Rules of Thumb: Financial Planning Hack?

I recently heard a radio story about Fidelity Investment’s Rule of $2,000. In an effort to simplify college planning for parents, Fidelity says that in order to determine how much you should have saved currently for your child’s college expenses, multiply your child’s current age by $2,000. So for my 11 year old daughter Melanie, we should have $22,000 saved for her college by now.

Fidelity bases their rule of thumb on the goal of saving one half of the average cost of a four year education (tuition, room and board) at an in state public university. And, they assume you are investing your savings in a tax qualified 529 plan (like the ones we covered in this blog post). So, their “Rule of $2,000” doesn’t help you much if your child goes to a private school or out of state university!

Another financial rule of thumb is that you should have your “age minus ten” in fixed income investments in your portfolio. So, for my husband, who turns 40 this year, he should have 30% of his portfolio in fixed income. The thought behind this rule is that your portfolio should get more and more conservative as you get closer and closer to withdrawing from it.

However, “age minus ten” completely ignores other factors that should go into your portfolio planning. Factors such as whether your job is steady (like a teacher or a government employee), your upcoming withdrawal needs, or other assets/income streams (like rental properties) all matter. Additionally, yoru own tolerance for losing money matters—in my husband’s case, he barely opens a statement and doesn’t mind taking prudent risk, so even though he should have 30% in fixed income, he prefers 15-20% in fixed income because it is too steady and boring for him. Likewise, we have clients in their 20s and 30s that saw the ravages of the 2008 crash up close, right when they were starting their careers and are still a little risk averse. For them, even though they should have 80-90% of their money in the stock market, they cannot handle the volatility and are more comfortable at lower levels of risk.

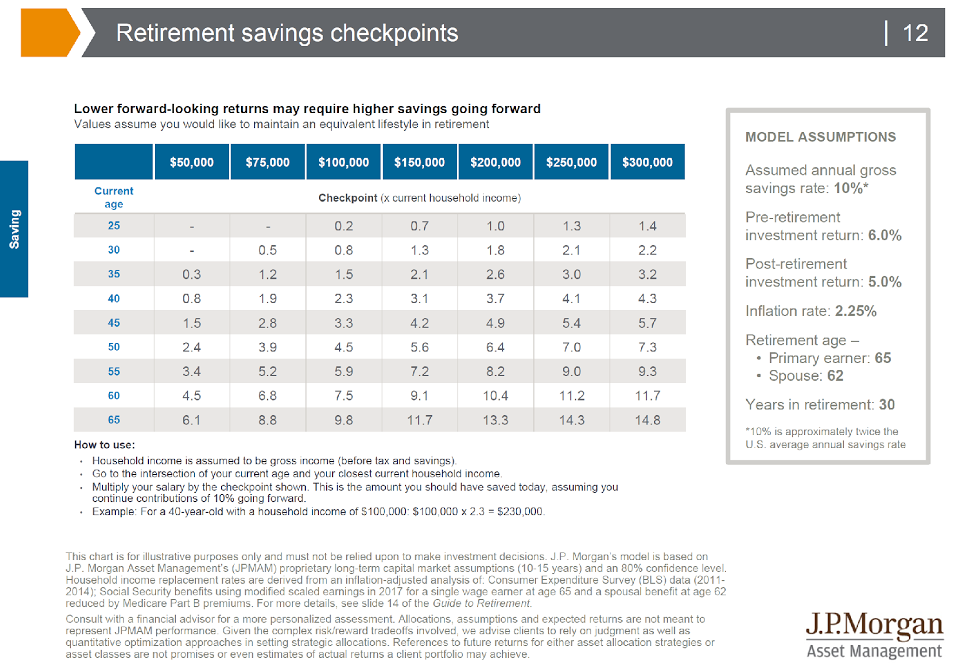

There is no way to make a rule of thumb for retirement savings (other than the oft quoted “4% rule”—i.e. you can withdraw 4% of a balanced portfolio annually for 30 years with relatively low chance of depleting the account), so JP Morgan assembled this great chart to give checkpoints to folks trying to see if they are on track for retirement:

As their instructions say, to use this chart, simply go to the intersection of the number closest to your current age and the income figure that is closest to your current household income. This is a good rule of thumb guideline, but all of the fine print on this chart matters.

This chart assumes that you are currently saving 10% of your income (which is TWICE that of the average household in America!). It assumes that you retire at 65, that you have your money invested for long term growth, and that social security still exists with its current benefit rates intact. This chart also ignores other sources of income (like pensions or rental real estate).

We think that all of these rules are great starting points for a conversation, but ultimately, they are like a one-size fits all shirt…they may fit everyone, but they flatter nobody. Instead of a one-size fits all approach, real financial planning is more of a tailored shirt…cut just right to suit you well. If you would like some help in building a tailored plan, call us anytime! We love to create plans that make our clients feel great!