Financial Planning for Fathers: Ensuring a Secure Future for Your Family

Two of the greatest joys in my life have been witnessing my husband navigating fatherhood and enjoying the growing relationship my family and I have with both my father and my father-in-law. Parenthood is an incredible journey filled with joy, responsibility, and a desire to provide the best for your children, all whilst trying to maintain a sliver of sanity.

With Father’s Day coming up, I have found myself thinking about the insight and guidance our fathers and father figures have provided throughout our lives.

While there are countless life lessons my father and father-in-law have provided me, the one area that really shines through is in finance. My father is well known for his frugality and hyper-focus on savings, which was an invaluable influence on me as a young person and guided me to make sound financial decisions. Although we like to give him a hard time every time he reuses a tea bag.

Below are several pieces of financial advice (reusing tea bags is not one of them) that our fathers and father figures have instilled in us and we feel are worth resharing.

Emergencies happen, set money aside for them.

One of the first steps in financial planning is establishing an emergency fund. Life is unpredictable, particularly with children and pets so having a cushion to fall back can provide peace of mind. When I was fresh out of college and working my first job, my father encouraged me to have a certain level of savings set aside before making a career move, just so I could have a layer of protection and I still think back to this advice regularly. Aim to save three to six months of living expenses in a readily accessible account. This is a starting point, and the amount of savings will fluctuate depending on family size, short-term goals, and employment circumstances This fund can cover unexpected expenses such as medical bills, car repairs, or sudden job loss, ensuring your family’s stability during tough times.

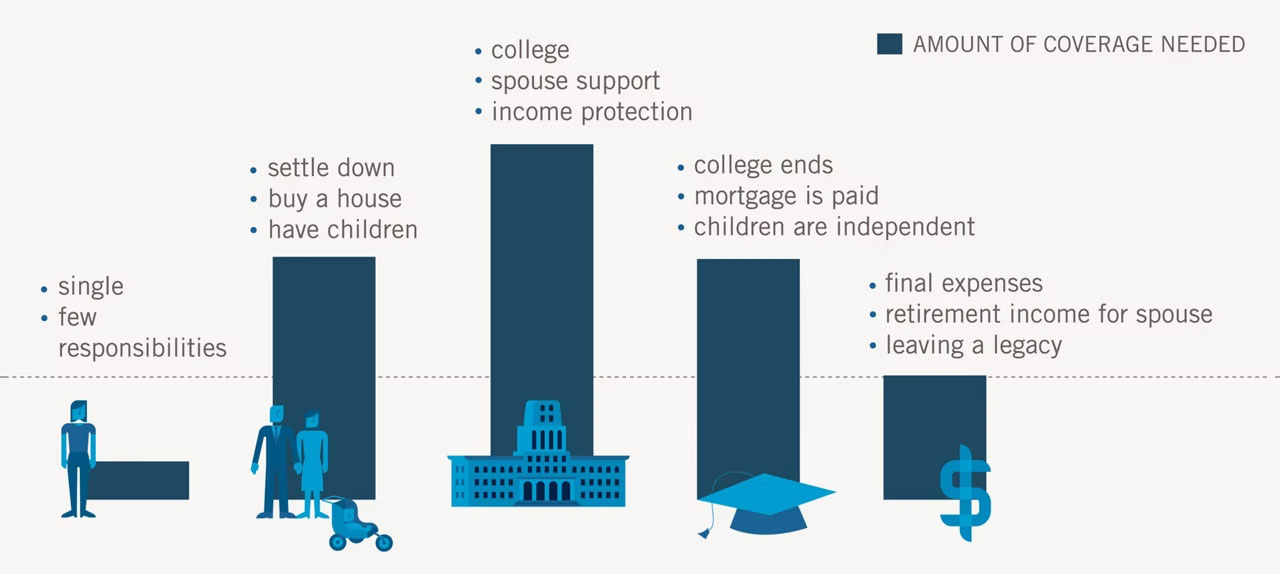

Insurance

Life insurance is a critical component of financial planning for parents. It ensures that your family will be financially secure even if something happens to you. When choosing a policy, consider factors such as your family’s living expenses, outstanding debts, and future financial needs like college tuition. Term life insurance is a popular and affordable option, providing coverage for a specified period, usually covering the period of time until dependents have moved out of the house or at the time of retirement. Many employers will provide life insurance up to $50,000, which is a non-taxable benefit to employees, or up to 1x, 2x, or 3x of salary. Utilizing employer-sponsored life insurance plans is usually the most cost-effective way to obtain coverage.

Source: https://www.prudential.com/personal/life-insurance/life-insurance-101/types-life-insurance

Disability insurance is also critical for working parents, and a vital benefit provided by most employers. One person in four becomes disabled during their working years – and 13% experience a long-term disability that lasts more than five years. For short-term and long-term disability policies, coverage should cover 60%-70% of your gross income.

College Savings Plans or Custodial Accounts

Saving for your child’s future is one of the greatest gifts you can give your children whether it be through a 529 or custodial account. College savings plans, such as 529 plans, offer tax advantages and flexible investment options to help you save for your children’s education covering expenses from Kindergarten past Graduate school.

If you are looking for more flexibility outside of saving for education, several options are available for custodial accounts ranging from savings accounts to investment accounts to Roths. Custodial accounts are opened on behalf of a minor and while the child technically owns the assets in the account, the adult serves as the custodian, making decisions, like managing contributions and making investment choices, on behalf of the child. Once the child turns age of majority the account becomes theirs. Nathan wrote a great blog a few years ago about the benefit of Custodial Roths for kids who are starting to earn their own money. Starting early allows you to benefit from compound interest, making it easier to accumulate a substantial fund over time. These kinds of accounts are also great options for grandparents to open as well.

Estate Planning

Estate planning is not just for the wealthy; it’s essential for anyone with dependents. Creating a will, establishing a trust, and designating guardians for your children ensures that your assets are distributed according to your wishes and that your children are cared for if something happens to you. It’s also important to regularly update your beneficiaries at least on retirement accounts (ideally naming both a primary and contingent beneficiary) and insurance policies.

Personal Finance Lessons from Fathers

Every parent has their own unique way of teaching their children whether it be through words, actions, or gentle nudges in the right direction. And although I’m certain there were times in my life when I seemed not to be paying attention to the life lessons my father was trying to instill in me, I was — and I am grateful for those. Here are a few of my favorite financial words of wisdom from several of the fathers in our lives:

- Only buy what you will pay for this month.

- Buy low, sell high.

- Take credit when credit is due…. But pay off any credit card debt.

- Open a Roth IRA as soon as you start working your first job.

- Come up with a strategy for investing and follow it. Don’t let your emotions deter you from your strategy.

Fathers have the profound responsibility and opportunity to guide their families toward a secure and prosperous future. Whether you’re just starting your journey as a father or are well along the path, remember that every step you take towards financial stability today will have lasting benefits for your family’s tomorrow. Happy Father’s Day!

Grateful for all of the words of encouragement, wisdom, and experiences shared by these great men.