You’ve Gotta Know When to Hold ’em

As someone who likes to think of himself as a “prudent investment manager,” I always cringe a little when someone compares investing to gambling. While there is certainly inherent risk in any type of market-related investment, there are tried-and-true strategies that will yield positive investment results over time. Gambling, on the other hand, is a very different story, and there are very few gamblers who can boast time-tested results (if they are telling the truth!).

Nonetheless, the lyrics from Kenny Rogers’ famous song The Gambler contain some good advice for investors. Certainly, the refrain is familiar to most of you: “You’ve got to know when to hold ’em, Know when to fold ’em, Know when to walk away, And know when to run…” And, while this post is not about staying the course, the current market volatility does make you think it might be time to run (SELL!). We would advise against that, and in fact, you might be able to use some of those investment losses for your benefit.

Turn Losses Into Wins

Currently, we are reviewing our clients’ accounts and looking for losses to take before the end of the year. Yes, I am saying we are purposely selling some investments at a loss!

“Every gambler knows, That the secret to survivin,’ Is knowin’ what to throw away, And knowin’ what to keep…”

The strategy to which I am referring is called tax loss harvesting. Note that it only works in non-retirement accounts, so there is no need to do this in an IRA, 401(k), or other retirement plan type. However, if you have an investment or brokerage account with holdings that have gone down, it might be a good idea to sell them before the end of the year. As long as you wait at least 30 days after the sale, you can buy back the same holding and still realize the loss for tax purposes.

Tax Trick for Investors

From Hayden Adams at Charles Schwab:

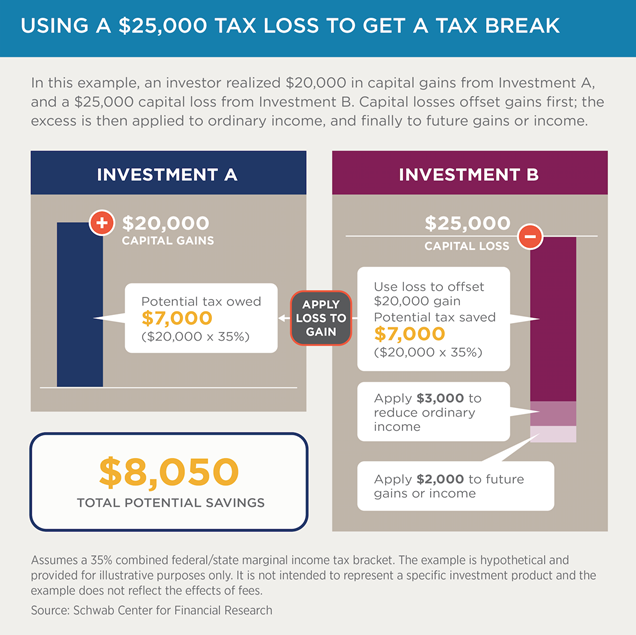

“Tax-loss harvesting generally works like this:

- You sell an investment that’s underperforming and losing money.

- Then, you use that loss to reduce your taxable capital gains and potentially offset up to $3,000 of your ordinary income.

- Finally, you reinvest that money into a different security that meets your investment needs and asset allocation strategy.”

Like many tax issues, it’s best to consult with your accountant or CPA if you aren’t sure if this strategy is appropriate for you. Knowing what to throw away (and when) and what to keep might just work to your benefit.