Understanding the “Step-Up in Cost Basis”: Help Your Family Keep More of Your Wealth

One of the most valuable tax benefits available to families is something called a step-up in cost basis. While the name may sound technical, the concept is actually quite simple and can have a significant impact on how much of an inheritance your loved ones ultimately keep.

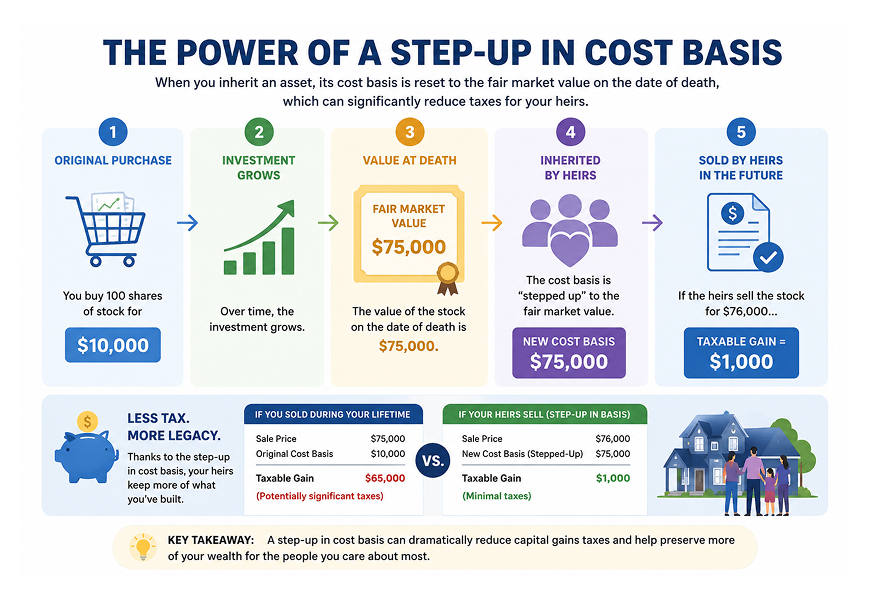

Your cost basis is generally what you originally paid for an investment, including certain purchase costs. When you sell that investment, the difference between your cost basis and the sale price is typically subject to capital gains tax.

For example, imagine you purchased stock many years ago for $10,000. Over time, it grows in value and is worth $75,000. If you sold the stock during your lifetime, you would generally owe capital gains tax on the $65,000 gain.

However, if your heirs inherit the stock after your death, they typically receive a step-up in cost basis. This means the investment’s cost basis is adjusted to its fair market value on the date of your death (or an alternate valuation date if elected by the estate). Instead of inheriting your original $10,000 cost basis, they inherit a new basis of $75,000. If they later sell the stock for $76,000, they would generally owe capital gains tax on only the $1,000 gain rather than the original $66,000 increase in value.

This adjustment can significantly reduce the taxes owed by beneficiaries and allow more of your wealth to stay within your family.

Does the Step-Up Apply to Everything?

No. The step-up in cost basis generally applies to assets such as:

- Individual stocks

- Mutual funds and ETFs held in taxable investment accounts

- Real estate

- Certain other appreciated assets

Retirement accounts, including Traditional IRAs, 401(k)s, and Roth IRAs, follow different tax rules and generally do not receive a step-up in cost basis because they are governed by separate income tax laws.

Estate Planning Strategies to Consider

Understanding the step-up in cost basis can influence many estate planning decisions.

For example, if you own highly appreciated investments in a taxable account and don’t need to sell them to meet your financial goals, holding those assets until death may allow your heirs to receive the step-up in basis, potentially saving them thousands of dollars in future capital gains taxes.

Conversely, if you own investments that have declined in value, it may make sense to sell them during your lifetime and realize the capital loss, since passing them to heirs provides little or no benefit from a step-up.

Another important consideration is gifting. Many people assume that giving appreciated investments to children or grandchildren will provide the same tax advantages as inheriting them, but that’s generally not the case. When you gift an appreciated asset during your lifetime, the recipient typically receives your original cost basis. This rule is known as carryover basis. For example, if you purchased stock for $10,000 that is now worth $75,000 and you gift it to your daughter, she generally inherits your $10,000 cost basis. If she later sells the investment for $75,000, she could owe capital gains tax on the entire $65,000 appreciation. Had she inherited the same investment after your death, her cost basis would likely have stepped up to $75,000, dramatically reducing or even eliminating the taxable gain.

This doesn’t mean gifting is always a bad strategy. Lifetime gifts can still be an effective way to reduce the size of a taxable estate, help family members financially, or transfer assets expected to appreciate substantially in the future. The key is understanding which assets make the most sense to gift and which may be better to leave as part of your estate.

Why Financial and Estate Planning Matter

The step-up in cost basis is one reason why investment management and estate planning should work hand in hand. Coordinating your investment strategy, beneficiary designations, trusts, and estate documents can help preserve more of your wealth for the people you care about.

Every family’s situation is unique. Tax laws are complex and can change over time, making it important to review your estate plan regularly with your financial advisor, tax professional, and estate planning attorney.

Based off the look on my daughter’s face, she’s holding the exact asset she’s been waiting for all morning.

If you plan to leave investments to your heirs, a good question to ask would be: “Am I holding the right assets in the right accounts?” The answer could make a meaningful difference in the taxes your family pays after you’re gone.