The Halfway Point

We’ve officially hit the half way mark in the year and as another parent pointed out, the half way mark of the summer as well. Last summer looked a lot different for everyone, so we are trying to make up for “lost time” and are squeezing in as many quintessential summer activities as possible without the kiddos missing too many naps! 😉

Summer isn’t complete without a hose and a dog

Mi Cha meeting the incredible wing walker at The Flying Circus on the 4th

And while this time of year, most of our focus is on a combination of soaking up the sun, spending time with our families, and vacationing, this time of year is usually a good time to do a mid-year financial check up both from the planning and investment standpoint. Here are a few places to start:

1. Check in on savings rates for retirement and other goals.

- Rule of thumb is to save 15 – 20% of gross income depending on your goals. If you have other goals outside of retirement to save for, such as education costs or a home purchase, a higher savings rate may be needed. If that number feels too painful to do all at once, increasing contributions a little bit at a time and utilizing an auto increase feature is a great way to ease into it.

- Check in to see how much you have contributed to your IRA or employer sponsored plan for the year so far if you are planning on maxing out your contributions. Do you have more room in your budget to increase contributions? The annual contribution limit for 401(k)s / 403(b)s is $19,500 if you are under the age of 50 and an additional $6,500 per year totaling an annual contribution of $26,000 if you are 50 and older.

- Traditional and Roth IRA contribution limits are $6,000 with an additional $1,000 for those 50 and older and contributions can be made until tax filing deadlines (as of right now April 15 2022). If you are within the income thresholds to make a deductible IRA contribution, this strategy reduces your taxable income, ultimately reducing your tax liability. If you foresee income levels rising in the future and have less than $140,000 in Modified Adjusted Gross Income (MAGI) if you file single or less than $208,000 in MAGI if you are married and file jointly, you are able to make a Roth contribution (keeping in mind taxes are paid now on Roth contributions).

2. Check in on emergency savings and cash levels.

- If you have taken on any big home projects (like the rest of America!), bought a house, or had a big expense, now is the time to start refiling the emergency savings bucket back up. Depending on individual circumstances (i.e – future short term cash needs, type of employment, family situation) typically it is recommended to have 3-6 months of living expenses in an easily accessible account.

