised down to 2.7% from 2.9% and 3.2% from the 3rd quarter. Reflects a downward revision to consumer spending figures and exports. Personal consumption expenditure rose less in the 4th quarter than predicted.

In addition to decline in GDP, decline in real income, employment, industrial production, and wholesale/retail sales historically have indicated recession.

Yield Curve Inversion

The spread between the 2-year and 10-year Treasury yields has fallen to the deepest inversion since the 1980s. Historically, an inverted yield curve has been a somewhat reliable indicator of a recession within 12 to 18 months; however there is no correlation between the depth of the inversion and the severity of a recession.

So What to Do?

One of the most prominent questions we hear is, “how do I position myself to weather this?”

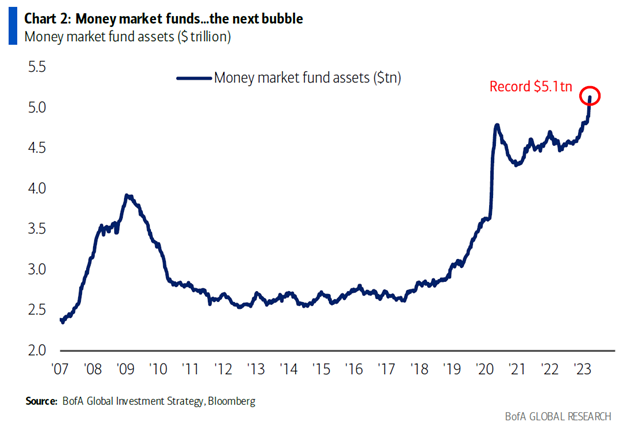

Per Nathan’s blog last week, while it feels safe to hold onto cash in times of uncertainty, “Cash is not always king”. The teaser rates of 5% on short term T-bill/CD will evaporate fast and so you only will earn that rate for a year or two.

For conservative investors, high quality investment grade bonds are paying substantially more and if typical recession conditions repeat themselves, the value of those bonds will increase as rates come down in the future.

Within stocks, high cash flow and high quality companies matter in a slow growth regime.

In a recession where growth contracts, stocks that are sensitive to the health of the economy tend to lose favor and defensive stocks perform better. Think companies that produce items which consumers are less likely to cut back on during a recession (non-discretionary goods, electricity, prescription drugs for example)

Companies returning capital to shareholders in the form of dividends has paid off during the long-term.

When stock prices depreciate, investors tend to prefer to get paid something as prices recover. Stocks engaging in buyback and dividend activity indicate a signal of a firms strength though the ability to distribute cash in times of economic stress.

Stocks can be considered the best long-term hedge for inflation due to the historical risk premium they have exhibited above inflation, but also because most companies are able to pass along rising input costs over time to their customers. This pricing power is evidenced by the long-term earnings and dividend growth of the market, outpacing inflation. Even during the 1970s and 1980s, when inflation averaged over 6% for two decades, dividend growth kept pace with inflation.”

In response to the concern of recession, Meridian continues to carefully assess the current economic environment, watch the indicators, and are making tactical shifts we feel are prudent. However, even given short term uncertainty, long term investment principals should still hold.

We encourage our clients to review their objectives, which allows matching individual risk tolerance and timelines with the ability to take risk and build appropriate portfolio. A strong, well laid out financial plan incorporating an appropriately allocated portfolio can help investors prevent slipping particularly when the short term is muddy.

Don’t be like Chae and not prepare for muddy terrain