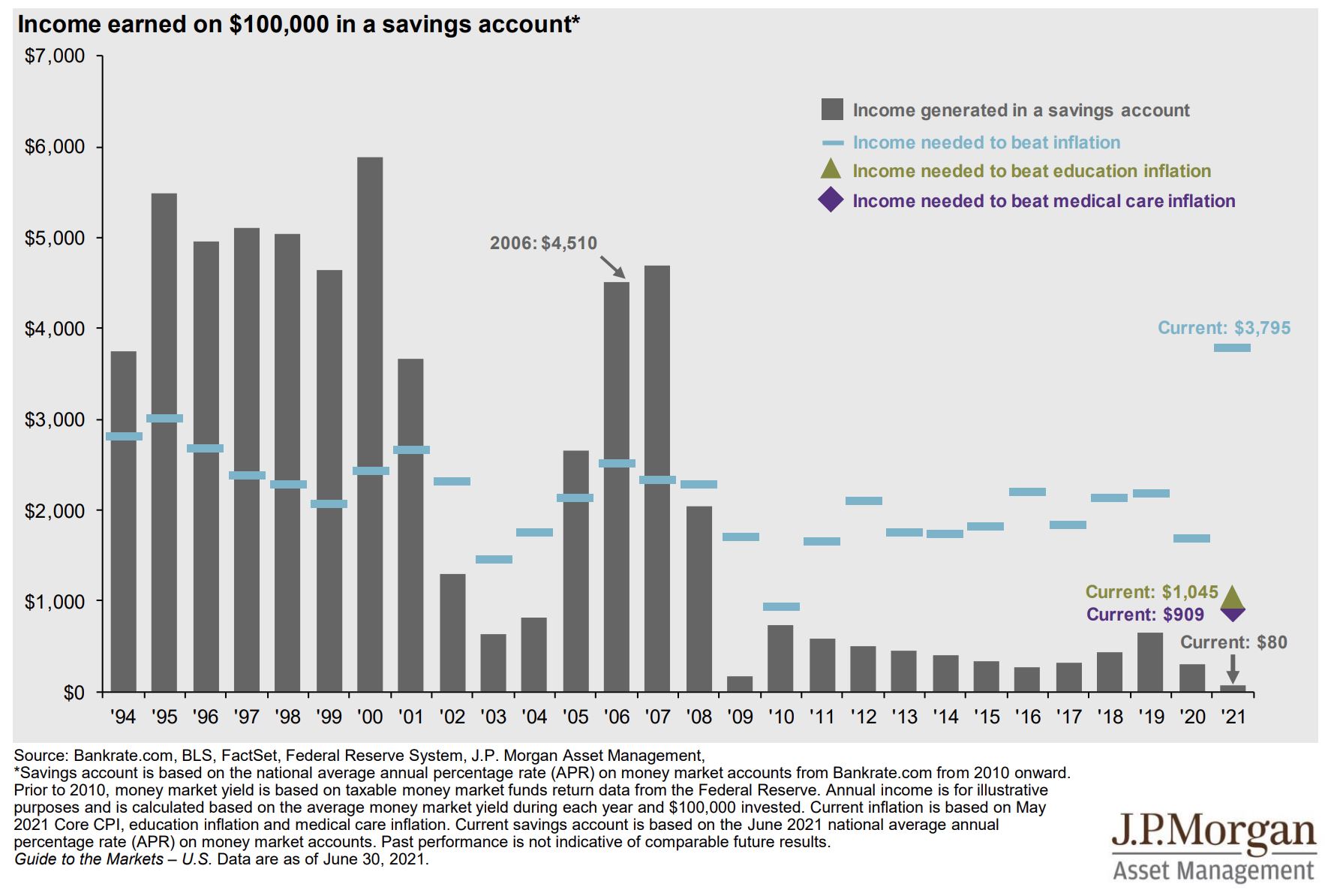

- However, many individuals are finding themselves in the opposite situation as savings levels today are almost double what they were pre-pandemic. If you are finding yourself with extra cash on hand outside of emergency savings and do not have short term cash needs, putting this cash to work will ensure you are at least beating inflation.

Income earned on $100,000 in a Savings Account

3. Gauge debt levels

- If paying off debt was a New Year’s resolution, it’s probably a good time to review progress and if need be, get back on track. Focusing on paying down debt with higher interest rates like credits cards first and sticking with a plan to pay off unnecessary debt can free up cash flows down the line which can be redirected to meeting financial goals.

4. Planned portfolio withdrawals

- If you are retired and are taking regular withdrawals from your portfolio, checking in on withdrawal rates is key to health of the overall financial plan. Although the 4% guideline is a good starting point, the right withdrawal rate is a product of individual circumstances, planning goals, and market performance. Vanguard has a neat retirement nest egg calculator for doing a quick projection. However, nothing can fully replace updating and reviewing your financial plan with your advisor to identify opportunities for improvement and planning on ways to implement such improvements.

5. Revisit portfolio allocations

- Equity markets have hit all time highs over the last few months which could throw off target allocations leading to overweight in equities. We like to rebalance our portfolios quarterly to ensure they stay within target, however if there is a change in goals, timelines, or your risk tolerance (remaining cognizant of recency biases!) it is worth reviewing the balance between equity and fixed income allocations with your advisor.

- However, while this is a useful exercise to do periodically, frequently changing portfolio allocation based off market volatility or news headlines can actually do the opposite of help. The below figures show the difference in returns over a period of 20 years from an average investor (more likely to make changes to a portfolio based off emotions) to one that stays allocated to a target of 60% equities and 40% fixed income.

6. Taxes

- Now is a great time to start thinking about tax planning for the year rather than waiting until December to implement tax saving strategies. We typically begin this process in the fourth quarter, but early preparation provides peace of mind. The first place to start is to check your withholdings to ensure you are not over withholding or under withholding, particularly if you owed or are expected to get a sizeable refund for 2020. My colleague Lucy wrote a very helpful blog on this topic.

- If higher taxes may be on the horizon due to increases in income, it’s never too early to maximize charitable deductions and discuss tax loss harvesting strategies or discussing conversions with your advisor.

Whether you prefer to look at is as having half of the year left or as the year is halfway over, checking in on your financial health at the halfway point in the year is just as much of a good strategy as making beginning of year resolutions or performing spring “cleaning”! Hope you and your loved ones had a safe and very Happy 4th of July!